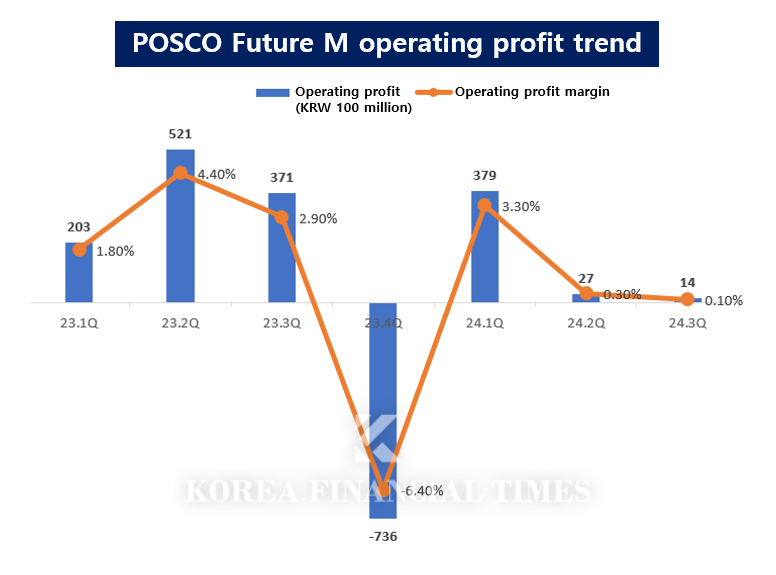

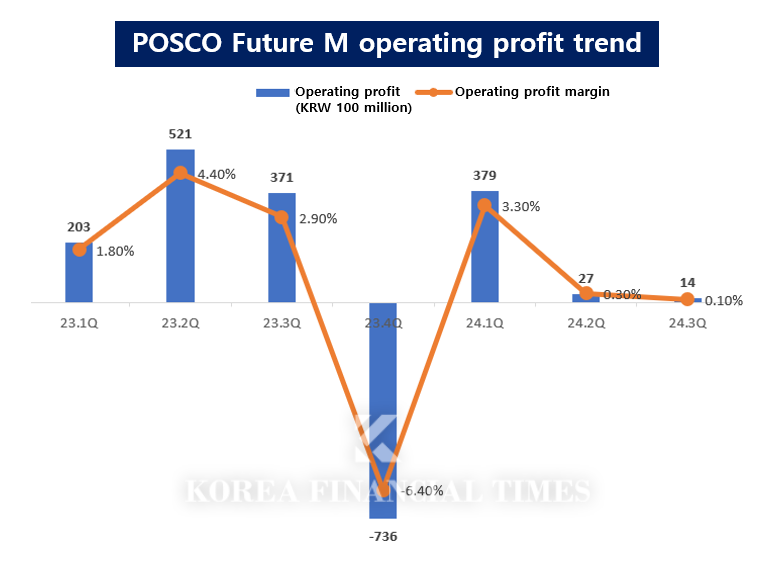

POSCO FutureM is recording operating profit of KRW 42 billion in the first to third quarters of 2024. This is a 61.6% decrease from the first to third quarters of 2023. It is only a quarter of the first to third quarters of 2022 (KRW 162.5 billion), which were on a roll. The profitability of the anode and cathode materials business deteriorated significantly due to the electric vehicle chasm and the plunge in raw materials.

Graph = Korea Financial Times / Source = Financial Supervisory Service Electronic Disclosure

이미지 확대보기

Due to poor performance and deteriorating financial stability, pressure to lower the credit rating (AA-, stable) is also increasing. Korea Ratings presents 'Net debt/EBITDA (operating profit before interest, taxes, depreciation, and amortization) exceeding 4 times' as a factor for reviewing POSCO Future M's credit rating. POSCO Future M had already exceeded the standard at the end of last year. In addition, it has also surpassed 'debt ratio of 150% or more', a factor for downward consideration presented by Korea Ratings.

Expectations for an improved electric vehicle market outlook next year are also low, but POSCO Future M is still supported by the POSCO Group.

Last month, POSCO Future M announced that it will issue a new type of bond-type capital security (perpetual bond) worth KRW 600 billion on the 18th. Of this, KRW 500 billion will be acquired by the holding company POSCO Holdings. Perpetual bonds are recognized as capital in accounting, which has the effect of improving the financial structure. Accordingly, POSCO Future M’s debt ratio is also expected to drop to around 150%. The group's emergency transfusion of funds will put out the fire.

It has decided to adjust its own speed by reducing or postponing planned investments. The company has decided to reduce its target production of negaitive electrode materials, which are currently in deficit, to 113,000 tons in 2026, half the previous level. It has also reduced its target production of positive electrode materials for the same period by about 13% to 395,000 tons.

POSCO-Hyundai Steel, when will the industry rebound? China's stimulus package is the only answer[ECM] SK On ∙ Lotte Chemical, Unstable PRS Contract… Concerns Over Increased Losses'Full of uncertainty' batteries seek turnaround opportunities in EuropeLG Energy Solution 'surpassed expectations', proved competitive, but is there a risk?

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)