NHN has expanded into various information technology sectors beyond its core gaming business, moving into music streaming, payment services, and cloud computing. The company’s share price remains in the high KRW 20,000 range, closing at KRW 27,800 on August 12. This marks a steep decline of around 81% from its KRW 149,500 valuation at the time of its 2013 spin-off from Naver.

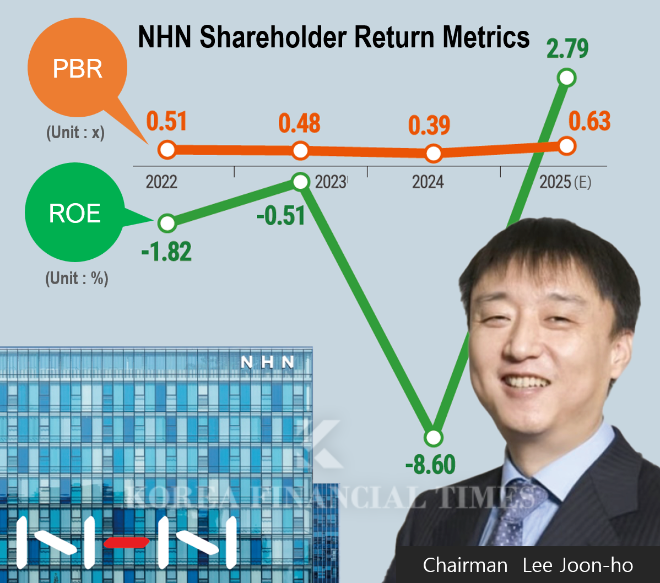

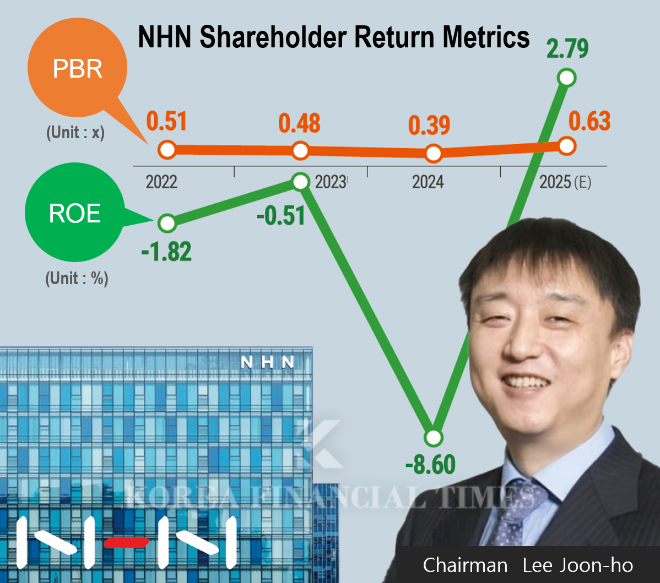

On July 29, the price briefly rose to KRW 36,200, fueled by optimism after NHN Cloud was selected as the primary operator for a government GPU infrastructure project. Despite this, the company’s price-to-book ratio (PBR) stood at just 0.63 x as of Q3 2025—a figure significantly lower than the average 2.10 x for major KOSPI-listed IT firms like Samsung SDS, LG CNS, and Hyundai Autoever.

PBR represents the ratio of a company's market value to its book value. A PBR below 1 suggests that the stock is undervalued relative to its assets, potentially making it attractive to investors.

NHN was created through the spin-off of Naver’s gaming division. Since then, Chairman Lee Joon-ho, who also serves as chairman of the board, has sought to transform NHN into a comprehensive IT firm—reducing its reliance on gaming while pursuing aggressive mergers and acquisitions to diversify.

CEO Chung U-jin, in his twelfth year at the helm, has faithfully carried forward Lee’s ambitions. The number of subsidiaries grew from 39 at his appointment to 89 in 2022. Notable subsidiaries formed during this period include NHN KCP (a digital payments company), NHN Payco, NHN Bugs, and NHN Cloud.

Nevertheless, performance has worsened since 2022. According to the company’s reports, consolidated operating profit came in at KRW 39.1 billion in 2022 and KRW 55.6 billion in 2023, turning to an operating loss of KRW 32.6 billion last year. Net losses amounted to KRW 31.8 billion in 2022, KRW 23.1 billion in 2023, and KRW 192.6 billion in 2024.

In 2022, Chung announced a structural efficiency strategy, aiming to reduce consolidated subsidiaries to around 60 by 2024, focusing on five core businesses: gaming, technology, payments, commerce, and content. As of March this year, NHN had scaled down to 69 subsidiaries.

Instead, it has been reinforcing its core operations by focusing on selected key areas. NHN KCP has maintained a steady cash flow, generating operating profits of KRW 44.2 billion in 2022, KRW 42 billion in 2023, and KRW 43.8 billion in 2024. NHN Cloud, regarded as the company’s future growth engine, has accumulated KRW 91 billion in operating losses over the past three years but has secured growth potential with the government GPU project deal.

During the Q1 2025 earnings call, Chung remarked, “We are accelerating structural improvements by concentrating resources on our core services.”

In 2022, NHN introduced a three-year shareholder return plan allocating 30% of EBITDA to shareholder rewards.

Accordingly, the company retired more than 3.75 million treasury shares — equivalent to 10% of its outstanding stock — between 2022 and last year. However, since NHN began paying regular dividends two years ago, the market has grown increasingly curious about the motives behind the move.

NHN initiated its first dividend of KRW500 per share in 2023, marking the tenth anniversary of its spin-off. The company maintained the same dividend amount last year (2024), despite posting net losses in both years—which resulted in a negative dividend payout ratio.

According to an industry insider, “Even with consecutive losses, NHN’s commitment to dividends over the past two years has been remarkably strong. Chairman Lee Joon-ho is expected to receive billions of won in dividend income annually.”

In reality, Chairman Lee Joon-ho’s direct stake in NHN has grown from 3.74% in 2013 to 28.76% as of 2025. Including JLC (9.92%) and JLC Partners (8.88%), both wholly owned by Lee, along with family affiliates holding 7.05%, Lee and related parties together control 54.61% of the company.

In April 2022, controversy flared over Chairman Lee Joon-ho’s growing influence during the physical spin-off of NHN Cloud. Minority shareholders fiercely objected, arguing that by carving out the company’s prized cloud business in this manner, only Lee’s control was strengthened while the interests of shareholders were disregarded.

The shareholders at the time argued, "If the IPO of the cloud division is pursued, it would intentionally undermine the value of the parent company," further claiming that "this is evidence that share price support is being avoided to facilitate succession."

Lee’s son, born in 1992, joined NHN in 2021 to head a new business task force but left in 2024 to study abroad. NHN has countered claims of succession planning, stating that it had established provisions for allocating shares of any newly-listed subsidiary to parent company shareholders and that no second-generation succession is currently under consideration.

Jeong Chaeyun (chaeyun@fntimes.com)

![[단독] 무신사 스탠다드 ‘산역사’ 이건오 퇴사…‘브랜드 정체성’ 전환점 맞나](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709134450047000b5b890e35c21123419294.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)