Samsung Electronics HBM3E 12-layer product image. / Photo = Samsung Electronics

Additionally, Samsung Electronics emphasized that mass production plans for its latest products, including HBM4 (6th generation), are proceeding smoothly in line with customer production schedules.

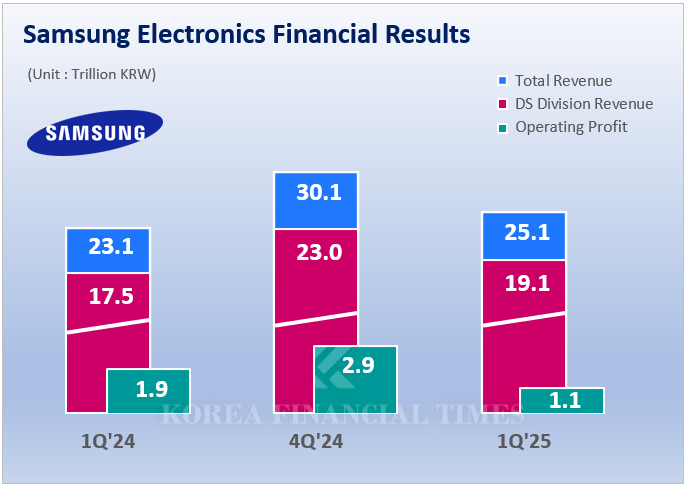

On April 30, Samsung Electronics announced its first-quarter results, reporting consolidated sales of KRW 79.14 trillion and operating profit of KRW 6.7 trillion. Sales surpassed market forecasts, marking the company’s highest-ever quarterly revenue.

However, the semiconductor division, including HBM, saw its performance decline despite expanded sales of server DRAM, primarily due to decreased HBM sales. The Device Solutions (DS) division, responsible for the semiconductor business, recorded first-quarter sales of KRW 25.1 trillion and operating profit of KRW 1.1 trillion. While sales rose by about KRW 2 trillion year-on-year, operating profit fell by approximately KRW 800 billion.

The DX division, buoyed by strong sales of the Galaxy S25, offset the DS division’s sluggish performance. The DX division posted first-quarter sales of KRW 51.7 trillion and operating profit of KRW 4.7 trillion.

Nevertheless, profitability in the second quarter is uncertain as the Galaxy S25 effect wanes and the smartphone market enters a seasonal downturn. This makes a rebound in the DS division, the other pillar of Samsung Electronics’ business, all the more urgent.

The key to the DS division’s recovery is undoubtedly securing competitiveness in HBM. In the first quarter, Samsung Electronics focused on redesigning the 12-layer HBM3E in response to customer demands. Kim Jae-joon, Executive Vice President and Head of the Memory Business at Samsung Electronics, explained during the earnings conference call, “There was some impact from delayed supply due to the HBM3E redesign and other factors”.

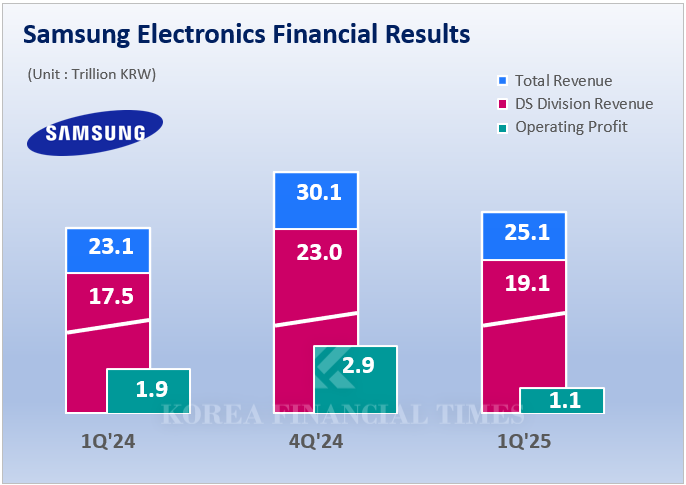

Samsung Electronics DS Division’s First-Quarter Performance Trend Over the Past Year. / Data = Samsung Electronics

이미지 확대보기

'Humanoid Pioneer' Oh Jun-ho Tasked with Nurturing Samsung Electronics' Future Robot BusinessSamsung Electronics' New CFO Park Soon-chul...Breaking through uncertainty 'special assignment'Lee Jae-yong’s 3 Picks Transforming Samsung Electronics : 'Automotive Electronics, Displays, and Robotics'Will Samsung Electronics Unlock Its Treasury After 8 Years? Potential for Mega M&ASamsung Electronics 'Trapped in the KRW 50,000 Swamp'... "Vows to Secure Competitiveness in AI and Robotics"

The company also revealed its mass production plans for the latest HBM4 product line. Samsung Electronics aims to begin mass production of standard HBM4 and HBM4E, as well as custom HBMs tailored to customer needs, in the second half of this year as scheduled.

Kim Jae-joon said, “The sixth-generation HBM4 is on track for mass production in the second half of the year, in line with customers’ project timelines. We are also preparing for mass production of custom HBM products based on HBM4 and HBM4E, collaborating with multiple customers”.

He added, “As sales of this HBM4 product lineup are expected to ramp up in 2026, volatility in memory earnings will be very high going forward.”

Furthermore, Kim Jae-joon stated, “Despite concerns over global trade disputes and economic slowdown, demand for memory in the mobile and PC markets is expected to improve due to the spread of AI servers and on-device AI. We will actively respond to demand for HBM and other high-capacity products, and focus on enhancing competitiveness around high-value-added products”.

Kim JaeHun (rlqm93@fntimes.com)

![[DQN] 커지는 하이닉스 의존도…SK스퀘어의 딜레마](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709203239068320141825007d12411124362.jpg&nmt=18)

![[자사주 리포트] 태광산업 vs 트러스톤](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607100742140295807de3572ddd12517950139.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)