SK "HBM First" vs Samsung "Flexible Approach"

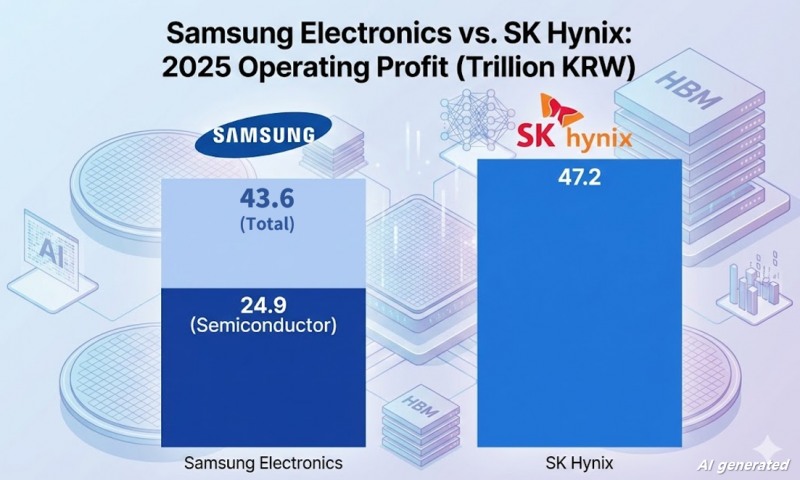

SK Hynix achieved KRW 97.1467 trillion in revenue and KRW 47.2063 trillion in operating profit last year. For the first time, it surpassed Samsung Electronics' profitability, which recorded KRW 333.6059 trillion in revenue and KRW 43.6011 trillion in operating profit during the same period. Samsung Electronics' DS (semiconductor) division posted an operating profit of KRW 24.9 trillion, approximately half that of SK Hynix. This is attributed to Samsung's late entry into the relevant market after losing HBM leadership in the first half of last year.

Rewritten with generative AI based on Korea Financial Times content / Source: Electronic disclosures from the Financial Supervisory Service and company earnings reports

이미지 확대보기

The two companies' business strategies for this year also differ subtly. SK Hynix emphasized stable HBM supply, stating that "customer trust is more important than short-term results."

In contrast, Samsung Electronics stated, "From a profitability perspective, we need to operate our product portfolio with a focus on servers rather than HBM," while adding, "We will operate flexibly and in a balanced manner rather than with concentrated supply."

Samsung Electronics also said, "For application markets other than servers, we will respond with a focus on high value-added products." Accordingly, memory supply shortages are expected to intensify in the small IT device market, including smartphones, tablets, and laptops, for budget models excluding AI-enabled flagship devices.

Competition to Secure HBM4

During this earnings conference call, attention focused on the status of the 6th-generation High Bandwidth Memory "HBM4" business, which can gauge memory technology competitiveness. This was because speculation emerged that Samsung Electronics would begin supplying HBM4 for the first time next month, leading some to interpret that SK Hynix, the No. 1 player in the HBM market, might be losing its leadership.

Samsung's 'Last Chance': Lee Jae-yong Pushes HBM4 as Make-or-Break Moment [KFT Topic]"Samsung Is Back," Chip Chief Declares, Eyeing Record Profit on HBM Recovery [KFT Topic]Lee Jae-yong and Chey Tae-won, Korea's 'Semiconductor Duo,' Head to China... What's the Status of Local Operations? [KFT Topic]SK Hynix's Five-President Team Set to Usher in KRW 100 Trillion Profit Era'AI Core' HBM4 Competition Strategy Poles Apart: Samsung Electronics 'Solo' vs SK Hynix 'Alliance'

Samsung Electronics explained, "HBM4 is scheduled to ship starting in February," and "Despite heightened performance requirements from major customers, we are smoothly proceeding with customer evaluation without redesign and are currently at the qual (quality test) completion stage." First, it confirmed the rumors were true through a specific shipment schedule. Mentioning "redesign," which SK Hynix is known to have experienced, is also interpreted as a remark targeting its competitor. Samsung Electronics went on to emphasize its technological competitiveness, stating, "We will supply HBM4E samples to customers in the middle of this year," and "We have already delivered HBM4E samples with hybrid bonding applied, and some are being planned for commercialization."

"Expanding Capital Expenditure"

Regarding this year's capital expenditure (CAPEX), both companies stated "we will invest more than last year" but refrained from mentioning specific figures. This is interpreted as reluctance to expose their strategies based on capital expenditure scale.However, SK Hynix mentioned that even this year, when a surge in revenue is expected, it would be able to maintain "capital expenditure in the mid-30% range as a percentage of revenue."

Samsung Electronics stated it would continue its shell-first strategy of preemptively constructing clean rooms and flexibly proceeding with capital expenditure according to market conditions. Most of this year's capital expenditure will also be executed on equipment to be installed in pre-secured new fab clean rooms.

Special Dividends on Record-Breaking Performance

Following last year's record-breaking performance that exceeded expectations, both companies decided to implement additional shareholder returns.SK Hynix plans to pay KRW 1,875 per share, adding KRW 1,500 in additional dividends to the existing fourth-quarter dividend of KRW 375 per share. The 2025 dividend per share is KRW 3,000, totaling approximately KRW 2.1 trillion. In addition, the company decided to cancel 2.1% of its existing treasury shares valued at over KRW 12 trillion to enhance existing shareholder value.

Samsung Electronics decided to pay KRW 566 per share by implementing an additional dividend of KRW 196 on top of the existing dividend of KRW 370 per common share. This also has the significance of meeting the government's "dividend tax separate taxation" requirement that shareholders of high-dividend companies can receive.

The company is also proceeding with its share buyback and cancellation plan, which applies through this year. Accordingly, the shareholder return scale for 2025 includes KRW 9.8 trillion in regular dividends, KRW 1.3 trillion in additional dividends, and KRW 6.6 trillion in treasury share buybacks and cancellations.

Gwak Horyung (horr@fntimes.com)

![지방이전에 뿔난 농협 노조 4000명 광화문 집결…"이전 강요 시 금융노조 총파업 불사" [막 오른 금융권 하투(夏鬪)]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607291713380470707c96e79780124111243152.jpg&nmt=18)

![송파구 '극동' 18평, 7.5억 오른 19.5억원에 거래 [일일 신고가]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260624115142011110dd55077bc212411124362.jpg&nmt=18)

![[그래픽 뉴스] 미국 증시 새로운 키워드 'MANGOS'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202607291740382069de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)