Steeling Against the Slump: Subsidiaries Hold the Line

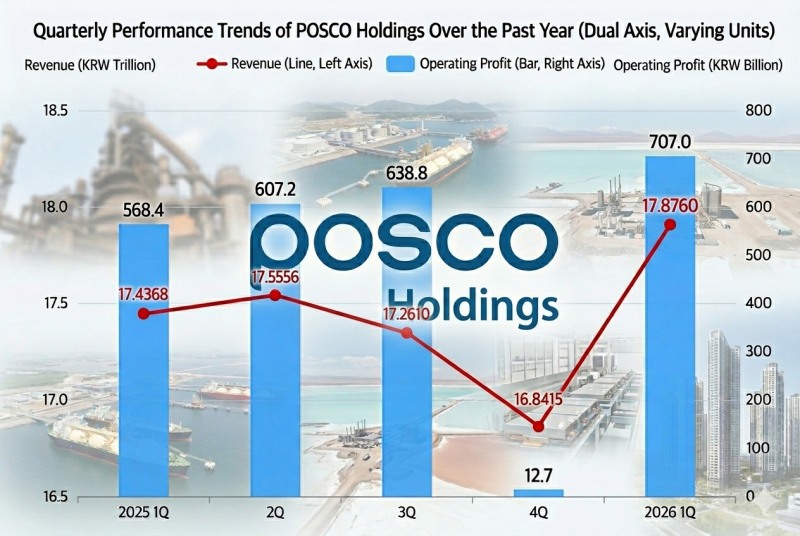

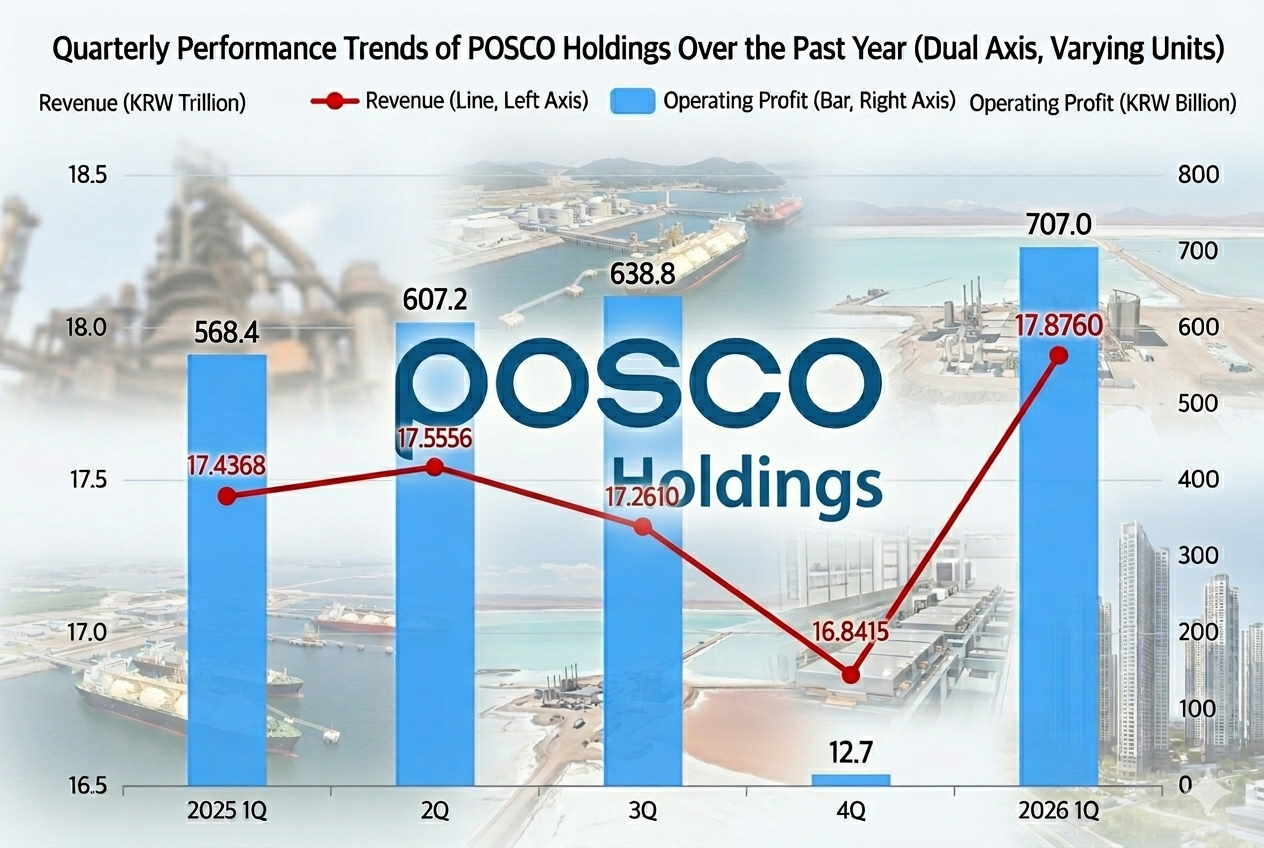

POSCO Holdings recorded consolidated revenue of KRW 17.876 trillion and operating profit of KRW 707 billion for the first quarter of this year, representing increases of 2.5% and 24%, respectively, compared to the same period a year earlier.The steel segment faced limited profitability amid sluggish global demand and cost pressures, but steep earnings improvements at non-ferrous metal and energy affiliates drove the group's overall growth.

POSCO International was the standout performer, delivering a surprise earnings beat and serving as the most pivotal contributor to the group's overall results. POSCO International's first-quarter operating profit, disclosed on the same day, came in at KRW 357.5 billion — a 32% surge year-on-year that exceeded brokerage consensus by more than 10%. The outperformance was attributed to increased output at Australia's Senex Energy, as well as the operation of a high-margin portfolio in the LNG and crude oil trading businesses.

This infographic, originally published by Korea Financial Times, has been reconstructed using generative AI (Gemini). / Source = POSCO Holdings

이미지 확대보기

The advance of the secondary battery materials segment was equally noteworthy. POSCO Future M successfully returned to profitability through expanded sales of high value-added products, while POSCO Argentina and POSCO Pilbara Lithium Solutions significantly narrowed their operating losses, supported by rising lithium prices and higher production volumes.

Notably, POSCO Argentina recorded its first monthly operating profit in March, signaling a full-fledged shift to earnings generation in the second quarter. POSCO E&C also bolstered the group's overall earnings capacity as major domestic and overseas construction projects returned to normal progress and overseas subsidiaries — including its Zhangjiagang entity in China — increased their profit contribution.

The strong performances by these subsidiaries demonstrate that POSCO Holdings' earnings structure has broken free from its single-pillar dependence on steel and has entered a genuinely diversified orbit. Analysts interpret this as evidence that the strategy of reducing exposure to the highly volatile steel cycle while pivoting the portfolio toward resources and energy is delivering tangible results.

POSCO Holdings Finds New Revenue Engine in Energy, but Debt Shadow DeepensPOSCO Holdings Completes 6% Share Cancellation Pledge — But Core Profit Recovery Remains the Missing PieceSix Years Locked Away: What Will Hyundai Steel Decide on Its Treasury Shares at This AGM?Korea's Four SI Firms Race to Own the Humanoid Operating System

After Confirming Results, the Rally Accelerates: China Output Cuts and Price Hike Expectations Priced In

Market attention is now squarely focused on the sharp share price reaction that has followed the solid earnings confirmation. As of the closing price on May 7, POSCO Holdings shares stand at KRW 535,000. What is particularly striking is the pace of the ascent: having retreated to KRW 318,000 as of March 4, the stock has surged 68.2% in just over two months.The market views the current price as already discounting catalysts well beyond the confirmed first-quarter scorecard — namely, second-half product price increases and the commercial launch of lithium operations. Observers say signals are emerging that the steel industry, after an extended slump, has entered a genuine turnaround.

Photo courtesy of POSCO Holdings

Above all, the intensification of global supply-demand imbalances has served as a powerful trigger lifting the share price. Iran, a major Middle Eastern steel producer, recently decided to impose a blanket ban on exports of steel slabs and plates through the end of next month, heightening supply tension across global supply chains.

Adding to the positive backdrop, China — the world's largest steel producer — officially confirmed that crude steel output last year fell 4.4% year-on-year to 961 million tons, making its production-cut stance unmistakably clear. As supply-side bottlenecks sharpened, POSCO Holdings appears to have reclaimed pricing leadership in the market.

The company raised prices for hot-rolled and cold-rolled steel sheet by KRW 50,000 per ton in the second quarter, beginning to pass rising costs through to product prices. Hyundai Steel and other industry peers have followed suit, sending a clear signal of price normalization across the sector.

Lithium Business Takes Shape: Corporate Value Restructured Around Secondary Battery Materials

The other key variable that prevents POSCO Holdings from being pigeonholed as a conventional steel stock is lithium.This year, with the first-phase plant at the Hombre Muerto salar in Argentina entering commercial operations in the first half, the company has established a lithium hydroxide production system capable of generating 25,000 tons annually — enough to supply batteries for approximately 600,000 electric vehicles.

A panoramic view of the Hombre Muerto salt flat in Argentina. / Photo courtesy of POSCO Holdings

이미지 확대보기

When construction at Australia's Greenbushes mine and the expansion of the Gwangyang Plant 2 are completed, the group's total lithium production capacity will expand to 93,000 tons — a level sufficient to rank the company among the top 5 to 10 lithium producers globally.

Major investment institutions, including Meritz Securities, are currently valuing POSCO Holdings' lithium business at approximately KRW 8.2 trillion and are leading a broad-based valuation re-rating.

Ultimately, the sharp surge in POSCO Holdings' share price is being interpreted as the convergence of a near-term tailwind — recovery in steel — and a medium-to-long-term momentum driver: the materialization of its lithium business. Having long languished in deeply undervalued territory at a price-to-book ratio (PBR) of around 0.5x, POSCO Holdings is now expected to command a premium as a materials company.

"If the first-quarter results confirmed the company's fundamental staying power," said one industry official, "the share price is now racing toward the future. As the point approaches when the lithium value chain begins translating into actual cash flows, the re-rating of POSCO Holdings' corporate value will only accelerate further."

Jeong Chaeyun (chaeyun@fntimes.com)

![[단독] 조좌진 前 롯데카드 대표, 하나투어 신임 대표 내정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20251113170440010389efc5ce4ae1439255137.jpg&nmt=18)

![‘포스트 서정진’ 지배구조 딜레마…멈춰 선 합병에 ‘애나그램’ 만지작 [셀트리온의 성장통 ③]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260626215954009600dd55077bc212411124362.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)