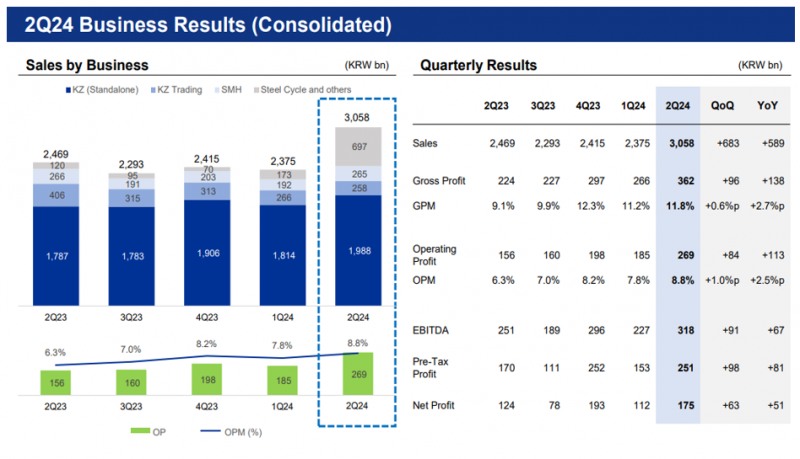

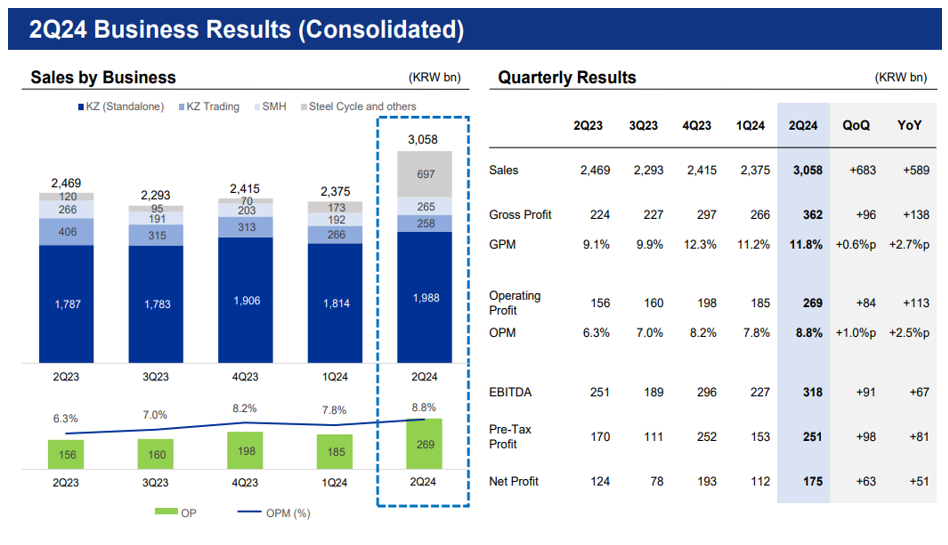

The company's sales and operating profit forecast for the 3rd quarter, as compiled by FnGuide on Sept. 9, is KRW 3.192 trillion and KRW 265 billion. The company is expected to post sales of KRW 3.225 trillion and operating profit of KRW 265 billion in the 4th quarter. The consolidated operating profit forecast for the second half of the year is 17% higher than the first half of the year and 48% higher than the first half of last year.

Korea Zinc is engaged in the business of producing and selling non-ferrous metals such as zinc and lead. The company also recovers and sells gold, silver, and copper from the smelting process, and when the prices of these products increase, the company's performance also increases.

Although the prices of non-ferrous metals have been falling recently due to recessionary concerns, the outlook for the company's performance in the second half of the year is positive as gold and silver prices are expected to strengthen in addition to expectations of interest rate cuts in the US.

“Given the economic slowdown concerns, interest rate cut expectations, and unstable international situation, the company will continue to benefit from stronger precious metal prices in the 2nd half of the year,” said Lee Jae-gwang, a researcher at NH Investment & Securities, in a report on Korea Zinc.

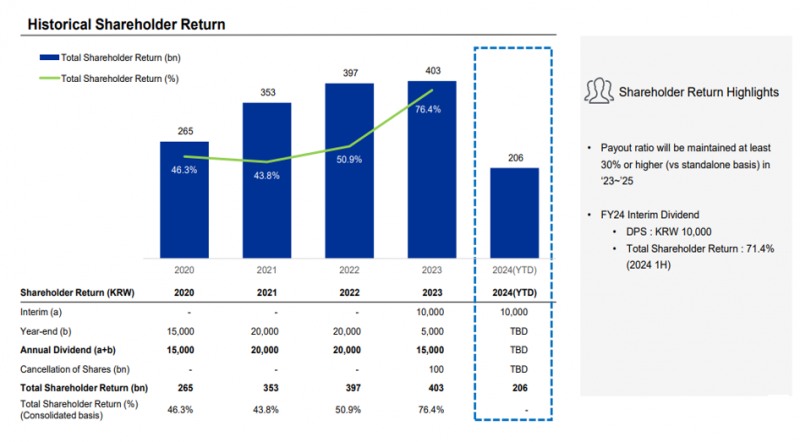

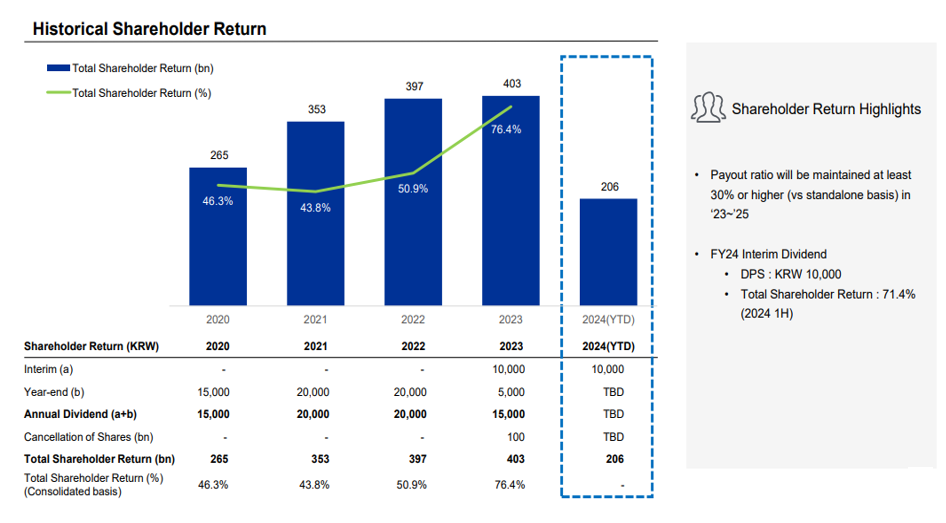

As the company's performance has been on the upswing, it has also been materializing its shareholder return plan.

At the same time, the company said it has approved a plan to buy back 400 billion won of its own shares. The reason for the purchase is to enhance shareholder value, including incineration, and the scale of incineration will be disclosed again when it is implemented until May next year.

The reason why the company favors share buybacks over dividends as a way to return to shareholders is related to the company's shareholding structure.

Korea Zinc is a family of the Youngpung Group, which was co-founded in 1949 by founders Jang Byung-hee and Choi Ki-ho. Recently, Choi Yoon-beom, the 3rd generation of Korea Zinc, has moved to separate the affiliates and is at odds with the Jang family.

The largest shareholder of Korea Zinc is Youngpung, which holds 25.4%. Including this, the Jang family owns 32% of the company. The larger the dividend, the greater the benefit to the Jang family.

While the personal shareholding of the current executive chairman, Choi Yoon-beom, is low at 1.84%, the favorable shareholding of related parties is estimated to be over 33%. In particular, Choi's camp has used domestic companies such as LG, Hanwha, and Hyundai Motor Group as allies to raise their shareholdings. In the process, he also utilized treasury shares purchased in the past.

Choi Yoon-beom, Chairman of Korea Zinc, and Jang Hyung-jin, Advisor to Youngpung (from left)

The conflict between the two families is ongoing. In April, Korea Zinc decided not to renew its 20-year contract with Youngpung to handle sulfuric acid, and in June, Youngpung responded with a lawsuit.

If Korea Zinc continues to perform above expectations under Choi Yoon-beom, the remaining shareholders are likely to support the current management. In fact, the National Pension Service, the second largest shareholder with a 7.8% stake in Korea Zinc, also voted for the agenda posted by the management at this year's general shareholders' meeting where the two families competed.

Gwak Horyung (horr@fntimes.com)

![신한금융, 롯데손보 인수 검토…손보 포트폴리오 강화 승부수 [보험사 M&A 지형도]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607211559530341409efc5ce4ae11823510136.jpg&nmt=18)

!['텐센트 주의보' 시프트업, 경영권 방어와 주주환원 사이 [자사주 리포트]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607211519290590007492587736124111243152.jpg&nmt=18)

![[DCM] SK에코플랜트, 공모사채 1000억 발행…단기물 승부수](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260720232329053880141825007d122461258.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)