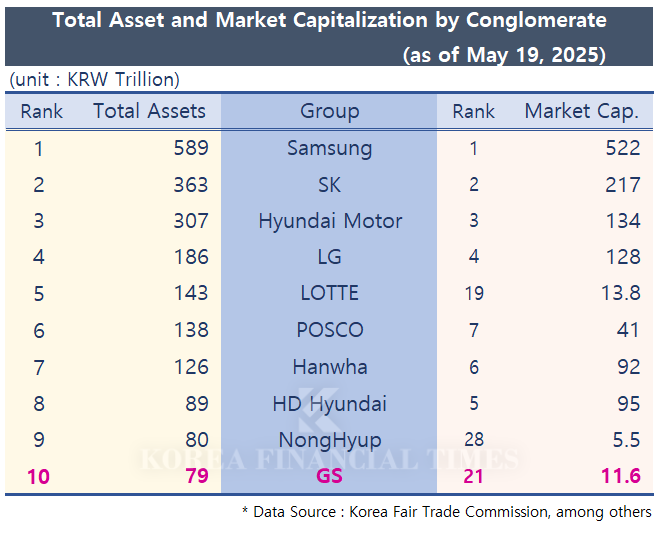

According to the '2025 Designation Status of Publicly Announced Business Groups' released by the Korea Fair Trade Commission (KFTC) on May 1, GS is now ranked 10th among business groups based on total fair assets. This year, GS ceded its 9th place position to NongHyup. In the previous 2024 survey, GS had already lost ground to HD Hyundai, marking a two-year consecutive decline in rankings.

The recent downward trend at GS can be traced to its business structure. GS is built on three main pillars: energy, construction, and distribution-traditional industries with high fixed costs and strong sensitivity to economic cycles. Compared to other conglomerates that have diversified into ICT and bio sectors, GS is seen as lacking in high-profit new business drivers.

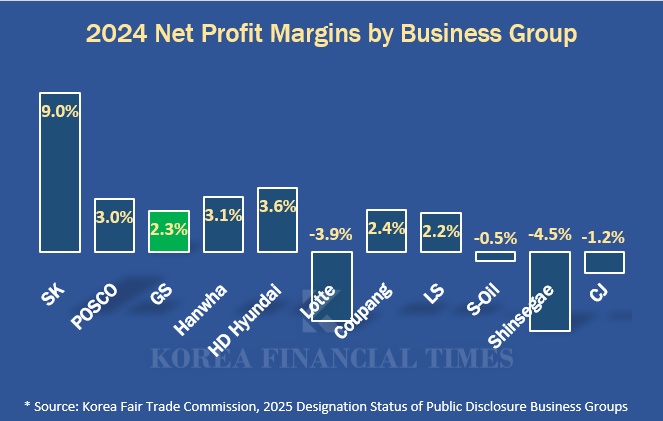

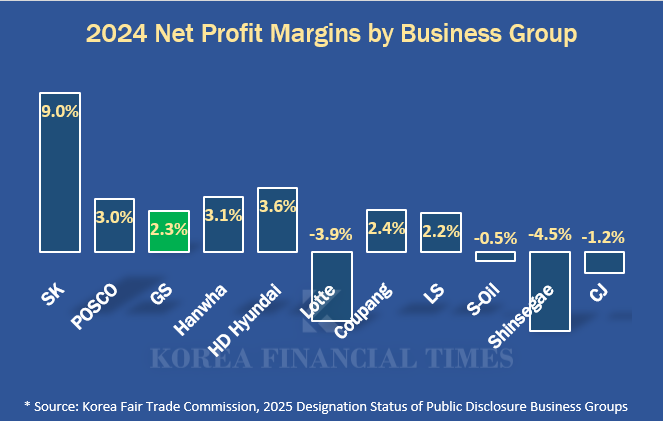

In fact, while GS ranked 6th in sales last year with KRW 81.816 trillion, its net profit was only KRW 1.9 trillion, placing it 12th. The net profit margin was 2.3%. This is lower than Samsung (10.4%), SK (9.0%), Hyundai Motor (8.1%), as well as HD Hyundai (3.6%) and Hanwha (3.1%), both of which have smaller sales volumes.

Nevertheless, some argue that GS performed relatively well given the sluggish business environment. Other energy and distribution groups recorded negative net profit margins: S-OIL at -0.5%, Lotte at -3.9%, and Shinsegae at -4.5%.

In summary, while GS may lack business expansion for future growth, it is interpreted as having stable management capabilities in its main businesses. This characteristic stems from its unique family management system. The holding company GS’s shares are divided among 53 members of the Heo family, the controlling shareholders. One of its key affiliates, GS Engineering & Construction, is directly owned in large part by the family of Chairman Heo Chang-soo, independent of the holding company.

Because the ownership structure is tightly bound by family shares, GS is passive in pursuing initial public offerings (IPOs). Of the 98 affiliates under GS Group, only 8 are listed companies. According to the Korea Exchange, GS Group’s market capitalization is about KRW 11.64 trillion, ranking 21st. Notably, Hugel-a biopharmaceutical company acquired in 2021-has the highest market capitalization at KRW 4.29 trillion. This is higher than not only GS Holdings (KRW 3.61 trillion), but also GS Engineering & Construction (KRW 1.65 trillion) and GS Retail (KRW 1.15 trillion).

An industry insider commented, “Given GS’s business structure, there is little strategic need to attract external capital, and the group likely views such moves as exposing itself to risk.”

Heo Seo-hong, CEO and Executive Vice President of GS Retail

Even so, a wind of change is being detected at GS as it enters a fourth-generation leadership transition. In particular, Heo Seo-hong, who was appointed CEO of GS Retail at the end of last year, has charted a course distinct from other fourth-generation owners. After starting his career as an analyst in the Corporate Finance Division at Samjong KPMG, he worked in the new business team at GS Home Shopping, served as head of management support at GS Energy, and led the Future Business Team at GS. He is known to have spearheaded the acquisition of Hugel during his tenure as head of the Future Business Team. This is considered a very rare M&A case that diverges from GS Group’s typically conservative investment stance.

Gwak Horyung (horr@fntimes.com)

![[DQN] 커지는 하이닉스 의존도…SK스퀘어의 딜레마](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709203239068320141825007d12411124362.jpg&nmt=18)

![[자사주 리포트] 태광산업 vs 트러스톤](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607100742140295807de3572ddd12517950139.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)