Lotte Chemical Bets Everything on Financial Recovery

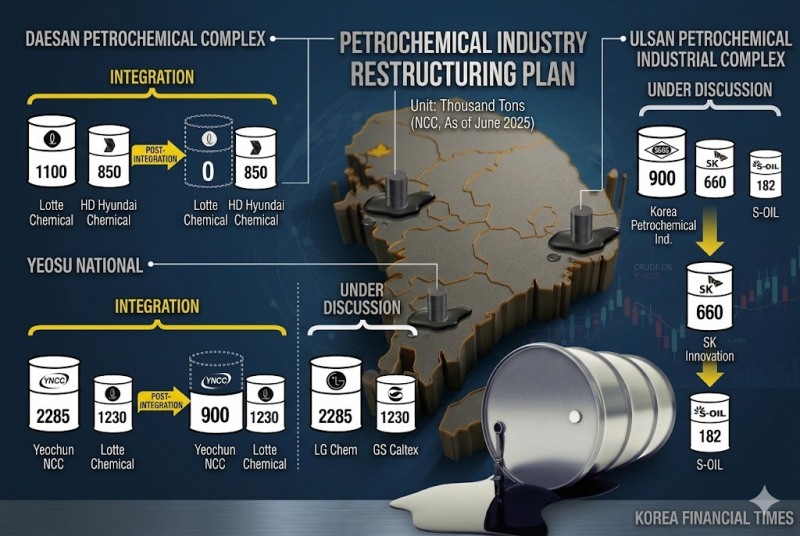

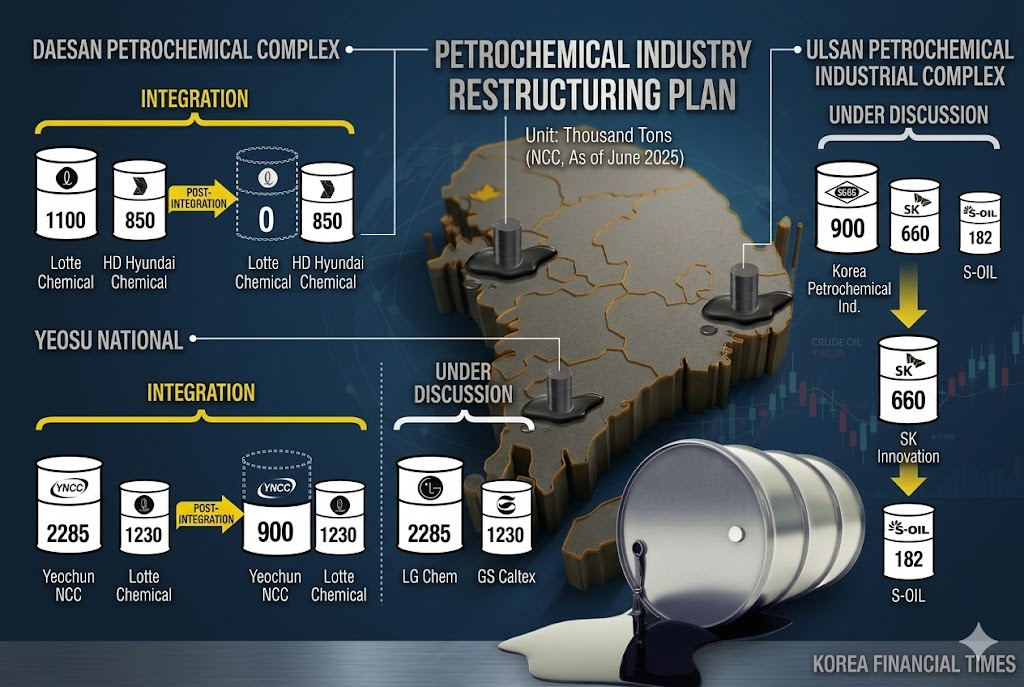

The most proactive actor in the petrochemical restructuring is Lotte Chemical. The company has posted losses for four consecutive years since 2022, largely due to its high exposure to commodity-grade products. Its cumulative deficit has reached a staggering KRW 3 trillion.Lotte Chemical has confirmed a plan to integrate its Daesan plant with HD Hyundai Oilbank. Under the scheme, the Daesan plant — to be spun off from Lotte Chemical — will be merged with HD Hyundai Chemical, a joint venture between Lotte Chemical and HD Hyundai Oilbank, to establish a new entity tentatively named "Lotte Chemical Daesan Petrochemical" in June. Each of the two parent companies will hold a 50% stake in the new entity.

The Lotte Chemical Daesan plant has an annual production capacity of 1.1 million tons of ethylene, while HD Hyundai Chemical has a capacity of approximately 850,000 tons. Following the launch of the new entity, existing Daesan plant facilities will be suspended for at least three years, proactively implementing the government's push to restructure the petrochemical sector.

Lotte Chemical moved quickly in anticipation of a significant improvement in its financial structure. As of end-last year, Lotte Chemical's total debt stood at KRW 6 trillion 965.4 billion, of which KRW 1 trillion 936.3 billion will be transferred to the new entity. Beyond merely reducing figures on the balance sheet, the move also comes with government-level financial support.

Korea Development Bank (KDB) and other creditors have confirmed KRW 2 trillion in financing for the new entity, which also includes a three-year moratorium on repayment of existing corporate bonds.

Lotte Chemical said it expects the Daesan restructuring to reduce its annual losses by hundreds of billions of won. Yuanta Securities forecast that the move could deliver an annual profit improvement of approximately KRW 200 billion.

Yeosu ①: Lotte, Hanwha, and DL Submit Final Plans

The Yeosu Petrochemical Industrial Complex is the central focus of this round of sector restructuring. It is South Korea's largest petrochemical complex, with annual ethylene production capacity exceeding 6 million tons.

Kumho Petrochemical's Treasury Shares Face Governance Test After 20 Years [Treasury Share Report]Lotte-HD Hyundai Daesan Merger Signals Full-Scale Petrochemical Restructuring in KoreaLotte Chemical's Losses Mount for 4th Year as Basic Chemical Unit Struggles, Plans Growth Push in Advanced Materials'Expansion' S-OIL vs. 'Caution' GS Caltex [KFT Topic]

Coordinating competing interests among the NCC (naphtha cracking center) operators in the complex — Yeochun NCC (a joint venture between Hanwha Solutions and DL Chemical) at 2.29 million tons, LG Chem at 2.08 million tons, Lotte Chemical at 1.23 million tons, and GS Caltex at 900,000 tons — is seen as the critical challenge.

Yeochun NCC and Lotte Chemical submitted their final integration plan to the government approximately ten days ahead of the government-set deadline of March 31, on March 20. For the NCC, the plan calls for spinning off Lotte Chemical's Yeosu plant and merging it with Yeochun NCC to establish a new entity.

Downstream operations — products derived from basic petrochemical outputs such as ethylene — will also be integrated into the new entity. These include Hanwha Solutions' polyethylene (PE) and petroleum resin operations in Yeosu, DL Chemical's PE, and Lotte Chemical's basic materials Yeosu business. The companies have further agreed to transition toward higher-value-added products such as medical-grade low-density polyethylene (LDPE) and functional polyolefin elastomers (POE) for automotive wiring, in order to strengthen long-term competitiveness.

Specific reduction targets and the scale of government support are to be finalized after a government review. Within the industry, there is talk of the possible closure of Yeochun NCC's No. 2 plant. Yeochun NCC's No. 3 plant has already been idled. The ethylene production capacities of Yeochun NCC's No. 2 and No. 3 plants are 915,000 tons and 470,000 tons, respectively, for a combined total of 1.385 million tons.

Yeosu ②: LG Chem and GS Caltex Hit by Middle East-Driven Naphtha Crisis

LG Chem and GS Caltex, also operating within the Yeosu complex, are still seeking common ground.Although the submission deadline has passed, both companies appear willing to participate. LG Chem and GS Caltex had submitted a restructuring proposal to the government in December last year, including plans to establish a joint venture for integrated operation of their Yeosu NCC facilities. On March 31, LG Chem President Kim Dong-chun stated the company is "making efforts to move forward with speed."

LG Chem and GS Caltex are said to broadly agree on consolidating and operating their NCC units but remain at odds in the final stages over matters such as equity structure for the proposed joint venture. Whether Chevron — a U.S. energy company that holds a 50% stake in GS Caltex — gives its approval is also considered a critical variable.

Against this backdrop, the military confrontation between the United States and Iran is expected to have a major impact. The view is gaining traction that, with naphtha inventories — the basic petrochemical feedstock derived from crude oil refining — falling sharply, both companies will have no choice but to join the restructuring. Indeed, LG Chem decided on March 23 to temporarily halt operations at its Yeosu NCC No. 2 plant.

LG Chem has also made an emergency procurement of 27,000 tons of Russian-origin naphtha, made possible after the United States temporarily eased sanctions on Russian naphtha tankers waiting at sea. However, further procurement is reported to be difficult.

Going It Alone: The 'Shaheen Variable' at S-OIL

The Ulsan Petrochemical Industrial Complex is regarded as the most challenging site for arriving at a final restructuring plan.Ethylene production capacities in the complex — Korea Petrochemical Ind. at 900,000 tons, SK Geo Centric at 660,000 tons, and S-OIL at 180,000 tons — are the lowest of all major petrochemical complexes. However, the dynamics could change significantly once S-OIL's Shaheen Project, with an ethylene capacity of 1.8 million tons, goes into full operation later this year.

S-OIL has little incentive to reduce its NCC output. The current petrochemical crisis stems from a flood of cheap Chinese supply and declining profitability of products from aging domestic facilities. S-OIL is expressing confidence in its profitability prospects once the Shaheen Project is operational.

The project will incorporate Saudi Aramco's new technology, "TC2C" (Thermal Crude to Chemicals), which directly converts crude oil into petrochemical feedstocks and offers more than three times the feedstock yield of conventional facilities. S-OIL is the company in which Saudi Aramco holds a major stake.

Timing has also worked in S-OIL's favor. Beginning in March, the company has temporarily suspended major facilities for a scheduled maintenance turnaround — planned before the Middle East crisis erupted — which has the effect of minimizing damage from the raw material supply disruption.

However, the financial burden has grown substantially, with KRW 9 trillion 300 billion invested in the Shaheen Project. According to FnGuide, S-OIL's debt-to-equity ratio stood at approximately 198.6% as of end-last year, a rise of roughly 60 percentage points over two years.

Immediate financial risk, however, is not severe, as Aramco's financial support has provided a buffer. Korea Ratings upgraded S-OIL's unsecured bond credit rating from AA (positive outlook) to AA+ (stable outlook) on March 25, also reflecting the resolution of previously identified downside rating factors.

Nonetheless, if the Shaheen Project fails to deliver results as expected, financial risk could resurface.

Korea Ratings stated: "The commercial operating performance of the Shaheen Project, scheduled for completion in the second half of 2026, will be a critical variable for operating results," adding that "depending on supply-demand conditions at the time of actual operation, the return on investment may be delayed beyond initial expectations or earnings volatility may increase."

Gwak Horyung (horr@fntimes.com)

![[DQN] 커지는 하이닉스 의존도…SK스퀘어의 딜레마](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709203239068320141825007d12411124362.jpg&nmt=18)

![[자사주 리포트] 태광산업 vs 트러스톤](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607100742140295807de3572ddd12517950139.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)