Photo: SK Chairman Chey Tae-won (left), and Samsung Electronics Chairman Lee Jae-yong

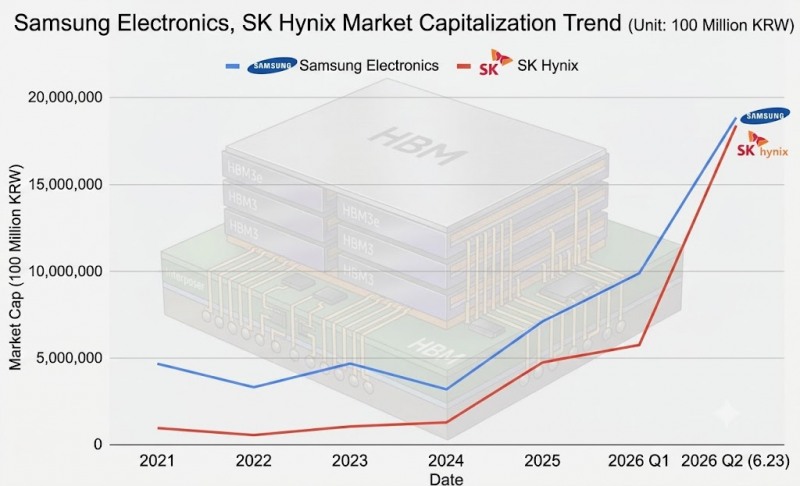

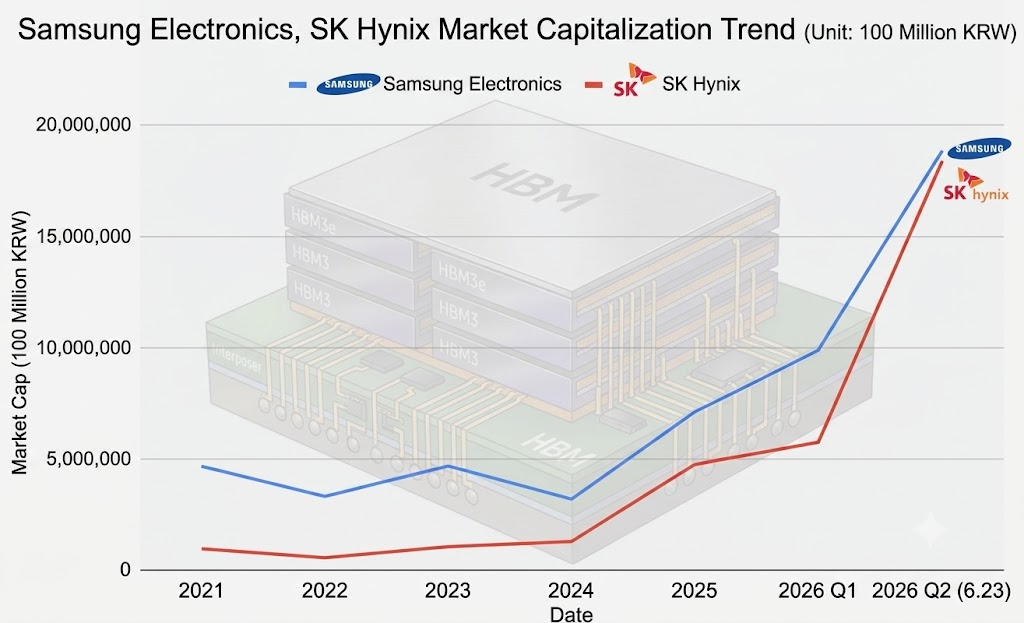

As of the closing price on the 22nd, SK hynix's market capitalization stood at KRW 2,080 trillion, surpassing Samsung Electronics' KRW 2,067 trillion to claim the No. 1 spot among individual listed stocks. Samsung Electronics pushed back through a statement, saying that "a company's market cap is the total sum of share value including both common and preferred stock." By this measure, Samsung Electronics' market cap, including preferred shares, stands at KRW 2,252 trillion — still No. 1. Nonetheless, the market appears to be paying greater attention to the symbolic significance of the No. 1 stock changing hands for the first time in 27 years since 1999.

As recently as the end of 2023 — just two years and six months ago — Samsung Electronics' market cap (common stock) was more than 4.5 times that of SK hynix. The gap between the two narrowed sharply after the end of the first quarter of this year, before reversing for the first time ever. What was it that allowed SK hynix to catch up with Samsung Electronics' market cap so abruptly?

This chart, originally published by Korea Financial Times, has been reconstructed using generative AI.

이미지 확대보기

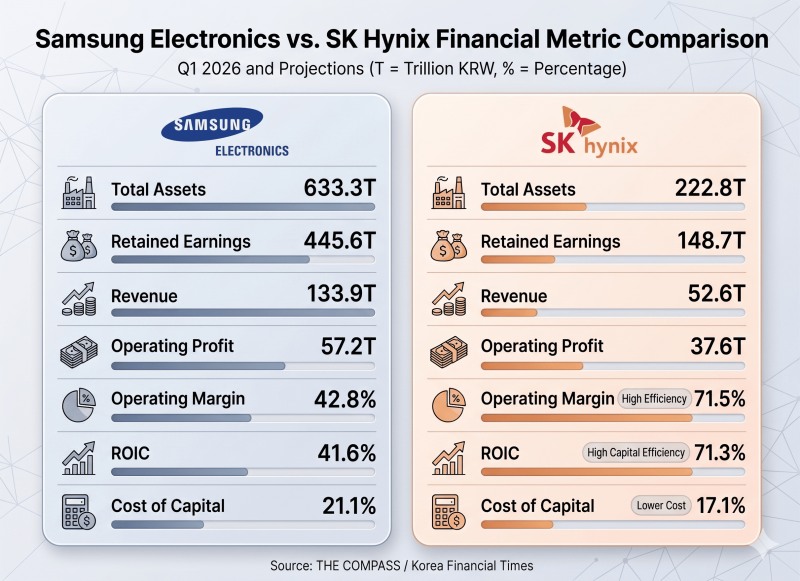

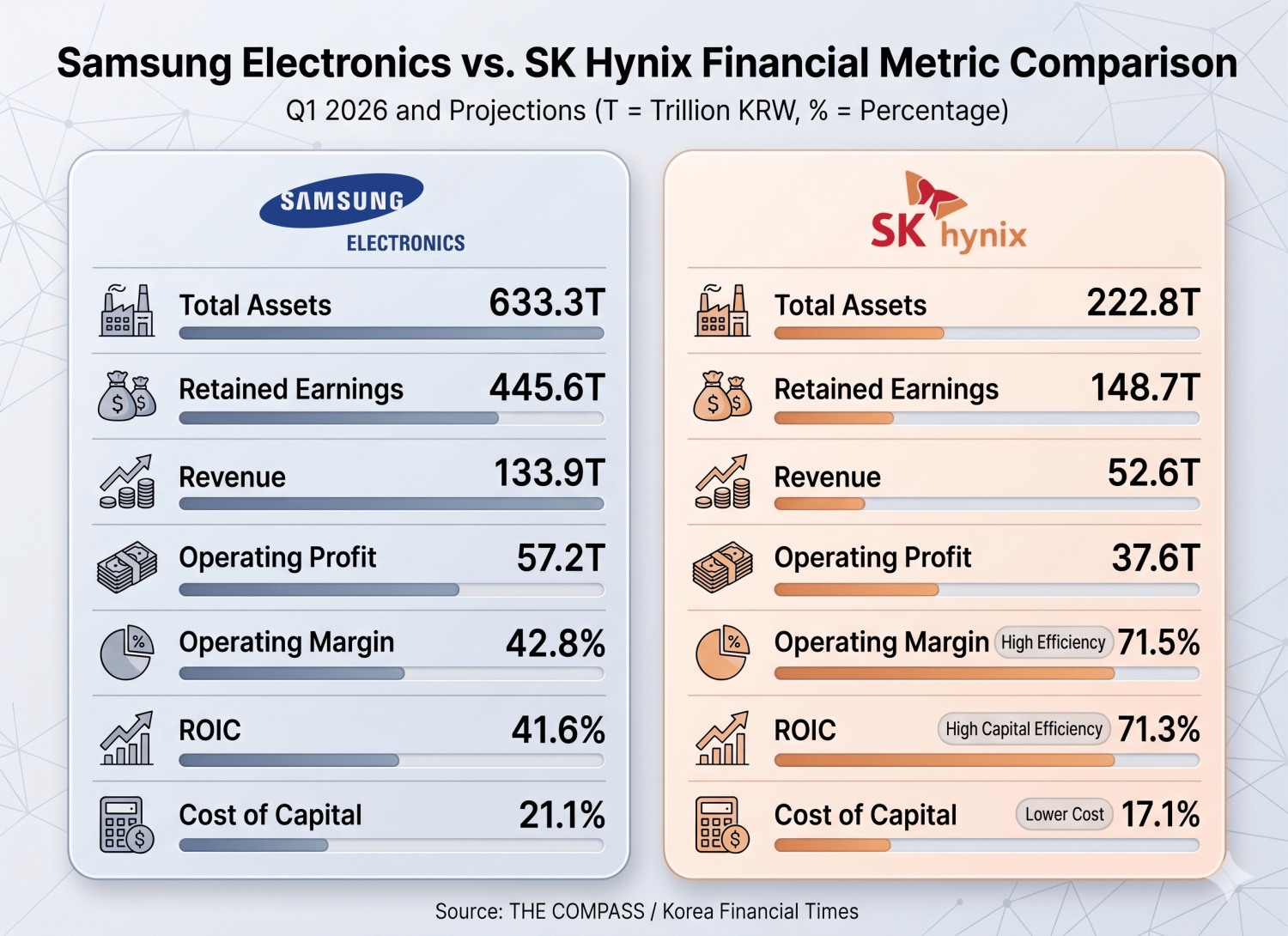

There is no dispute that Samsung Electronics boasts overwhelming scale compared with SK hynix. As of the end of the first quarter of this year, Samsung Electronics' total assets are 2.8 times larger and its revenue roughly 2.6 times greater. Its retained earnings — the funds accumulated from the profits earned through corporate activity — are also three times larger.

The premium SK hynix has received from the market is capital efficiency. Even with less capital invested, it generates returns at a far higher rate of efficiency.

According to THE COMPASS, the AI data platform built in-house by Korea Financial Times, SK hynix's projected return on invested capital (ROIC) for this year, based on first-quarter 2026 results, stands at 71.3%, overwhelming Samsung Electronics' 41.6%. The spread (ROIC − WACC) — which represents the actual profit after excluding the cost of raising capital (weighted average cost of capital, WACC) — reaches 54.1% for SK hynix, more than 2.5 times higher than Samsung Electronics' 20.6%.

In calculating invested capital (IC), the denominator of ROIC, this platform applies a conservative standard that does not exclude short-term financial instruments and the like. This is done to gauge a company's actual capacity to utilize its funds. Samsung Electronics, which holds an enormous volume of non-operating financial assets, faces the disadvantage of having its capital efficiency assessed as relatively lower.

Samsung Electronics Surpasses 30% NAND Market Share, Bolsters 'Super-Gap' Lead Through NVIDIA AllianceSK hynix Eyes KRW 40 Trillion in Q1 Operating Profit — Is AI Ushering in a Long-Term Boom?Once Samsung's Cash Cow, Galaxy Now Teeters on the Brink of a LossSK Hynix Weighs Growth Over Governance in Treasury Share Strategy [Treasury Share Report]Exynos Reborn: How Samsung Is Betting Its Chip Future on On-Device AI

In addition, the cost of capital (WACC) was derived using a free cash flow (FCF) reverse-calculation method. For Samsung Electronics' projected 2026 FCF of KRW 88.4 trillion to justify its market cap as of the end of the first quarter, the company must prove a high average annual growth rate of 27.3% over the next 10 years. By contrast, the average annual growth rate the market demands of SK hynix under the same standard was set at 22.8%, lower than that of Samsung Electronics.

Ultimately, SK hynix's profit-generating capacity, which far exceeds what the market requires, is interpreted as the key factor explaining its recent runaway share-price gains and market-cap premium.

SK hynix adds strategic momentum to its earnings cycle

The indicators above reflect annual projections based on first-quarter financial data this year.In the first quarter, the price of commodity DRAM exceeded that of high-bandwidth memory (HBM), creating a favorable environment for Samsung Electronics, which has a large scale and high proportion of commodity semiconductors.

Moreover, Samsung Electronics' device (DX) division — including smartphones and home appliances — tends to peak in the first quarter and decline from the second through fourth quarters.

As a result, SK hynix's capital efficiency is expected to stand out even more from the second quarter onward.

SK hynix's listing of American depositary receipts (ADRs) in the U.S., projected to be completed in August, is also analyzed as contributing to the share-price rise.

Expectations are growing not only for inflows of global passive funds but also for a re-rating of the company's value. According to Hanwha Investment & Securities, SK hynix's 12-month forward price-to-earnings ratio (PER) stands at 6.6 times — undervalued compared with U.S.-based Micron, which commands more than 10 times.

Chey Tae-won, chairman and owner of SK Group, has also been actively promoting SK hynix's future strategy, citing specific figures. This also has the effect of lowering the risk of future uncertainty for investors. Attending Computex 2026, Taiwan's largest IT expo, earlier this month, Chairman Chey said, "Driven by surging demand for AI memory, shortages of memory such as HBM will persist until 2030," adding, "We will expand our total wafer production capacity to double the current level."

For Samsung Electronics, success of HBM4 is the key

Samsung Electronics' relatively low capital efficiency stems from the existence of low-margin business units such as non-memory (System LSI and Foundry) and the DX division. Over the long term, once the AI era fully arrives, a diversification strategy that reduces dependence on memory could contribute to enhancing corporate value. In the current AI memory super-cycle phase, however, attention is concentrating on SK hynix, which has maximized profitability by simplifying its business structure.For now, Samsung Electronics is focused on securing market leadership through HBM4 (sixth generation). Samsung Electronics' HBM4, which combines its cutting-edge 10-nanometer-class 1c DRAM with a 4-nanometer foundry process, began the world's first mass-production shipments in February. Samsung Electronics still faces the task of proving whether its recovery in HBM4 technological capability translates into actual earnings.

Gwak Horyung (horr@fntimes.com)

![[DCM] 한국금융지주, 최대 4000억 조달…'자회사 호실적' 속 커지는 '차입 부담'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260623090230031360141825007d12411124362.jpg&nmt=18)

![[DQN] 주가 하락 방어·지속 상승···위기에 강한 금융지주는 [금융지주 밸류업 점검]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260622001546057790b4a7c6999c121131189150.jpg&nmt=18)

![[DQN] 정일선號 광주은행 평균신용점수·취약차주금리···가계 포용금융 '우수' [은행권 금리 전략]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260622195051049730b4a7c6999c121131189150.jpg&nmt=18)

![이찬진 금감원장 “금융 지배구조 개선안 최종안 보고…7월 전 나올 것” [금감원장 월례 기자간담회]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202606221510430121005e6e69892f211217229227.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)