Gwak Noh-Jung, CEO of SK hynix

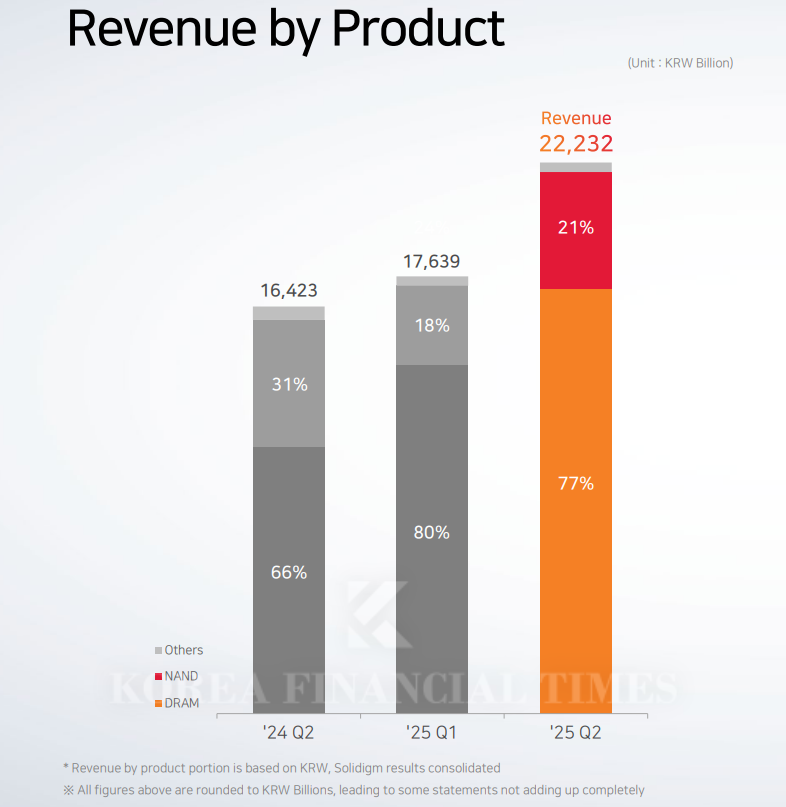

On July 24, SK hynix announced that it achieved revenue of KRW 22.232 trillion, operating profit of KRW 9.2129 trillion, and net income of KRW 6.9962 trillion in the second quarter of 2025. Both revenue and operating profit surpassed the company’s previous records set in the fourth quarter of 2024, and the operating margin reached 41%.

Compared to market expectations, operating profit met the heightened outlook after Micron’s results, while revenue exceeded market estimates by about 7%. SK hynix explained the revenue outperformance as being due to uncertainty over tariffs. Major customers purchasing semiconductors had initially planned to maintain more conservative inventory levels in response to concerns about weakening demand in the second half, but they changed their tactics to maintain adequate inventory in consideration of tariff risks.

SK hynix Rides HBM3E Wave—Is the Era of KRW 10 Trillion Quarterly Operating Profit Here?'DRAM Leader' SK hynix — Can It Make a Mark in 'Non-Memory' Too?SK Group Doubles Cash Generation on Semiconductor Gains... Energy Sector Increases BorrowingSK hynix Posts Over KRW 7 Trillion in Q1 Operating Profit… “Strong Demand for HBM to Persist”SKT Appoints Group's Strategic Expert, Marking Pinnacle in 'AI Company' Transformation

This strong performance was again led by HBM, a memory semiconductor for artificial intelligence (AI). SK hynix stated, “As global big tech firms are actively investing in AI, demand is continuing to grow,” adding that it will maintain its plan to double year-on-year sales in the HBM sector.

SK hynix’s financial soundness has become even more solid as the company continues to post operating margins above 40%. At the end of the second quarter, cash and cash equivalents totaled KRW 16.96 trillion, marking an 75% increase from KRW 9.69 trillion a year earlier. During the same period, the net debt ratio dropped by 20 percentage points to 6%.

Market attention is now focused on next year’s outlook. U.S. investment bank Goldman Sachs downgraded its rating on SK hynix last week from “Buy” to “Neutral,” citing concerns that HBM prices could decline next year.

The next-generation HBM4, which SK hynix is set to launch in full scale in 2025, may face margin pressure. Competitive order bidding with Samsung Electronics and NVIDIA, as well as joint development efforts with TSMC, are expected to weigh on profitability.

At the earnings briefing, an SK hynix official said, “For HBM4, we will adopt a pricing policy that reflects increased costs. We will strive to sustain profitability while promoting further growth in the AI market.”

Gwak Horyung (horr@fntimes.com)

![[DQN] 임종룡號 우리금융, 비은행 순이익 기여도 '꼴찌 탈출' [금융권 2026 1분기 리그테이블]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260430045712008370b4a7c6999c121131189150.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[그래픽 뉴스] “AI가 소프트웨어를 무너뜨린다? 사스포칼립스의 진실”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=2026030416113601805de68fcbb3512411124362.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)

![[AD] 기아 ‘PV5’, 최대 적재중량 1회 충전 693km 주행 기네스 신기록](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20251105115215067287492587736121125197123.jpg&nmt=18)

![[카드뉴스] KT&G, 제조 부문 명장 선발, 기술 리더 중심 본원적 경쟁력 강화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202509241142445913de68fcbb3512411124362_0.png&nmt=18)