Yet the challenges of KRW 12.6 trillion in total debt and the imperative to defend its 'AA-' credit rating remain burning issues for Hanwha Solutions. With the company now required to cover the KRW 600 billion reduction through asset sales, it has entered a critical test of its ability to generate real, tangible cash.

On the 17th, Hanwha Solutions reduced its rights offering from KRW 2.4 trillion to KRW 1.8 trillion, a 25% cut. The funds earmarked for debt repayment were scaled back from KRW 1.5 trillion to KRW 900 billion, while the KRW 900 billion designated for capital expenditures — including investment in Tandem cell technology for future growth — was maintained as originally planned.

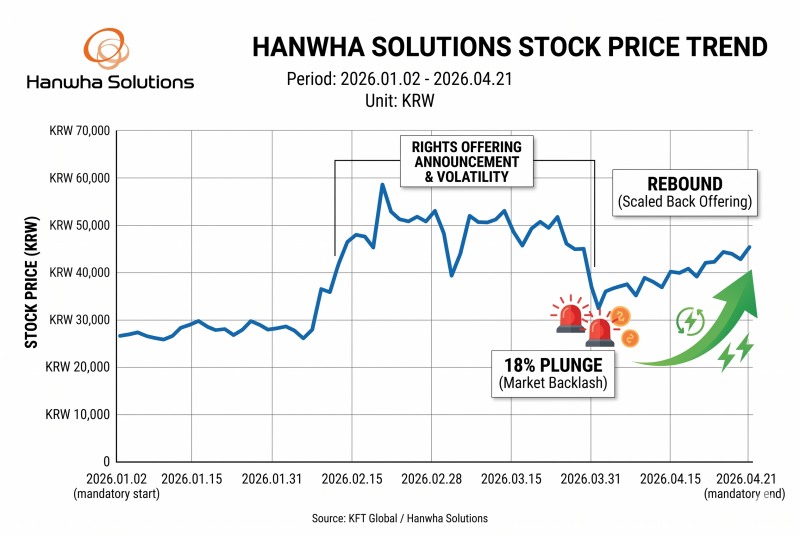

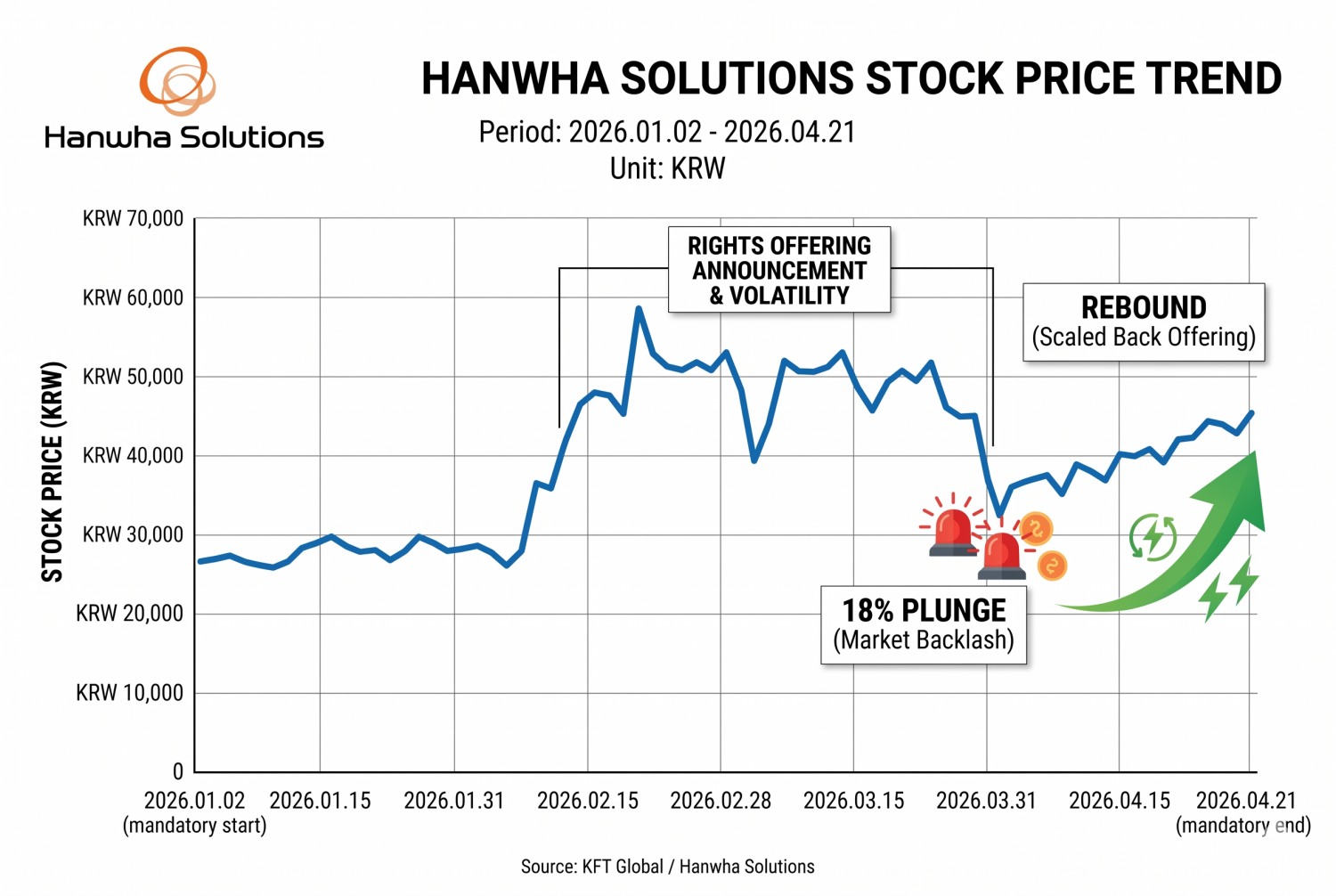

Hanwha Solutions' share price fell 18.22% on the day the rights offering was announced last March 26, dropping to KRW 36,800, and slid further to KRW 35,600 the following day. Since then, the stock has gradually recovered, closing at KRW 45,450 on the 21st — returning to levels seen prior to the capital raise announcement.

Defending the 'AA-' Credit Rating: A Last-Ditch Effort

DATA SOURCE = KOREA EXCHANGE / Recreated with generative AI based on Korea Financial Times content

이미지 확대보기

Hanwha Solutions announced plans to plug the KRW 600 billion gap resulting from the reduced offering through the sale of non-operating assets (KRW 300 billion) and additional capital procurement by overseas subsidiaries (KRW 300 billion), with both measures to be completed within the year.

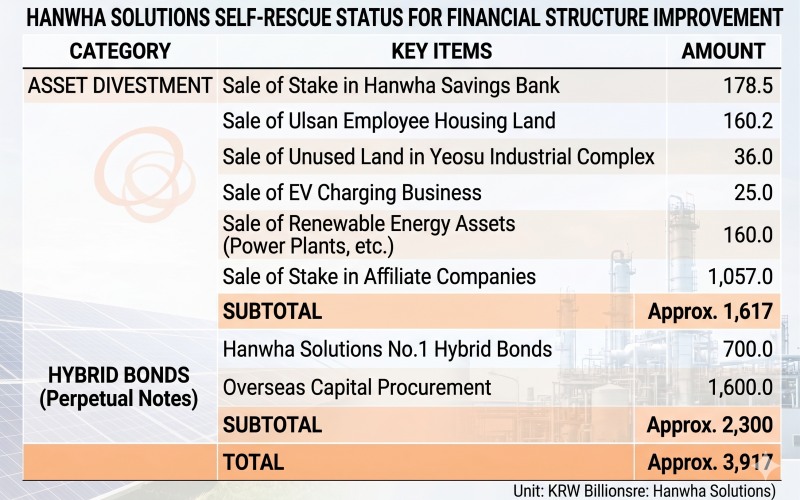

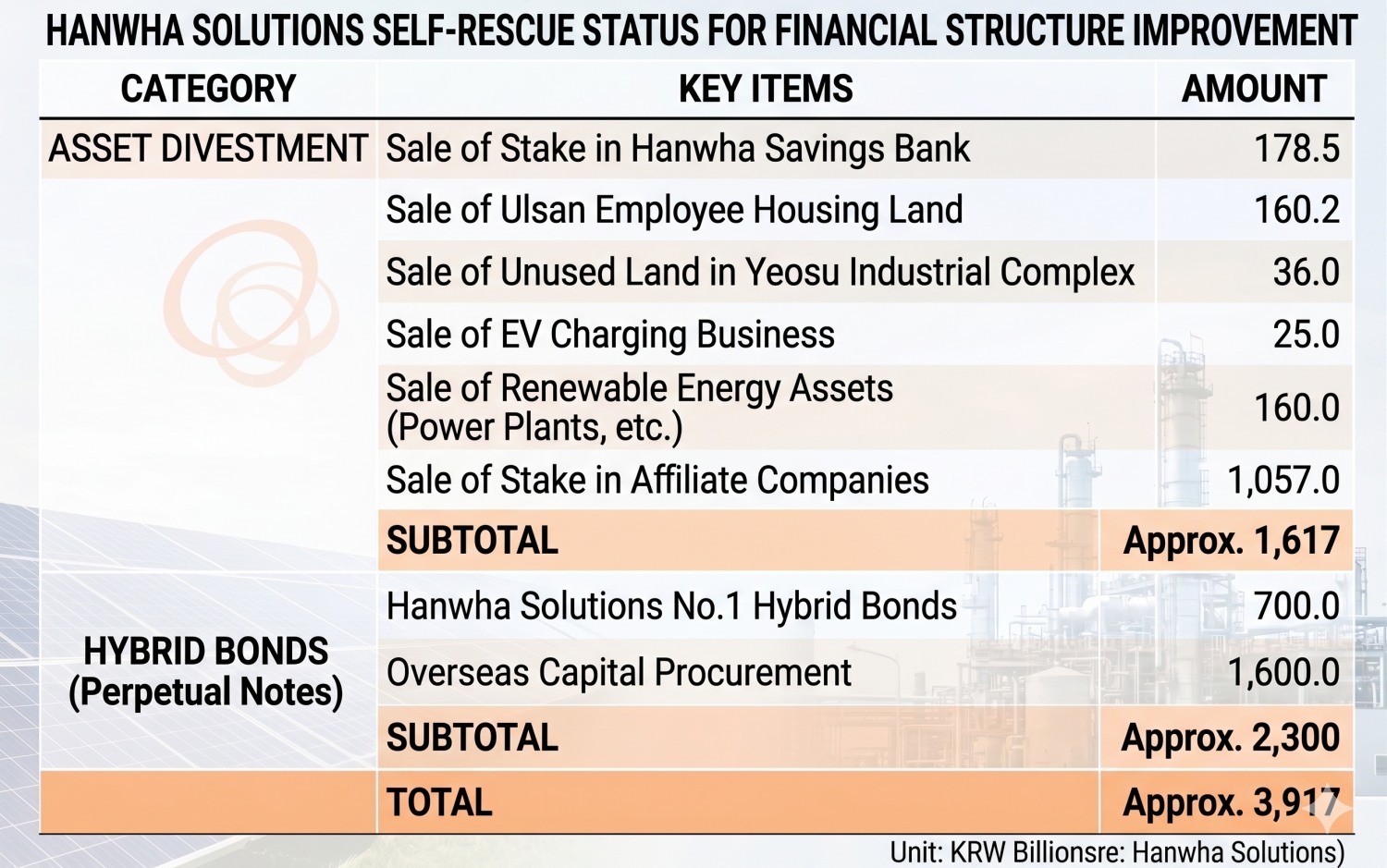

The company has already implemented an aggressive self-rescue plan since 2024, executing measures totaling KRW 3.9 trillion — including approximately KRW 1.6 trillion in asset sales and the issuance of KRW 2.3 trillion in hybrid bonds (perpetual subordinated notes). However, the company stated that with most readily executable options now exhausted and limited capacity for additional large-scale self-rescue measures, the rights offering represents the optimal path to improving its financial structure and securing growth capital.

The reason Hanwha Solutions is staking everything on financial restructuring comes down to its rapidly ballooning debt. Compounded by a prolonged downturn in business conditions, the company's consolidated net debt surged to KRW 12.6 trillion at the end of 2025.

In particular, given that the company has met all criteria for a rating downgrade since 2023 and has faced sustained pressure for a cut, the rights offering is described as a preemptive move to ease the burden of refinancing bonds maturing through the first half of 2028 and to prevent further erosion of corporate value.

Hanwha Solutions presented a financial health roadmap under which the debt-to-equity ratio will be managed below 150% by year-end and below 110% by 2030. Specifically, it plans to reduce net debt from the current KRW 12.6 trillion to KRW 9 trillion in 2026 and KRW 7 trillion by 2030. The company has set targets of KRW 33 trillion in revenue and KRW 2.9 trillion in operating profit by 2030, and plans to use approximately KRW 13.8 trillion in projected EBITDA (earnings before interest, taxes, depreciation and amortization) over the next four years to simultaneously pay down debt and expand shareholder returns.

"Self-Rescue Plan Must Be Executed on Time"

This infographic, originally published by Korea Financial Times, has been reconstructed using generative AI (Gemini).

이미지 확대보기

Market experts have offered a sobering assessment of the tasks ahead for Hanwha Solutions.

Kim Seo-yeon, a senior analyst at NICE Credit Rating, noted that the improvement in financial stability metrics may be limited, since the full KRW 600 billion reduction came entirely from the debt repayment portion. She added that the net debt-to-total-assets ratio under the KRW 1.8 trillion offering scenario would be 29.8% — worse than the previously estimated 27.6%.

Accordingly, she viewed the pace at which Hanwha Solutions monetizes its stake in Hanwha Impact and its holding in Hanwha Hotels & Resorts as the decisive factor for the credit rating outcome.

Jo Hye-bin, a senior analyst at Kyobo Securities, also emphasized the importance of executing the self-rescue plan. She pointed out that while the company intends to sell approximately 10% of its 48% stake in Hanwha Impact within the year, the additional capital procurement of KRW 300 billion from overseas subsidiaries faces challenges — with available capacity standing at only KRW 100 billion as of last month and terms that were unfavorable — making it essential to verify actual execution capability.

She further noted that since this rights offering is a preemptive step ahead of the June regular credit review, the self-rescue plan must be executed on schedule. She also cautioned that with the 2030 targets of KRW 33 trillion in revenue, KRW 12 trillion from Engineering, Procurement and Construction (EPC) operations, and KRW 6.5 trillion from residential energy solutions all requiring simultaneous realization, investors should closely monitor the visibility of the company's earnings structure following the U.S. Investment Tax Credit (ITC) and Advanced Manufacturing Production Credit (AMPC) regimes.

At its rights offering briefing on the 21st, Hanwha Solutions explained the rationale for setting the Hanwha Impact stake sale at KRW 300 billion: "Following discussions with multiple securities firms, we concluded that a sale in the trillion-won range would be difficult given market demand. We determined that approximately 10% of our holdings — equivalent to KRW 300 billion — is a realistic target that can be executed within the year."

On the question of a potential spin-off and sale of the Chemical Division, the company responded: "We are in discussions with a potential counterparty, with the goal of establishing a comprehensive holding entity within the year. Various structures beyond a merger, including share exchanges, remain open options."

Shin Haeju (hjs0509@fntimes.com)

![SK 중간지주사 엇갈린 성적표…‘열등생’ 된 SK디스커버리 [정답은 TSR]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260606000542028020dd55077bc212411124362.jpg&nmt=18)

![‘자사주 소각’ 韓 게임사에 中 텐센트 ‘경보’ [자사주 리포트]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260606014713068990dd55077bc212411124362.jpg&nmt=18)

![‘항공’ 품은 소노트리니티…이젠 ‘숫자’로 증명할 때 [소노트리니티 새 시대 ③]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260605150537047140b5b890e35c220117168247.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)