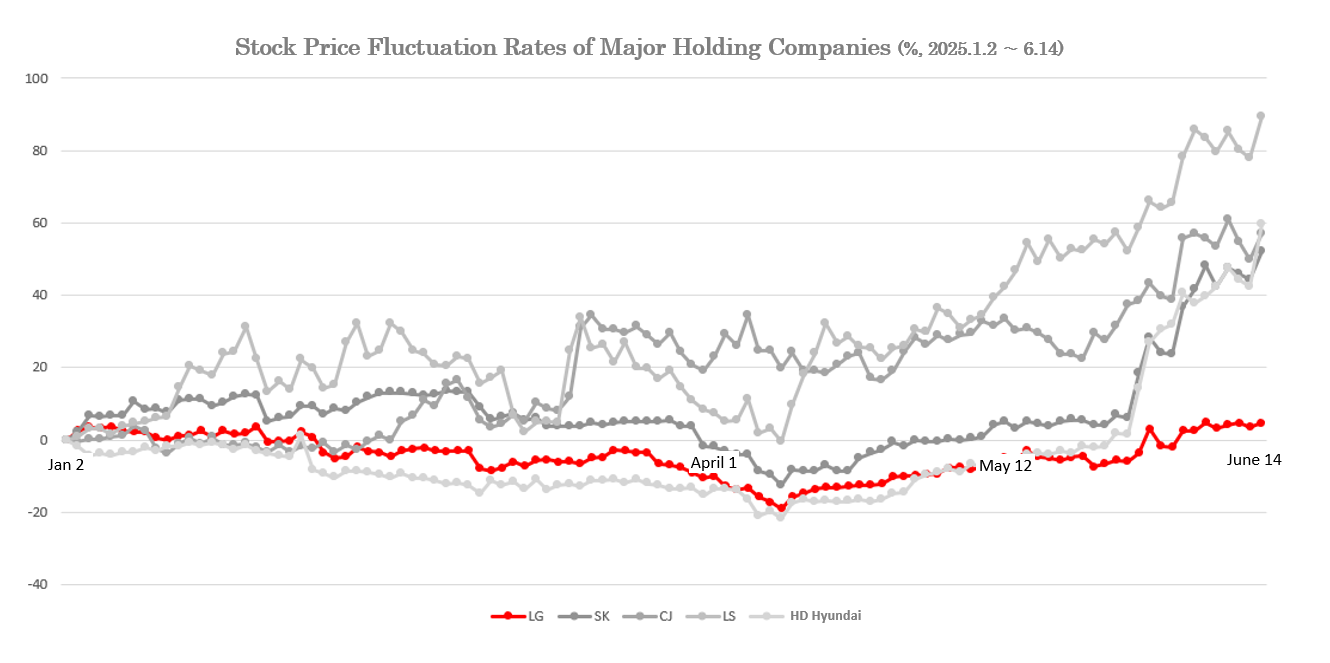

LG Corp. shares rose 4.7% this year, climbing from 72,200 won at the start of the year to 75,600 won as of the closing price on June 16. This pales in comparison to other holding companies that have soared over the same period: LS (89.3%), HD Hyundai (59.6%), CJ (56.9%), and SK (52.3%). Even GS, which spun off from LG and whose affiliates have struggled, climbed 23.7%.

LG is a pure holding company that does not run its own business operations. Last year, most of its separate revenue of 932 billion KRW came from subsidiaries. The breakdown: 432 billion KRW in dividends, 356 billion KRW in trademark royalties, and 143 billion KRW in rental income from investment properties.

Its main subsidiaries (ownership stakes) include LG CNS (49.95%), LG Electronics (31.07%), LG Chem (30.69%), LG Uplus (37.66%), LG Household & Health Care (30.0%), and HS Ad (35.0%). With the electronics and chemical/battery sectors suffering from weak demand and policy uncertainty in the U.S., expectations for an earnings rebound are low.

However, the recent surge in holding company stocks is largely attributed to policy expectations from the new administration, which has pledged to boost shareholder value and the stock market through measures like amending the Commercial Act.

Through its value-up plan announced late last year, LG raised its minimum dividend payout ratio (based on separate net income, excluding non-recurring gains) from at least 50% to at least 60%. It also announced it would cancel all treasury shares (3.85% of shares, worth about 500 billion KRW) by next year. Still, some argue that “shareholder returns remain insufficient” to drive up the stock price, especially as cash inflows from subsidiaries dwindle.

LG CNS was listed on the KOSPI in February this year. Even before the IPO, LG Corp. shareholders were concerned about dilution of shareholder value.

In response, LG CNS CEO Hyun Shin-kyun personally stated, “We will be able to deliver benefits to LG Corp. shareholders by enhancing corporate value.”

On the other hand, Kim Jang-won, a researcher at BNK Investment & Securities, wrote in a pre-IPO report, “When LG CNS was unlisted, there was a direct reason to invest in LG, but after the listing, that role has ended,” adding, “It is hard to expect unlisted companies to serve as substitutes for LG CNS now.”

Meanwhile, Koo Kwang-mo, chairman of LG, recently met with President Lee Jae-myung. The meeting took place on the 13th, when the president invited the heads of the five major conglomerates and the leaders of six economic organizations to discuss economic growth strategies. At the meeting, Samsung Electronics Chairman Lee Jae-yong remarked, “After you were elected president, I read your autobiography.” Attendees, including Chairman Koo, were seen smiling. When it was Koo’s turn to speak, he requested to do so “off the record,” and the president accepted. However, it is reported that sensitive topics for companies, such as amendments to the Commercial Act, were not discussed at the meeting.

Gwak Horyung (horr@fntimes.com)

![[김의석의 단상] 왜 지금 ‘윤종규 리더십’인가](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260807170724038790c1c16452b012411124362.jpg&nmt=18)

![3년 만에 글로벌 1위, 로봇판 화웨이의 탄생 :애지봇(AgiBot·智元机器人)의 시대 [전병서의 中 첨단기업 리포트⑬]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260807173916059060c1c16452b012411124362.jpg&nmt=18)

![12개월 최고 연 6.50%…애큐온저축은행 '처음만난적금'[이주의 저축은행 적금금리-8월 2주]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202608090009240069907c96e797801121481643.jpg&nmt=18)

![장종환 농협캐피탈 대표, 금리 상승·주가 하락 수익성 일시 하락…렌터카 중심 자동차금융 성장세 [2026 금융사 상반기 실적]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260710235019067720dd55077bc212411124362.jpg&nmt=18)

![[그래픽 뉴스] ISA 대개편! 나에게 유리한 계좌는?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202608041713155615de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 미국 증시 새로운 키워드 'MANGOS'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202607291740382069de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)