What is the reality? An examination of Hyundai Motor’s detailed profitability metrics suggests that meeting the union's demands would be unrealistic. Hyundai Motor is leading large-scale future investments for the group, meaning its earnings performance does not align with its actual cash flow. Furthermore, rising internal and external uncertainties, including U.S. tariffs, are deteriorating profitability. The situation is clearly turning unfavorable for Hyundai Motor.

Shareholder Dividends of KRW 2.6 Trillion vs. Performance Bonuses of KRW 3 Trillion

The labor and management of Hyundai Motor held a preliminary meeting on May 6 to begin this year’s collective wage agreement negotiations. With major South Korean conglomerates like Samsung Electronics currently engaged in intense tugs-of-war over performance bonus increases, the demands from Hyundai Motor’s union—historically known for its hardline stance—have drawn significant attention.

Prior to the negotiations, the union submitted a list of demands to management. This included an increase in the monthly base salary by KRW 149,600 (excluding automatic step-ups), a performance bonus equivalent to 30% of last year’s net profit, the implementation of a fully fixed monthly salary system, an increase in regular bonuses from 750% to 800%, a reduction in working hours without intensifying labor, an extension of the retirement age linked to the national pension eligibility age (up to 65 years old), and the hiring of new personnel.

Similar to last year, the core issues in this year's collective bargaining negotiations at Hyundai Motor revolve around wage and performance bonus increases driven by record-high performance, retirement age extensions aligned with government policies, and job security amid the introduction of robots and artificial intelligence (AI). Industry observers project that this year's negotiations will once again face severe friction between labor and management.

Among these issues, the demand for performance bonuses—a topic that has recently flared up between labor and management at other major conglomerates like Samsung Electronics—has become the biggest talking point. Once performance bonus standards are set, they are difficult to adjust downward, which can pose a significant financial burden on companies depending on industry conditions.

This is precisely why Samsung Electronics has maintained a hardline standoff against its union’s demand for a performance bonus equal to 15% of the previous year's operating profit. Samsung Electronics shareholders have also voiced concerns over the union's excessive bonus demands.

Shareholder Returns or Succession Strategy? The Dual Purpose Behind Hyundai Motor and Kia's Payout PoliciesHyundai Motor Shifts Gear: From Automaker to Advanced Mobility CompanyBeyond Atlas: Hyundai Bets on Collaborative Robots to Pave Way for Humanoid FutureFrom Carmaker to Logistics Platform: Kia's Robotics-Fueled ReinventionTesla's Humanoid Rival Has Arrived — Boston Dynamics Eyes $70 Billion Valuation [K-Humanoid Wars, Part 1]

Hyundai Motor faces a similar predicament. According to the union’s proposal, Hyundai Motor would need to allocate approximately KRW 3 Trillion—30% of its roughly KRW 10 Trillion net profit last year—for performance bonuses. This amount exceeds the total dividend payout of approximately KRW 2.6 Trillion that Hyundai Motor returned to shareholders last year.

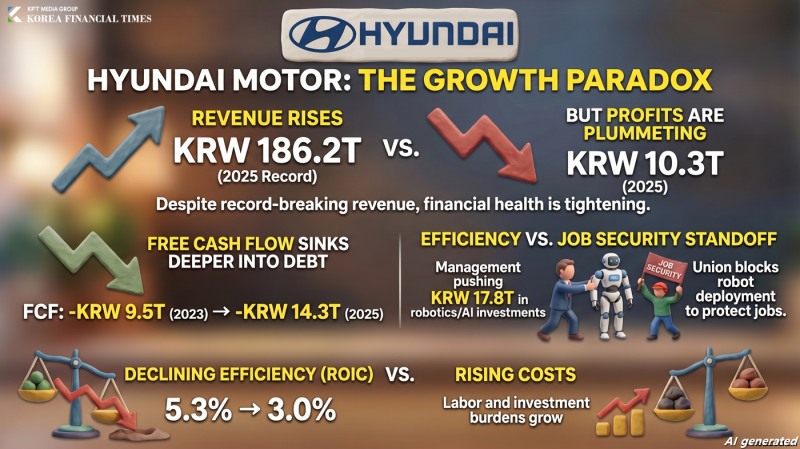

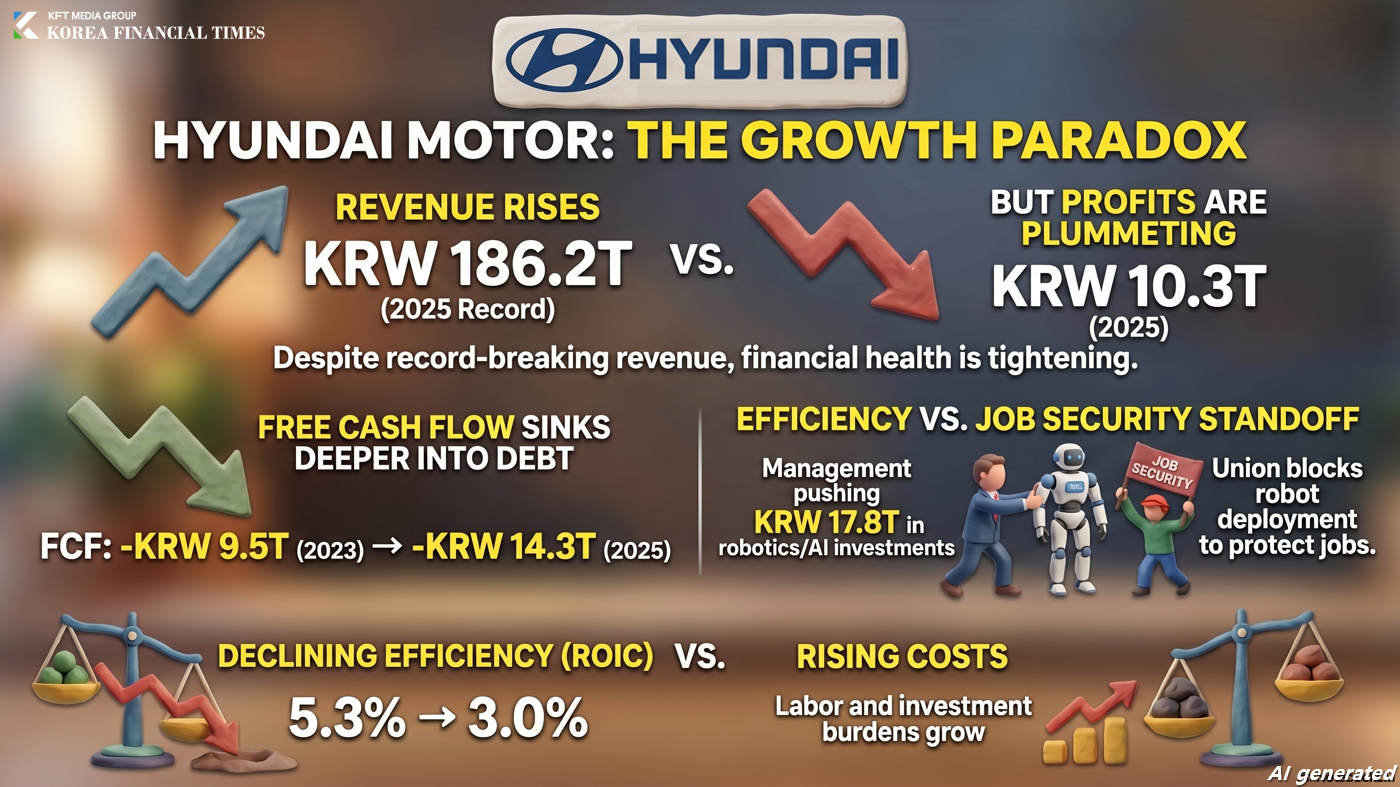

The problem is that while Hyundai Motor recorded historic revenue, its net profit is on a downward trend. Hyundai Motor’s annual revenue over the past three years has increased consecutively, from KRW 162.6636 Trillion in 2023 to KRW 175.2312 Trillion in 2024, and KRW 186.2545 Trillion in 2025. Conversely, net profit—the basis for the performance bonuses—increased from KRW 12.2723 Trillion in 2023 to KRW 13.2299 Trillion in 2024, but plummeted to KRW 10.3648 Trillion last year due to factors such as U.S. tariffs.

Declining Cash Flow and the Burden of Future Investments

Analysts point out that accepting the union's demands is practically impossible, not only because of earnings performance but also when looking at Hyundai Motor’s detailed cash flow and investment efficiency metrics. While profitability has weakened, the burden of funding future investments, such as autonomous driving, remains high.

First, looking at Hyundai Motor’s cash flow from operating activities over the past three years, despite breaking historical revenue records, it turned into a net outflow of minus KRW 2.5188 Trillion in 2023, with the deficit widening to minus KRW 5.6616 Trillion in 2024 and minus KRW 5.9913 Trillion in 2025.

Consequently, Hyundai Motor’s free cash flow (FCF) also sank deeper into negative territory, recording minus KRW 9.5895 Trillion in 2023, minus KRW 13.723 Trillion in 2024, and minus KRW 14.358 Trillion in 2025. This indicates that the cash generated from operations was insufficient to cover essential expenditures, including interest, corporate taxes, and investments.

In fact, Hyundai Motor's annual operating profit has been on a downward trend after peaking at KRW 15.1269 Trillion in 2023, dropping to KRW 14.2396 Trillion in 2024 and KRW 11.4679 Trillion in 2025. Operating profit for the first quarter of this year was also tallied at KRW 2.5147 Trillion, down 30.8% year-on-year due to increases in warranty expenses and labor costs, as well as the impact of U.S. tariffs.

Despite its murky profitability outlook for this year, Hyundai Motor plans to spend approximately KRW 17.8 Trillion on future investments such as autonomous driving and robotics. This volume nearly equals the KRW 18 Trillion in cash and cash equivalents held by the automaker. As the flagship entity of the group, Hyundai Motor bears the largest share of funding for future technology investments, putting it under greater financial pressure compared to other affiliates.

For instance, Motional, an autonomous driving joint venture established in 2020 with a total investment of KRW 2.5 Trillion, saw participation from Hyundai Motor, Kia, and Hyundai Mobis at a ratio of 2.6 to 1.4 to 1, respectively. Furthermore, in the KRW 1.3 Trillion paid-in capital increase for Boston Dynamics in August last year, Hyundai Motor contributed the largest share at KRW 362.6 Billion, followed by Kia (KRW 223.4 Billion) and Hyundai Mobis (KRW 146.5 Billion).

Union Blocking the Introduction of Robots

Other union demands, such as the introduction of a fully fixed monthly salary system and the extension of the retirement age, could act as risks to Hyundai Motor's corporate value in the long term.

These demands were put forward by the union to secure employment stability in response to the introduction of robots and AI. Previously, the union took a hardline stance regarding the deployment of the humanoid robot 'Atlas' to Hyundai Motor's production lines, stating, "We oppose the deployment without labor-management consultation."

Hyundai Motor has invested vast amounts of capital to transition into a global robotics company, including the acquisition of Boston Dynamics. However, until last year, these efforts remained in the research phase without delivering tangible results, leading to criticism over low investment efficiency.

In fact, looking at the trend of Hyundai Motor’s return on invested capital (ROIC) over the past three years, it declined annually from 5.3% in 2023 to 4.19% in 2024 and 3.0% in 2025. ROIC is a metric that shows how efficiently a company generates profit relative to the capital it has invested; a lower figure signifies declining investment efficiency.

From Hyundai Motor's perspective, if the union’s demands are met, it will inevitably disrupt its plans to improve production efficiency and cut costs through robots like Atlas. In the securities market, one of the driving forces behind Hyundai Motor’s stock price rise following the unveiling of Atlas has been anticipation over enhanced process efficiency and the mitigation of labor cost risks through robotics.

"Hyundai Motor’s collective bargaining is a complex challenge that goes beyond simple wage negotiations, as it is intertwined with guaranteeing job security in the era of robotics," a high-ranking official in the automotive industry said. "Both labor and management must engage in in-depth discussions, looking not only at superficial financial numbers but also at detailed financial metrics and the enhancement of future competitiveness."

Kim JaeHun (rlqm93@fntimes.com)

![‘후계 0순위·지분 0%’ 코오롱 4세 이규호의 고민 [기업지배구조 보고서]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260704000520063140dd55077bc212411124362.jpg&nmt=18)

![[기자수첩] 농협 이전, 지방부흥 만능키 아냐](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260704005258006900dd55077bc212411124362.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)