After joining Hanwha Group, Hanwha Ocean overcame long-standing financial difficulties inherited from its Daewoo Shipbuilding & Marine Engineering days, returning to profit within just 17 months. The company also became the first Korean shipyard to win a contract for maintenance of U.S. Navy vessels.

Both the normalization of management and expansion into global markets were promises made by Hanwha Group Vice Chairman Kim Dong-kwan in 2023. However, Hanwha Ocean still faces a major challenge: an urgent need for a credit rating upgrade.

Daewoo Shipbuilding & Marine Engineering officially changed its name to Hanwha Ocean on May 23, 2023. At that time, five Hanwha Group affiliates-Hanwha Aerospace, Hanwha Systems, Hanwha Impact Partners, Hanwha Energy (then Hanwha Convergence), and Hanwha Energy Singapore-invested a total of KRW 2 trillion to acquire a 49.3% stake, completing the acquisition.

Currently, Hanwha Aerospace is the largest shareholder of Hanwha Ocean, holding a 46.28% stake. Recently, Hanwha Aerospace increased its shareholding by acquiring all Hanwha Ocean shares held by Hanwha Energy and Hanwha Energy Singapore, as well as part of the stake owned by Hanwha Impact Partners.

This additional acquisition by Hanwha Aerospace is aimed at facilitating a credit rating upgrade for Hanwha Ocean.

On April 8, An Byung-chul, CEO & Head of Strategy at Hanwha Aerospace, stated, “Hanwha Ocean’s credit rating remains relatively weak, and considering the situation of competitors supported by European governments, it is impossible to win orders based solely on product performance and price competitiveness.”

He emphasized the intention to bolster Hanwha Ocean’s credit standing by leveraging the high AA- (Stable) credit rating of its parent company. Ultimately, however, it is also necessary for Hanwha Ocean to enhance its own credit profile.

HD Hyundai Heavy Industries Tops Foreign Exchange Gains Among Big Three Shipbuilders in 2024 with KRW 457.1 BillionHanwha’s Kim Seung-youn and Kim Dong-kwan: Will the Father-Son 'Parallel Theory' Be Completed?Why HD Hyundai Heavy Industries Focuses on 'Surface Ships' and Hanwha Ocean on 'Submarines'Hanwha Group recruits successive foreign talents to lead defense and shipbuilding overseas business'The shipbuilding industry is booming...' Samsung Heavy Industries sells its headquarters building again after 23 years

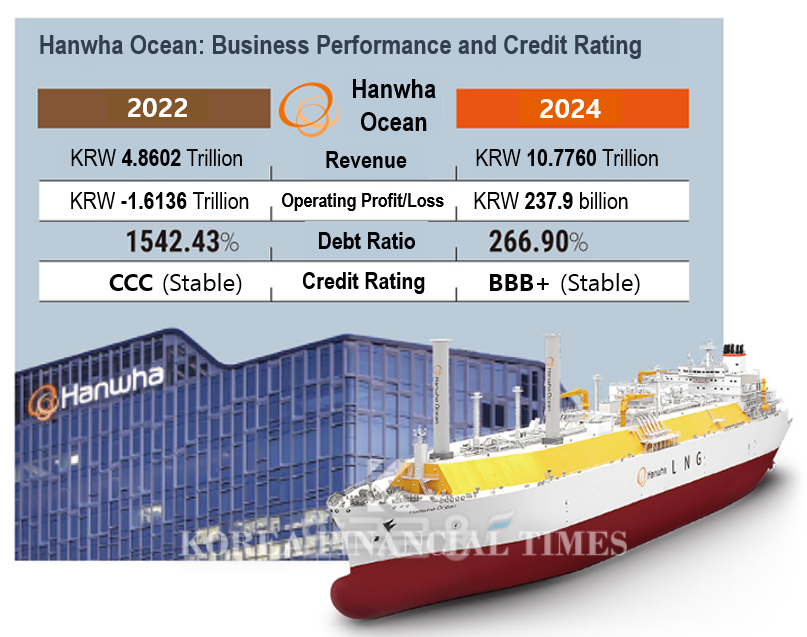

Hanwha Ocean’s current corporate bond credit rating stands at BBB+ (Stable). This is an improvement from the CCC (Stable) rating it held between 2017 and 2022, but remains three notches below competitor HD Hyundai Heavy Industries, which holds an A+ (Stable) rating. A BBB+ rating indicates that while the company is expected to meet its debt obligations, its overall ability to repay debt could deteriorate in the event of adverse changes in the business environment.

An industry insider commented, “If a shipbuilder’s credit rating is low, the company not only faces difficulties in securing financing and increased financial costs, but also risks disadvantages in order competition. Given the long-term contract nature of the shipbuilding industry, a low credit rating can undermine trust in the company’s sustainability, making it difficult to even participate in bidding for new contracts.”

As of the end of last year, Hanwha Ocean’s debt ratio stood at 266.90%. This was a 43.62 percentage point increase from the previous year, but was largely due to increased borrowing in response to a surge in business activity amid a shipbuilding boom. Nevertheless, the company managed to overcome past deficits and achieved an operating profit of KRW 237.9 billion last year, successfully returning to profitability.

Previously, Hanwha Ocean recorded massive operating losses of nearly KRW 2 trillion in both 2021 and 2022, severely weakening its financial soundness. The debt ratio soared from 379.04% in 2021 to 1,542.43% in 2022. However, after joining Hanwha Group, the company reduced its net loss to KRW 196.5 billion by the end of 2023 and improved its debt ratio to 223.28% through a group-level capital increase.

Shin Haeju (hjs0509@fntimes.com)

![[단독] 무신사 스탠다드 ‘산역사’ 이건오 퇴사…‘브랜드 정체성’ 전환점 맞나](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709134450047000b5b890e35c21123419294.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)