According to the Financial Supervisory Service's electronic disclosure system on November 11, Emart's consolidated revenue decreased 1.4% year-over-year to KRW 7.4008 trillion. However, with operating profit increasing, the company continued its earnings improvement trend following its return to profitability in Q2. Cumulative operating profit for the first three quarters reached KRW 332.4 billion, up 167.6% from KRW 124.2 billion in the same period of 2024.

On a separate basis (Emart, Traders, No Brand, Everyday), total sales in Q3 2025 decreased 1.7% year-over-year to KRW 4.5939 trillion, while operating profit fell 7.6% to KRW 113.5 billion. An Emart official said, "Despite temporary factors such as the timing difference of Chuseok, the profitability enhancement measures we have been pursuing continuously contributed to defending our performance."

By business division, discount stores (Emart) recorded total sales of KRW 2.9707 trillion in Q3 2025, down 3.4% year-over-year, with operating profit decreasing 21% to KRW 54.8 billion.

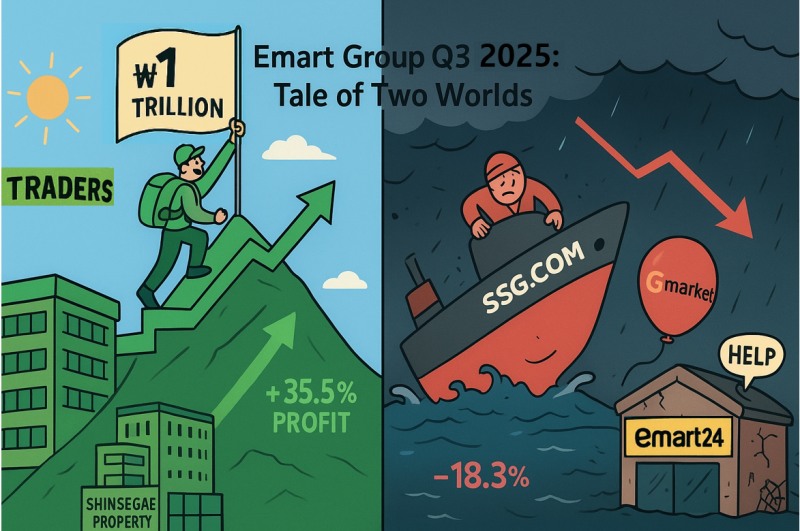

Traders broke through the milestone of KRW 1 trillion in quarterly total sales for the first time. Q3 total sales increased 3.6% year-over-year to KRW 1.0004 trillion, and operating profit rose 11.6% to KRW 39.5 billion. Traders has established itself as a core growth pillar driving Emart's profitability improvement with its steady growth momentum.

Notably, the Magok store (opened in February) and Guwol store (opened in September), both opened this year, achieved profitability from their first month and settled in successfully. This strengthened Traders' competitiveness along with external growth.

An Emart official commented, "The strategy centered on the private brand 'T Standard,' which combines differentiated products focused on bulk buying and value for money with global sourcing capabilities, led to enhanced core competitiveness and became Traders' distinctive strength even amid high inflation." In fact, T Standard's Q3 sales increased 25% compared to the same period last year.

Specialty stores (No Brand) recorded total sales of KRW 254.8 billion, down 2.9% year-over-year, with operating profit decreasing 25% to KRW 8.3 billion. SSM business Everyday's total sales decreased 0.6% year-over-year to KRW 367.8 billion, while operating profit increased 62% to KRW 10.2 billion.

Despite KRW 950 Billion Net Loss, Emart Expands Dividends…PBR at 0.24x ‘Attractive’Chung Yong-jin’s “Determined Resolve” Proven by Results… E-commerce Still Has a Long Way to GoOn the Same Boat with Alibaba? Shinsegae Still Has a Long Way to GoDistribution CEO's Key Message for 2025... Shin Dong-bin's 'Constitution Improvement', Chung Yong-jin's 'Main Business', Chung Ji-seon's 'Cooperation'

Looking at major consolidated subsidiaries' performance, e-commerce divisions SSG.com and Gmarket, and convenience store Emart24 all recorded poor results this quarter.

SSG.com's net sales decreased 18.3% year-over-year to KRW 318.9 billion, with operating losses expanding by KRW 25.7 billion to KRW 42.2 billion. Gmarket also saw net sales decrease 17.1% year-over-year to KRW 187.1 billion, with operating losses expanding by KRW 6.4 billion to KRW 24.4 billion.

Emart24 recorded sales of KRW 552.1 billion, down 2.8% year-over-year, with operating losses expanding by KRW 7.7 billion to KRW 7.8 billion.

In contrast, Shinsegae Property, Shinsegae Food, and Chosun Hotel & Resort posted stable results. Shinsegae Property's net sales increased 46.8% year-over-year to KRW 114.6 billion, with operating profit rising by KRW 34.8 billion to KRW 39.5 billion. An Emart official explained, "We achieved solid results thanks to strong business performance centered on Starfield, which customers consistently visit, and participation in various development projects."

Shinsegae Food's net sales increased 1.4% year-over-year to KRW 390.8 billion, with operating profit rising by KRW 1.5 billion to KRW 10 billion. Chosun Hotel & Resort's revenue increased 12.7% to KRW 210.8 billion, with operating profit rising by KRW 2.6 billion to KRW 22 billion. The company showed stable growth momentum as operating profit expanded through improved occupancy rates and average room rates.

An Emart official stated, "Q3 results demonstrate that our core business competitiveness is strengthening without being shaken by external variables. We will continue our stable growth trajectory based on core business competitiveness while strengthening benefits that customers can feel, centered on the three pillars of price, products, and space."

Park seulgi (seulgi@fntimes.com)

![[DCM] 아시아나항공, 에어부산 살리려 주주가치 희생했나](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260617175630066310141825007d12411124362.jpg&nmt=18)

![엔씨 ‘자사주 활용법’...‘방어’에서 ‘보상’으로 [자사주 리포트]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202606181253540575307492587736124111243152.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)