This infographic, originally published by Korea Financial Times, has been reconstructed using generative AI (Gemini).

이미지 확대보기

Caught in the dual bind of surging raw material prices and a slump in downstream industries, Hyundai Steel's financial soundness and profitability indicators have been stuck in a holding pattern for several years. The company has launched a head-on push to break out of the mire of weak earnings: boldly clearing out marginal assets with depressed utilization rates while pursuing new investment geared toward North American mobility and upgrading its portfolio around high-value-added products.

Operating Margin and Interest Coverage Ratio in "Free Fall"

Korea's steel industry has recently been suffering a "triple bind": an onslaught of cheap Chinese plate, a global demand slowdown, and a prolonged downturn in the construction sector, a key downstream industry. Hyundai Steel is no exception to these macro-level headwinds.Outwardly, the company maintains a strong corporate standing with total assets exceeding KRW 34 trillion. Internally, however, it has embarked on aggressive efficiency measures targeting marginal assets—halting operations at its Ulsan plant, where utilization had fallen, and shutting down some EAF lines at its Dangjin Steelworks.

The question is whether such slimming-down and structural-improvement efforts are translating into a genuine recovery in the company's underlying financial strength. Some in the market diagnose that while Hyundai Steel is maintaining its revenue scale at a certain level, the actual profit generated from its core business has shrunk substantially compared with the past.

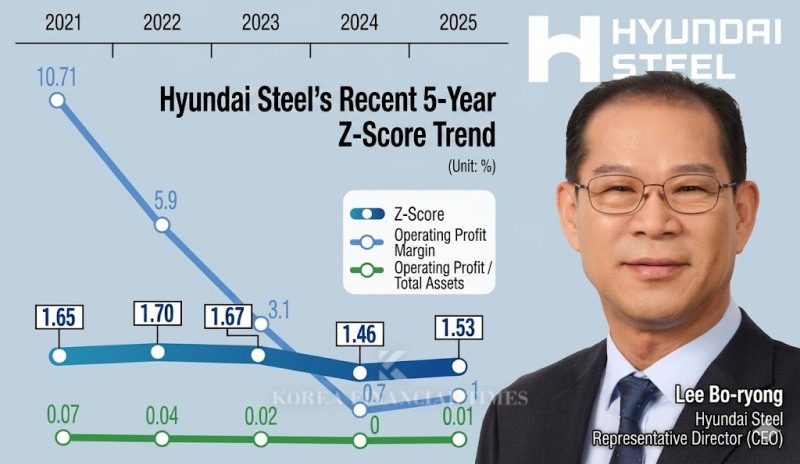

A look at Hyundai Steel's earnings trend over the past five years shows this declining profitability laid bare in the numbers. The company's operating margin reached 10.71% in 2021, when the steel cycle was at its peak. But it then plunged to 5.9% in 2022 and 3.1% in 2023, before finally falling to 0.7% in 2024.

In 2025, the margin rebounded slightly to 1.0% as the effects of aggressive asset slimming—the Ulsan plant suspension and the partial shutdown of Dangjin EAF lines—were reflected. Critics note, however, that this was closer to a defensive move achieved by cutting fixed costs than to genuine structural improvement.

This low-profitability structure is starkly evident in the interest coverage ratio, which indicates a company's ability to service its debt. Hyundai Steel's interest coverage ratio, which boasted a solid 13.9x in 2021, plummeted to 0.6x in 2024 as core-business margin compression peaked.

Six Years Locked Away: What Will Hyundai Steel Decide on Its Treasury Shares at This AGM?POSCO Holdings Stock Soars 68% in Two Months on Wings of Non-Steel BusinessLIG D&A, Hanwha Systems Enter Full-Scale Rivalry as Defense AI Battle Reaches the BoardroomKorea's Four SI Firms Race to Own the Humanoid Operating System

Through belt-tightening management in 2025, the company managed a modest defense at 0.9x, but its interest coverage ratio has now stayed below 1x for two consecutive years. As a state in which a single year's operating profit cannot even fully cover interest payments persists, concerns are deepening over a vicious cycle in which the company—far from securing its own funds for future growth drivers—must rely on external borrowing.

Financial Soundness Eaten Away by a "Paralyzed Core Business"

As the entrenchment of a long-term low-profitability structure has been compounded by the shock of a quarterly loss, the market is turning its attention to objective financial-soundness indicators that can comprehensively diagnose Hyundai Steel's potential distress risk.Hyundai Steel's first-quarter operating profit on a consolidated basis was KRW 15.7 billion, swinging to a profit from an operating loss of KRW 19.0 billion in the same period last year. On a separate (standalone) basis centered on the core steel business, however, the operating loss came to KRW 72.5 billion, with the deficit actually widening from the KRW 56.1 billion loss in the same period last year.

This weakening of fundamental strength has triggered a warning light in the Altman Z-Score, a financial measure that predicts a company's likelihood of bankruptcy. According to "THE COMPASS," the proprietary artificial intelligence (AI) data platform built in-house by the Korea Financial Times, Hyundai Steel's Z-Score recorded 1.65 in 2021, 1.70 in 2022, and 1.67 in 2023, before falling to 1.46 in 2024. While it rebounded slightly to 1.53 in 2025, it has remained below 1.81—the threshold typically deemed to indicate a high level of financial risk—for five consecutive years.

The decisive cause of Hyundai Steel's Z-Score being locked in low territory aligns with the aforementioned plunge in operating margin and interest coverage ratio. This is because the "operating profit / total assets" indicator, one of the five variables that make up the Z-Score model, declined sharply.

Hyundai Steel's total assets shrank from around KRW 37.0423 trillion in 2021 to around KRW 34.4423 trillion in 2025 as it went through its efficiency drive, but over the same period operating profit plummeted by roughly 90%, from KRW 2.4475 trillion to around KRW 219.2 billion.

As a result, the operating-profit-to-total-assets figure shriveled from 0.07 in 2021 to 0.00 in 2024 and 0.01 in 2025. This means that, relative to the weight class of its assets, the substance of its core business has been effectively paralyzed.

That said, the market interprets this prolonged Z-Score weakness not as a sign that the company faces an imminent bankruptcy crisis, but rather as a product of the chronic valuation slump brought on by core-business margin compression. Apart from the warning light, the company's actual short-term solvency and liquidity defenses remain firmly intact.

As of 2025, Hyundai Steel holds current assets amounting to KRW 11.3175 trillion, and it has secured near-term financial stability by tightly managing current liabilities at around KRW 7.4105 trillion.

In the end, while there are no fears of a collapse in terms of fundamental strength, this is why critics point out that the decline in core-business profitability is proving a stumbling block, leaving the company hard-pressed to lift its market valuation.

The Paradox of "No. 1 in Electric Arc Furnaces"

So what is the key link in the profitability deterioration that has so battered Hyundai Steel's internal health? Paradoxically, the cause begins in the very "electric arc furnace" segment that was Hyundai Steel's greatest strength and identity.Hyundai Steel has boasted a balanced portfolio with annual capacity of 12 million tons via the blast furnace method and 12 million tons via the EAF method. The EAF, in particular, was regarded as a key weapon in the decarbonization era, as it draws molten iron by recycling scrap metal and can therefore cut carbon emissions by roughly 20% or more compared with the blast furnace method.

The problem is that as global steelmakers simultaneously declared EAF expansion, a war broke out to secure high-quality ferrous scrap, the key raw material. With demand exploding while supply remained limited, ferrous scrap took on the character of a strategic asset.

According to Hyundai Steel's earnings materials, the price of "Heavy A," a premium grade of ferrous scrap, surged more than 12%, from USD 355 per ton in March 2025 to USD 397 in April this year. This ran directly counter to the path of traditional blast furnace inputs over the same period, with coking coal (-21%) and iron ore (-3%) prices stabilizing downward.

To lower its cost burden, Hyundai Steel has resorted to stopgap measures such as recently raising the delivery prices for ferrous scrap supplied to its Incheon plant and Dangjin Steelworks by KRW 15 per kilogram each, but this fed straight through to higher input costs.

The bigger problem is that it is impossible to reflect these increased costs in product prices. The main buyers of Hyundai Steel's EAF products are the domestic construction industry, including its affiliate Hyundai Engineering & Construction. Yet due to the prolonged construction downturn, the distribution price of H-beams (USD 1,050 → USD 1,080 per ton) and the benchmark price of rebar (USD 810 → USD 830) rose only modestly, by around 2–3%.

In the end, with raw material costs soaring while selling prices marched in place, Hyundai Steel took a direct hit in the form of a standalone swing to loss in the first quarter of this year. The company has, in effect, been trapped in a paradoxical structure in which a transitional alternative meant to serve decarbonization is instead eating away at its earnings.

A KRW 8.5 Trillion North American "Bet"

To overcome the structural limitation of EAF margin compression at home, Hyundai Steel is deploying a bold strategy of "selection and concentration" on the global stage. It is channeling the funds and capabilities secured by clearing out low-profitability marginal assets at home toward the North American eco-friendly steel market, a future core growth driver.Hyundai Steel is currently teaming up with POSCO and Hyundai Motor and Kia to push for the construction of an integrated EAF steel mill in Louisiana, USA, with a total investment of USD 5.8 billion.

This mega-project, targeting commercial production in 2029, could weigh on financial liquidity and the debt ratio in the short term by increasing the burden of initial capital expenditure (CAPEX).

Over the long term, however, the prevailing view in the industry is that it is an essential building block for pre-emptively responding to the U.S. Inflation Reduction Act (IRA) while gaining first-mover advantage in the North American eco-friendly automotive steel-sheet market.

The steel industry and securities analysts assess that for this large-scale North American investment to lead not merely to outward expansion but to a medium- to long-term re-rating of corporate value, the company's drive to reshape its portfolio toward high-value-added, eco-friendly product lines must gather considerably more speed.

Hyundai Steel has made expanding the share of high-value-added steel sheet aimed at global automakers its top priority and is accelerating its push into overseas markets.

The plan is to diversify its automotive steel-sheet supply chain—currently concentrated on the internal group market such as Hyundai Motor and Kia—toward global and local automakers, timed to the completion of its Steel Service Center (SSC) in Georgia and the Louisiana project. Securing independent pricing-negotiation power through this is expected to be the key watershed for defending profitability in the North American market going forward.

In addition, the company is fleshing out a strategy to break away from a business structure centered on commodity rebar and section steel—whose earnings are highly volatile in tandem with construction conditions—and to gain first-mover advantage in high-value-added energy infrastructure markets such as the recently fast-growing AI data center sector and the global expansion of power grids.

The plan is to target niche markets by increasing supply of ultra-heavy, high-strength structural materials tailored to AI data centers—where demand is surging amid explosive power consumption—and of specialty steel for energy infrastructure. This aligns with a strategy of filling the space cleared of inefficiency through the slimming of domestic marginal assets with high-margin, high-value-added steel supply capacity.

One securities industry official forecast: "To overcome the raw material price volatility that arises in the course of the carbon-neutral transition, securing margins through product sophistication is essential," adding, "Ultimately, how quickly Hyundai Steel can deliver visible results in the early stabilization of its new North American base and in securing independent order volumes from global automakers beyond Hyundai Motor and Kia will determine the long-term direction of its corporate value."

Jeong Chaeyun (chaeyun@fntimes.com)

!['생산적 금융 ISA' 신설…이자·배당소득 전액 비과세 [2026 세제개편안]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260803214921016190179ad4390711823514132.jpg&nmt=18)

![한의사가 '셀프 진료'부터 '유령 환자' 행세까지…자동차보험 악용 심각 [경상환자 8주룰 도입 초읽기]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202608040715370165908a55064dd1124111243152.jpg&nmt=18)

![[그래픽 뉴스] 미국 증시 새로운 키워드 'MANGOS'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202607291740382069de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)