According to the financial investment industry on the 19th, LG Electronics shares closed down 9.77% from the previous session at KRW 217,000. The stock had previously surged as high as KRW 266,500 intraday on the 15th, surpassing its previous all-time high of KRW 193,000 recorded in 2021, but reversed course on the 18th as profit-taking orders poured in. Nevertheless, the share price continues to hold above the KRW 200,000 level, maintaining elevated ground.

Last year, LG Electronics shares closed at KRW 92,000. The stock had begun rising in earnest from the start of this year, but had gone relatively unnoticed as market attention was focused on artificial intelligence (AI) and the semiconductor sector.

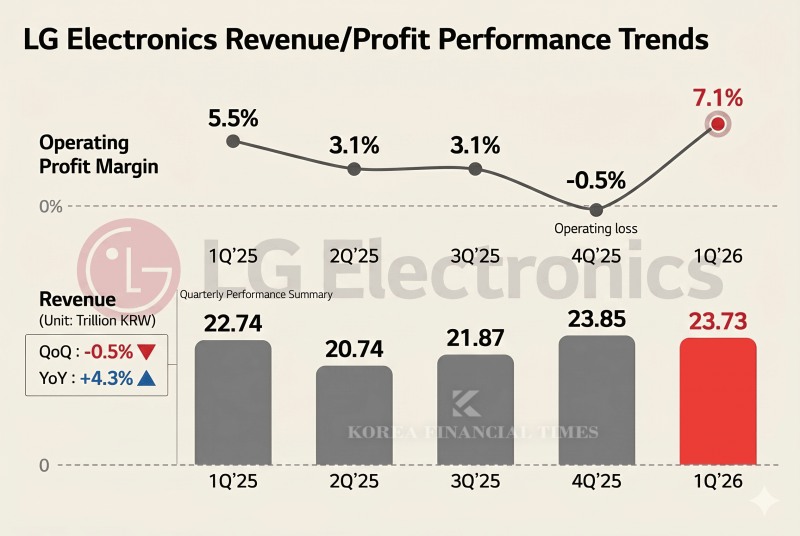

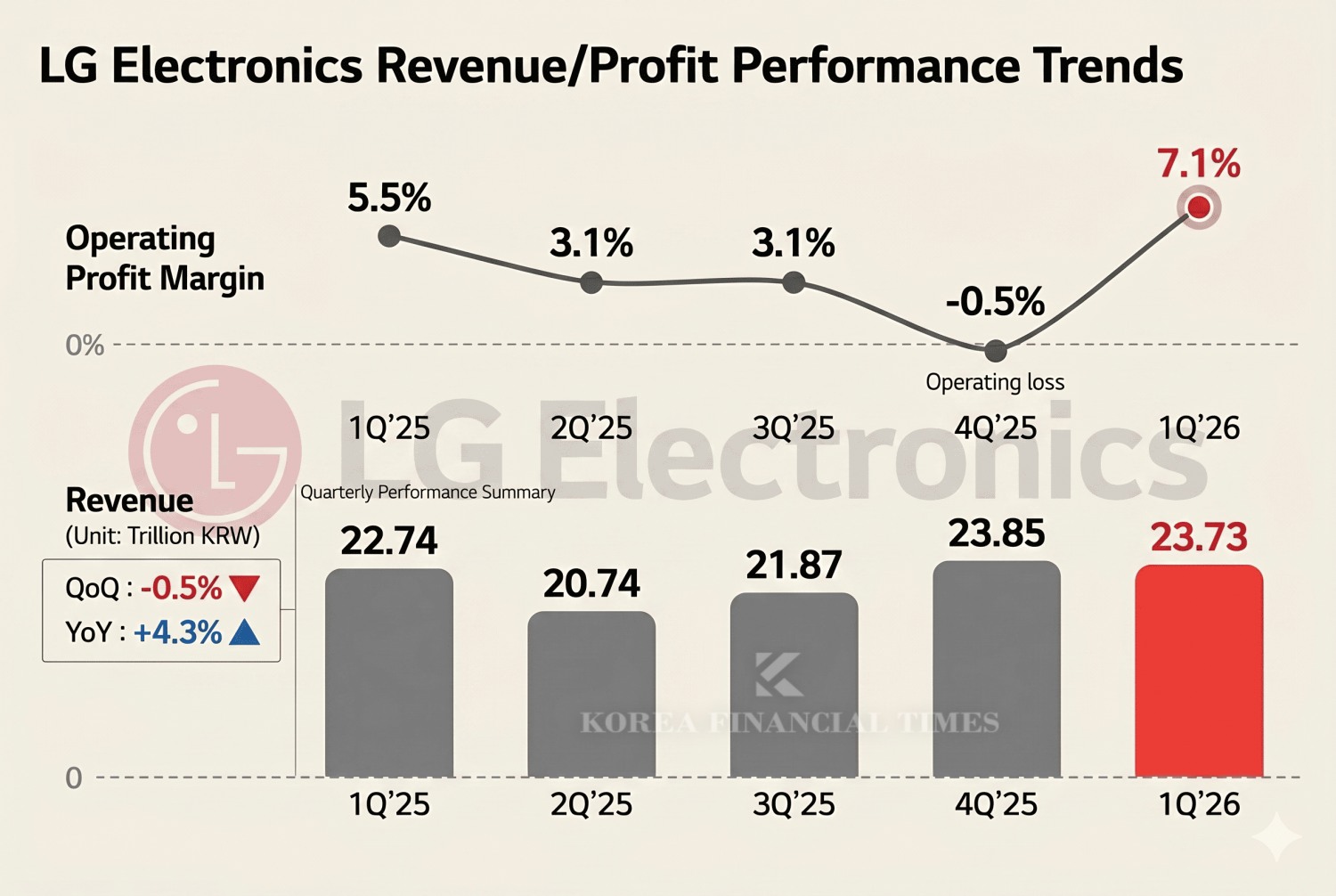

In Q1 of this year, LG Electronics posted a significant earnings surprise. In stark contrast to the sluggish performance of 2025 — when annual operating profit fell 27.5% year-on-year — the company reported record-breaking Q1 2026 results of KRW 23.7 trillion in revenue and KRW 1.6737 trillion in operating profit.

The growing visibility of the company's robotics business, widely regarded as a promising future industry, also acted as one of the factors driving up its corporate value. Strong earnings combined with optimism about future growth were seen as positive catalysts for investor sentiment.

However, such assessments fail to fully capture the depth of LG Electronics' fundamental transformation. In particular, market "optimism" is heavily influenced by supply-and-demand dynamics, and it can turn toxic for investors if anticipated developments fail to materialize.

Cross-divisional Linkages and the Evolution of a 'Sales + Services' Platform

The primary contributors to LG Electronics' improved earnings are its Home Appliance & Air Solution (HS) and Vehicle component Solutions (VS) business divisions. The HS division benefited from peak-season tailwinds and successfully executed a two-track strategy simultaneously targeting both premium and entry-level product segments.

Koo Kwang-mo's Vision for AI and Robotics Drives LG Group's Transformation [KFT Topic]LG Electronics' Two Robot Companies Show Polar Opposite Results...Robostar vs ROBOTIS '10-Fold Return Gap'LG Corp. Taps Asset Sale Proceeds to Defend Dividend Amid Subsidiary SlumpLG Energy Solution vs. Samsung SDI: The Robot Battery Market BattleLG Electronics challenges to become India's 'national appliance brand', targeting growing middle class

The VS division likewise recorded all-time highs in both revenue and operating profit. The results reflect tangible payoffs from product mix improvements centered on high-value-added products and structural cost innovation, underpinned by a stable vehicle component order backlog.

The Media Entertainment Solutions (MS) division, despite a seasonal off-peak period, also achieved a year-on-year turnaround to profitability, driven by solid premium TV sales and expanding revenue from the webOS platform.

Viewing each division in relation to one another, LG Electronics' strategic direction becomes unmistakably clear. The core focus is on "servicification" — generating continuous revenue that extends well beyond the point of sale, rather than ending the customer relationship at a product transaction.

At the center of this effort is the webOS platform. According to LG Electronics, webOS is installed on more than 200 million LG Smart TVs worldwide. This has become a powerful vehicle for generating service revenue through content and advertising. The company is steadily raising the share of non-hardware revenue, effectively shedding its identity as a conventional manufacturer.

By extending the successful home appliance subscription model beyond Asia into the Middle East, the company has achieved two objectives simultaneously: structural transformation and continued growth.

Another notable shift is the expansion of B2B (business-to-business) operations. The vehicle components and commercial energy solutions divisions together account for 36% of total revenue, while the home appliance segment remains primarily B2C (business-to-consumer) oriented. A business model skewed too heavily toward either B2B or B2C tends to be less resilient in the face of external disruptions. By expanding its B2B operations, LG Electronics has secured greater earnings stability.

Smart Life Solutions — the Leading Driver of FCF Improvement

LG Electronics' strong Q1 performance this year did not emerge overnight. The company has long recognized that customers seek increasingly sophisticated experiences through their products. Rather than ending its relationship with customers at the point of purchase, LG Electronics has continually deliberated on how to deliver ongoing care and create new value throughout the entire product lifecycle.

This reflects sustained, long-term effort to transcend the inherent limitations of a traditional manufacturing model. In plain terms, the objective has been to supplement a hardware-centric sales model that is highly sensitive to economic cycles.

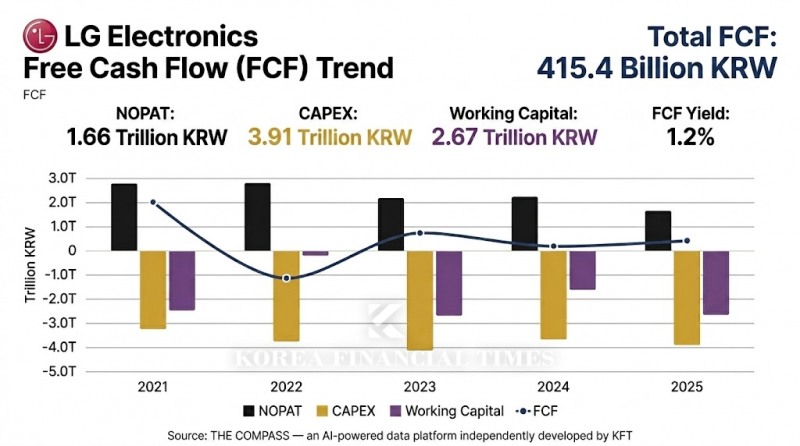

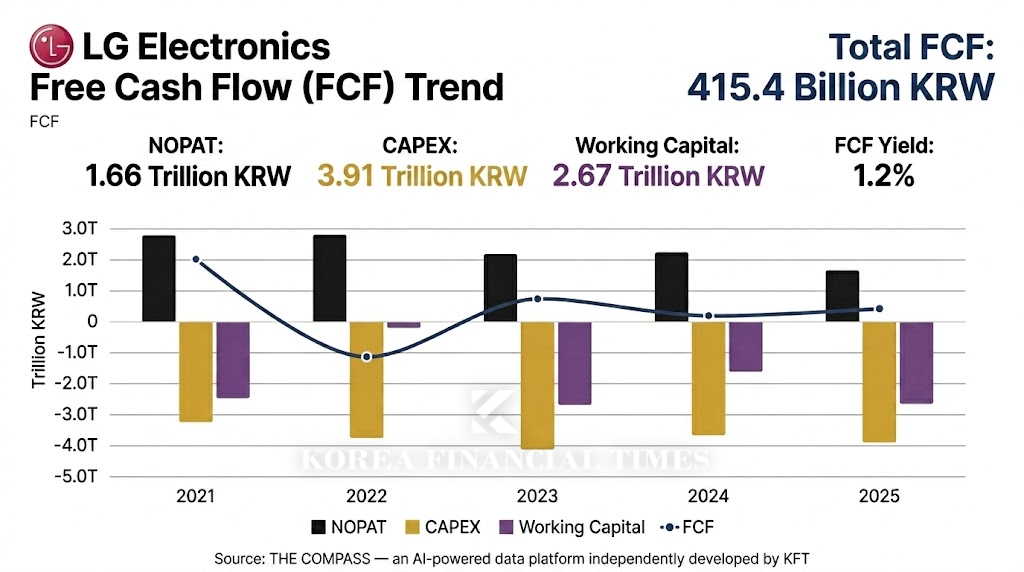

Manufacturing entails large-scale capital expenditures (CAPEX), which exerts a negative impact on cash flow and makes it more difficult to enhance corporate value.

This infographic, originally published by Korea Financial Times, has been reconstructed using generative AI (Gemini).

이미지 확대보기

However, LG Electronics has not actually cut CAPEX. According to The COMPASS — an AI-powered data platform independently developed by Korea Financial Times — LG Electronics' CAPEX rose from KRW 3.6680 trillion in 2024 (including intangible assets) to KRW 3.9074 trillion in 2025.

Over the same period, free cash flow (FCF, after deducting depreciation and amortization) jumped significantly from KRW 185.9 billion to KRW 415.4 billion. This is particularly noteworthy given that operating profit declined from KRW 3.4197 trillion to KRW 2.4784 trillion during the same period, suggesting that substantial progress has already been made in cash flow management.

Return on Invested Capital (ROIC) — an indicator of the profit generated from operating assets — declined from 6.8% in 2024 to 4.9% in 2025. However, given the improvement in FCF and the continued expansion of the platform-based home appliance subscription service, an upturn in ROIC is anticipated.

While the recent share price surge has significantly elevated the Weighted Average Cost of Capital (WACC), the strong Q1 earnings, together with improvements in business fundamentals and FCF, are expected to meet investor expectations.

An investment banking (IB) industry source noted, "Many critics have pointed out that LG Electronics missed the opportunity to acquire SK Hynix in the past," adding, "Not every company can operate in the AI or semiconductor space; what matters is pursuing stable growth within one's own domain, and this narrow-minded perspective has led to an undervaluation of LG Electronics." The source further commented, "LG Electronics' share price has risen sharply, but it has only just crossed a price-to-book ratio (PBR) of 1x. If the company continues to demonstrate growth through fundamental transformation, its true value will be fully recognized by the market."

Lee Sungkyu (lsk0603@fntimes.com)

![[DQN] 커지는 하이닉스 의존도…SK스퀘어의 딜레마](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709203239068320141825007d12411124362.jpg&nmt=18)

![[자사주 리포트] 태광산업 vs 트러스톤](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607100742140295807de3572ddd12517950139.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)