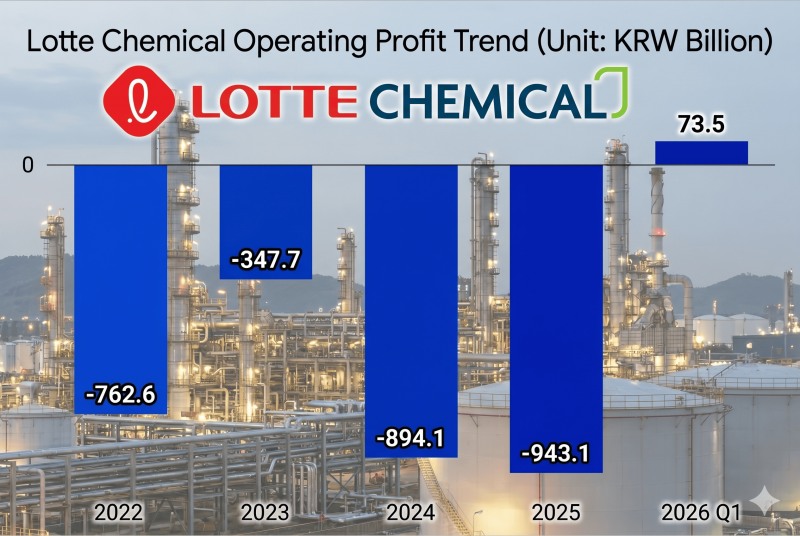

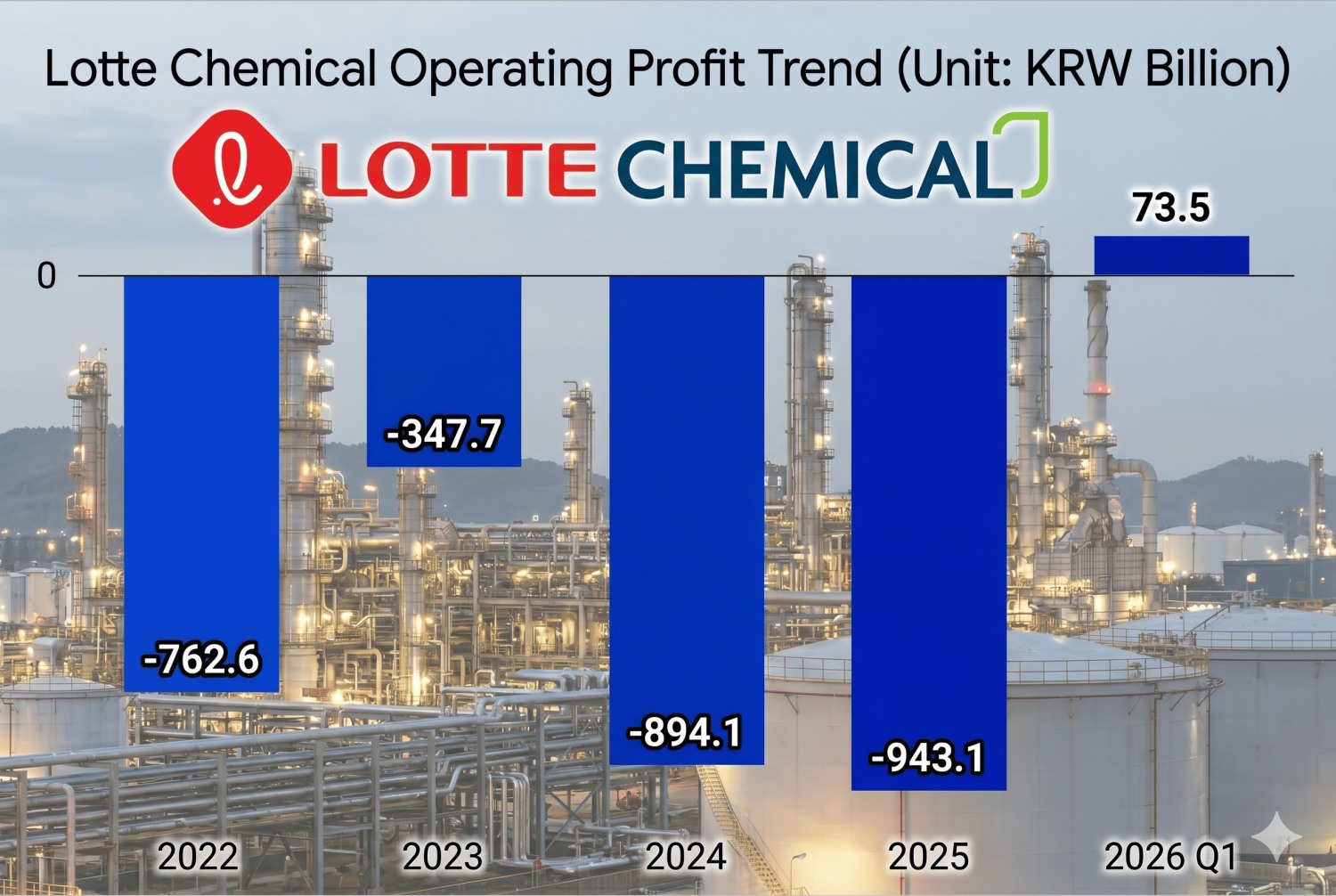

The company posted an operating profit of KRW 73.5 billion in the first quarter, marking its first quarterly profit in 10 quarters—since the third quarter of 2023. The unexpected result was driven by a lagging effect, in which the U.S.-Iran war pushed up international oil and product prices.

From the second quarter onward, there are concerns that earnings could shrink due to a reverse-lagging effect, as the company will have to sell products made from expensive raw materials (naphtha) at lower prices. Still, Lotte Chemical is expected to stay in the black on a full-year basis, as international oil prices are unlikely to suddenly fall below their pre-war levels. At its first-quarter earnings briefing, the company likewise stated that "if raw material and product prices follow a gradual trend through the end of the year, the (negative lagging) impact could be limited."

Expectations of the Strait of Hormuz reopening have also reduced fears that the worst-case scenario—disruptions to naphtha procurement—might materialize.

However, the structural factors weighing on profitability have not been resolved. The domestic petrochemical industry is now in its fifth year of a downturn driven by oversupply originating from China.

On top of this, the financial burden that has long dragged on Lotte Chemical remains. It stems from the company's investment in the "Line Project," a large-scale petrochemical complex in Indonesia, which began at a time that coincided with the industry slump. With the related investment wrapped up at the end of last year, the company's first-quarter capital expenditure (CAPEX) fell to KRW 165.1 billion, less than half the previous quarter's level. However, as temporary funding needs arose to improve its financial structure, the company's negative free cash flow (FCF) widened roughly twofold to KRW 789.8 billion.

Lotte Chemical's financial burden is expected to persist for the time being.

On the 12th, Korea Investors Service lowered the outlook on Lotte Chemical's unsecured corporate bond credit rating from "AA- (stable)" to "AA- (negative)." It noted that, despite the first-quarter earnings rebound, the actual reduction in financial burden is limited owing to a delayed mid-to-long-term industry recovery, an annual interest burden of around KRW 400 billion, and KRW 600 billion in capital contributions to the integrated Daesan entity.

Lotte Chemical Snaps 10-Quarter Deficit Streak... How Long Will War-Driven Windfall Last?Lotte Chemical's Losses Mount for 4th Year as Basic Chemical Unit Struggles, Plans Growth Push in Advanced Materials[Petrochemicals: A Shifting Landscape] Korea's Petrochemical Restructuring Accelerates as Middle East Crisis BitesLotte-HD Hyundai Daesan Merger Signals Full-Scale Petrochemical Restructuring in Korea

Lotte Chemical has faced downgrades to its credit rating or rating outlook almost every year since 2022. Since 2024, the company has been raising liquidity through price return swaps (PRS)—which carry a lighter initial burden as they are not recorded as financial debt—while steadily proceeding with the sale of "non-core" assets.

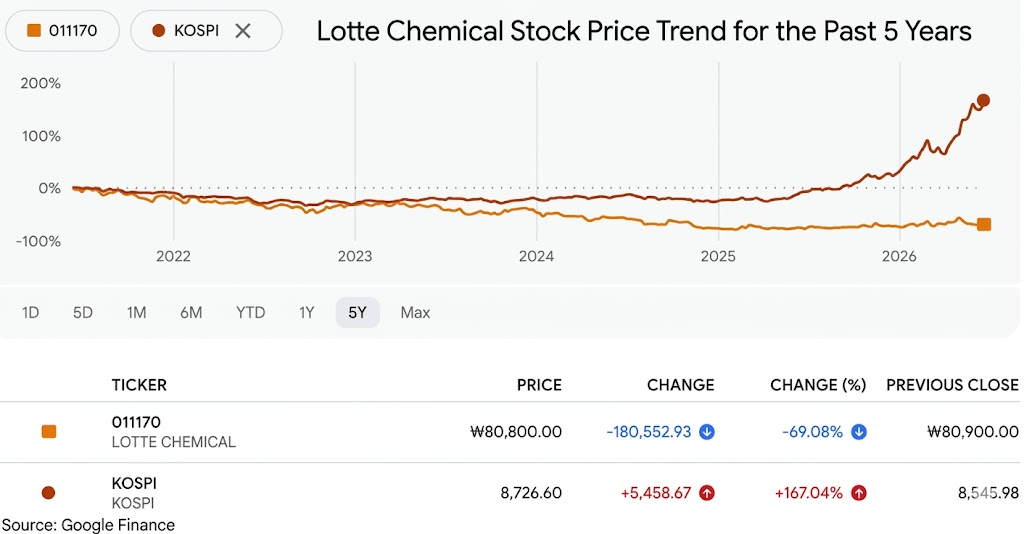

The market, too, maintains a conservative view of Lotte Chemical.

The company's stock has risen 19% this year, underperforming the KOSPI index's 102% gain. Even that increase was concentrated in a roughly 10% surge that began on the 11th, when expectations grew that the Middle East war would come to an end.

According to "THE COMPASS," the proprietary AI data platform developed by the Korea Financial Times, Lotte Chemical's price-to-book ratio (PBR) stood at 0.19 as of the first quarter. This reflects an extreme undervaluation in which the market recognizes only 19% of the asset value recorded on the company's books—effectively a forecast that the current earnings recovery will not be sustained.

A re-rating of Lotte Chemical's corporate value is expected to occur once the effects of its business restructuring become visible. The new businesses being pursued by President Lee Young-jun have stalled, pushed down the priority list for now by the broader restructuring of Korea's petrochemical sector. In his New Year's address this year, Lee emphasized that the company "aims for a fundamental transformation in which functional compounds, semiconductor process materials, green materials, functional copper foil, and eco-friendly energy materials such as hydrogen and ammonia account for more than 60% of its portfolio."

Gwak Horyung (horr@fntimes.com)

![[DCM] 아시아나항공, 에어부산 살리려 주주가치 희생했나](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260617175630066310141825007d12411124362.jpg&nmt=18)

![엔씨 ‘자사주 활용법’...‘방어’에서 ‘보상’으로 [자사주 리포트]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202606181253540575307492587736124111243152.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)