Anwar A. Al-Hejazi, CEO of S-OIL

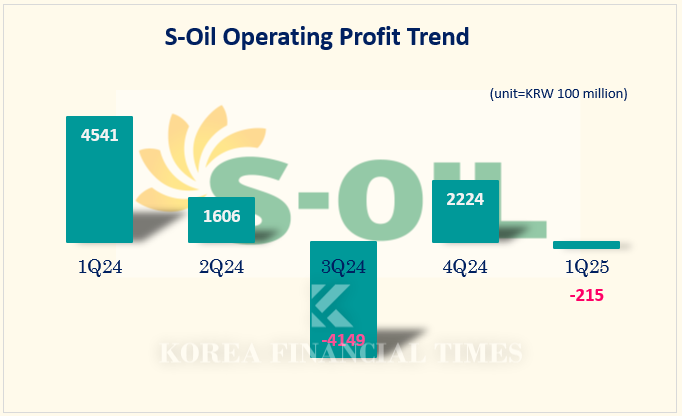

S-OIL announced on the 28th that its Q1 2025 sales were provisionally calculated at KRW 8.9905 trillion, with an operating loss of KRW 21.5 billion. Compared to the same period last year, sales decreased by 3.4%, and operating profit turned to deficit.

S-OIL's operating profit forecast was as high as KRW 280 billion until March. However, expectations for performance rapidly declined this month due to a combination of weak demand from economic slowdown and falling refining margins caused by plummeting international oil prices.

Looking at the actual results, all business divisions performed poorly.

The refining division shifted from an operating profit of KRW 250.4 billion in Q1 last year to an operating loss of KRW 56.8 billion in Q1 this year. The petrochemical division also recorded an operating loss of KRW 74.5 billion during the same period, compared to an operating profit of KRW 48 billion last year.

The lubricant base oil division maintained profitability with an operating profit of KRW 109.7 billion. However, the profit size decreased by about 30% compared to the same period last year. This was due to lubricant base oil margins falling by about 17% to an average of $43 per barrel in the first quarter.

S-OIL explained, "Demand was weak due to concerns about economic slowdown, and profitability declined as scheduled regular maintenance by some regional refineries in Q1 was postponed to Q2."

S-OIL appears to be on high alert regarding the "tariff risk" from the U.S. government.

According to S-OIL, the company has almost no direct impact from U.S. tariff policies. Refining and lubricants, which account for about 90% of sales, are not subject to tariffs. For petrochemicals, most items except MX (mixed xylene) are subject to tariffs. For example, exports of benzene, a U.S. tariff target item, decreased in the first quarter.

However, S-OIL noted, "Even for items subject to tariffs, direct exports to the U.S. accounted for only about 0.1% of sales based on 2024 figures."

Nevertheless, the company did not deny the impact from overall market demand weakness due to tariffs. S-OIL said, "Market participants in olefin and aromatic markets are taking a wait-and-see approach due to U.S. tariff policies," adding, "Major global organizations predict that petroleum demand will decrease by 100,000 to 500,000 barrels per day."

If S-OIL's poor performance continues, financial burden is also expected to be significant. The company has been conducting the "Shaheen Project" since 2023, investing approximately KRW 9.3 trillion to build large-scale petrochemical facilities in Ulsan. The company's net borrowings have soared from KRW 3.862 trillion at the end of 2023 to KRW 6.075 trillion at the end of Q1 2025.

Dividend expectations may also decrease. S-OIL paid KRW 5,500 per share in 2022, but reduced this to KRW 1,700 in 2023 when the Shaheen Project began. In 2024, only KRW 125 was paid due to poor performance.

This year, according to the "Value-up" disclosure announced in January, the company plans to maintain a minimum dividend payout ratio of 20%. Based solely on Q1 performance, which recorded a net loss, the company would not be able to pay dividends.

Gwak Horyung (horr@fntimes.com)

![“희망퇴직 아닌 구조조정”…라이나생명 노조, IT 인력 재편에 반발 집회 [막 오른 금융권 하투(夏鬪)]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260731143300046780ed56b8e1f8203251185109.jpg&nmt=18)

![[그래픽 뉴스] 미국 증시 새로운 키워드 'MANGOS'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202607291740382069de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)