Chey Tae-won, Chairman of SK

The holding company SK has three main revenue streams. These are: the IT service business (SK AX) absorbed by the holding company and used to strengthen group control, royalties received from affiliates for the use of the ‘SK’ brand, and dividends received from subsidiaries or investment companies.

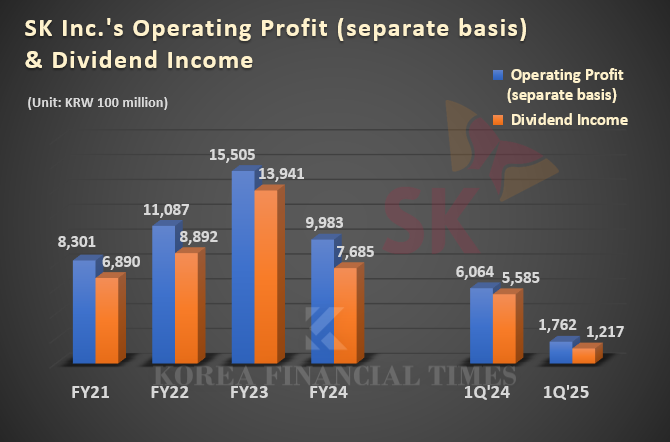

Among these, dividend income is the most significant, accounting for 80–90% of total operating profit. The sharp decline in SK’s earnings in the first quarter was due to a reduction in dividends received. The company’s dividend income was KRW 121.7 billion, a steep 78% drop from KRW 558.5 billion a year earlier.

The company most responsible for this sharp decline in dividends is SK Innovation E&S. Until October last year, SK E&S was a subsidiary in which SK held a 90% stake, serving as a cash generator, but it was merged with SK Innovation.

SK does not disclose the amount of dividends received by each company, but estimates can be made based on the total dividend amount and shareholding ratios. Last year, the company received KRW 768.5 billion in dividends, with about half—KRW 360 billion—coming from SK E&S. Given the absence of E&S dividends this year, it is not surprising that operating profit has plummeted.

However, the dividend effect from E&S has not disappeared entirely, as SK still receives dividends from SK Innovation, which absorbed E&S.

Following the merger, SK’s stake in SK Innovation increased from 36.2% to 55.9%. SK Innovation has resolved to pay a dividend of KRW 2,000 per common share for 2024, with a total dividend payout of KRW 297.6 billion. Accordingly, SK is expected to receive approximately KRW 166 billion in dividends. While this is a significant reduction compared to when it held E&S directly, it is not a complete loss. The dividend was paid in April and will be reflected in second-quarter earnings, not in the first quarter.

SK On Turns to Private Bonds Amid Market Challenges—Can It Stabilize Its Finances?SK Group Doubles Cash Generation on Semiconductor Gains... Energy Sector Increases BorrowingSK Innovation's Credit Rating Downgrade Spiral... Battery Division Faces KRW 1 Trillion Loss Concerns This YearChairman Chey Tae-won of SK Group gives 'high praise at CES'... Who is he praising?

An industry insider commented, “Transferring E&S to SK Innovation shows the holding company’s willingness to accept short-term losses to support SK On. In the long run, it depends on whether Innovation can realize its vision as a comprehensive energy company.”

Gwak Horyung (horr@fntimes.com)

![[DQN] 커지는 하이닉스 의존도…SK스퀘어의 딜레마](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709203239068320141825007d12411124362.jpg&nmt=18)

![[자사주 리포트] 태광산업 vs 트러스톤](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607100742140295807de3572ddd12517950139.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)