This infographic, originally published by Korea Financial Times, has been reconstructed using generative AI.

이미지 확대보기

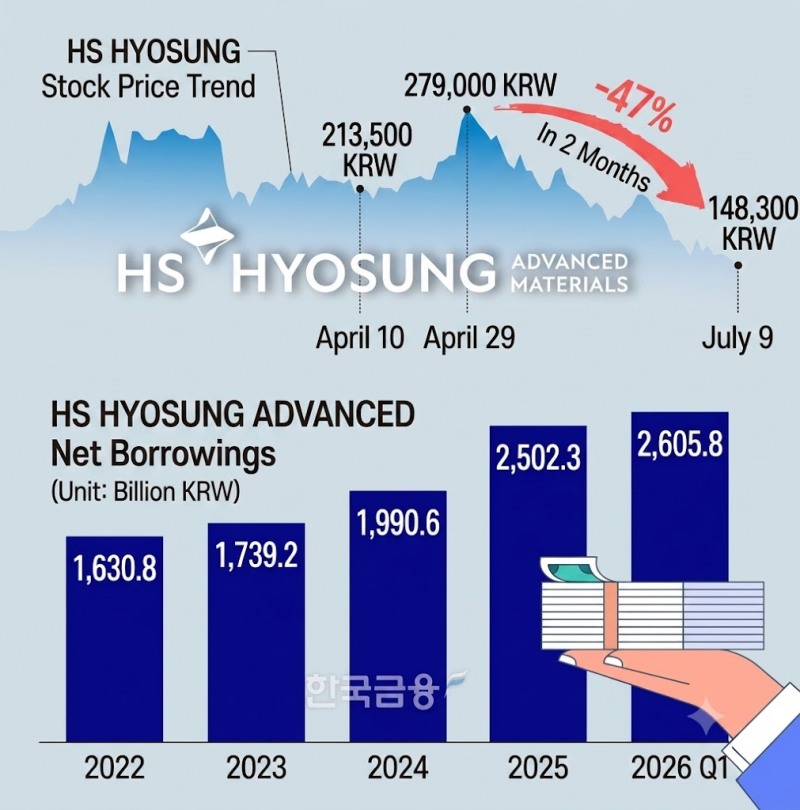

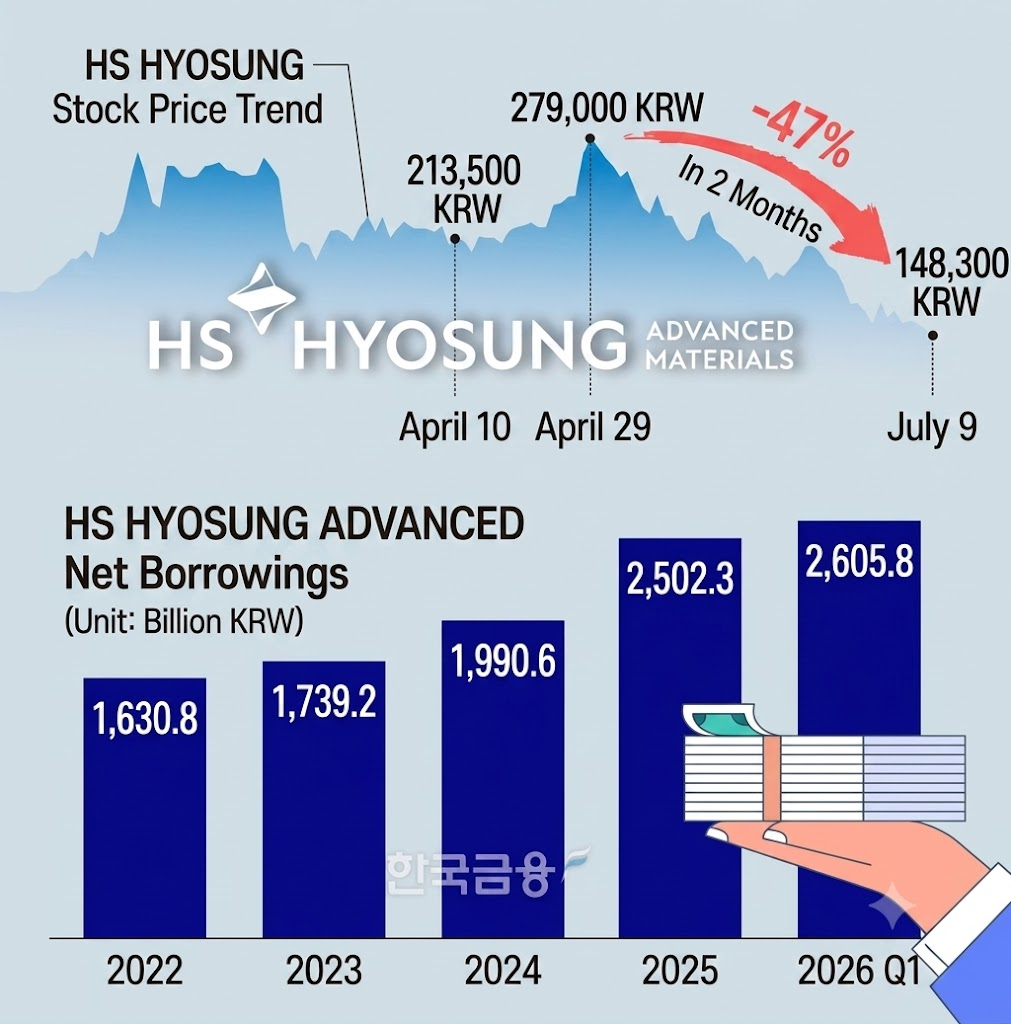

HS Hyosung Advanced Materials shares have fallen 15% since the start of the year.

In particular, the stock plunged 47% in just two months, from its yearly high of KRW 277,500 on April 29 to KRW 148,300 on July 9. Even as expectations grow for an industry rebound this year, why has the stock performed so poorly?

HS Hyosung was established in 2022 as the entity through which Vice Chairman Cho Hyun-sang, younger brother of Hyosung Group Chairman Cho Hyun-joon, built a genuinely independent management structure. HS Hyosung Advanced Materials — which operates industrial materials businesses including tire reinforcement materials, industrial yarn, aramid, and carbon fiber — serves as the pillar subsidiary of HS Hyosung Group. Although the holding company owns only a 30% stake, the unit accounts for 67% of the group's consolidated revenue.

Owner-manager Vice Chairman Cho Hyun-sang abruptly joined HS Hyosung Advanced Materials as an in-house director this past March. At the same time, he stepped down as CEO of the holding company. The move was interpreted as a sign of his determination to personally oversee HS Hyosung Advanced Materials and focus on the business.

Since Cho's arrival, the company's new business strategy has shifted. Previously, the company had acquired EMM, the Belgian silicon anode material subsidiary of Umicore, for KRW 200 billion last November. It also announced a massive investment plan to inject KRW 1.5 trillion over five years to enter the silicon anode material market — a key next-generation battery material.

To raise cash, the company had also been pursuing the sale of its tire steel cord business. However, in April, HS Hyosung Advanced Materials disclosed that it had notified private equity firm Bain Capital — with which it had been negotiating the sale — that it was withdrawing from the deal, adding that it had no plans to pursue further sale procedures.

The company cited a "surge in demand" and the need for a "stable supply chain" as the reasons for withdrawing the sale. It explained that tire customers had requested a stable supply chain following the outbreak of the U.S.-Iran war on February 28. Concerns over raw material price spikes and supply disruptions also pushed up overall product selling prices.

However, from late April — when the Middle East conflict entered a lull — HS Hyosung Advanced Materials shares began a sharp decline. This is attributed to renewed concerns over the financial burden, which had been one of the reasons behind the steel cord sale plan in the first place.

The company's financial burden has grown since 2023, when it began ramping up expansion of its carbon fiber plants. According to THE COMPASS, Korea Financial Times' proprietary AI data platform, HS Hyosung Advanced Materials' net debt has continued to rise, from KRW 1.607 trillion in 2022 to KRW 2.5307 trillion as of the end of the first quarter of 2026.

This has resulted in annual interest expenses of KRW 80–90 billion. Because operating cash flow has fallen short of capital expenditures, free cash flow (FCF) has been negative for four consecutive years since 2023.

Concerns are also mounting that the financial burden could intensify further as large-scale investment proceeds for the company's new secondary battery materials business. In effect, financial fatigue is accumulating from a new large-scale investment even before the carbon fiber investment has fully borne fruit.

The key question is whether the company can demonstrate its ability to handle additional investment. The company's operating profit this year is expected to rise more than 30% year-on-year to around KRW 200 billion — a level sufficient to cover roughly KRW 300 billion in annual investment. However, analysts note that to generate meaningful cash flow and ease the current financial burden, the company would need to post annual operating profit in the mid-KRW 300 billion range or higher for several years to come.

Securities firms project the company's 2027 operating profit at around KRW 250 billion. While profitability is improving, given the downward pressure on margins from Chinese capacity-expansion competition in the advanced materials sector, easing the financial burden in the near term is unlikely to be easy.

Gwak Horyung (horr@fntimes.com)

![기관 '원익IPS'·외인 'ISC'·개인 '펩트론' 1위 [주간 코스닥 순매수- 2026년 7월6일~7월10일]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260710221307044270179ad439071182357427.jpg&nmt=18)

![12개월 최고 연 4.51%…HB저축은행 '스마트·e-회전정기예금'[이주의 저축은행 예금금리-7월 3주]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607120021220071607c96e797801121481643.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)