This was the reaction from an industry insider to news that SK keyfoundry, SK hynix’s non-memory subsidiary, is aggressively expanding into power semiconductors to escape the loss-making 8-inch foundry market.

Indeed, the company’s performance has deteriorated to the point of turning losses over the past two years. Although it is a fellow semiconductor company, SK keyfoundry finds itself in a world apart from the soaring SK hynix. Still, it’s too early to jump to conclusions. After all, who would have predicted SK hynix would surpass Samsung Electronics in the memory market?

◇ A Return After 18 Years

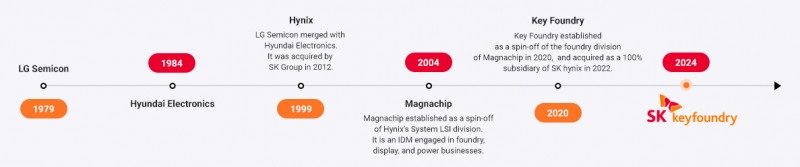

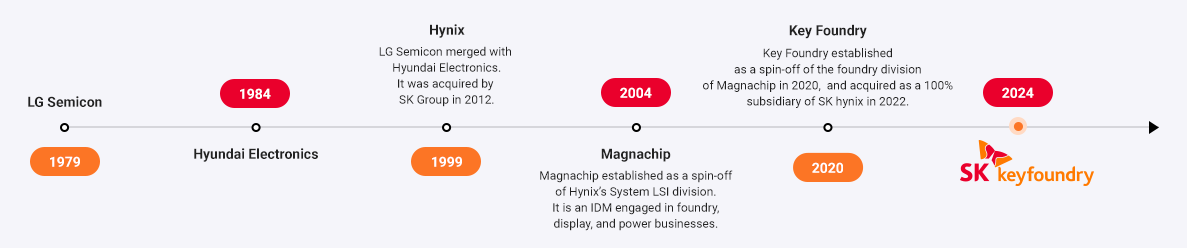

SK keyfoundry is a wholly owned subsidiary of SK hynix. Its roots go back to LG Semicon, founded in 1979. In 1999, during the Asian financial crisis, LG Semicon was merged with Hyundai Electronics in a government-led “Big Deal.” The enlarged semiconductor company sought survival in the market but failed to overcome excessive debt and a liquidity crisis following the “princes’ feud” within Hyundai Group.After leaving Hyundai and rebranding as Hynix, the company sold its non-memory division to a private equity fund in 2004, which became MagnaChip Semiconductor.

In 2022, SK hynix acquired MagnaChip’s foundry business, now known as SK keyfoundry. Eighteen years later, the business has returned to the SK hynix fold.

SK hynix already operates a foundry division, SK hynix System IC, which was spun off in 2017. This unit contract-manufactures general-purpose semiconductors based on 8-inch wafers—such as camera sensors (CIS), display driver ICs (DDI), and power management ICs (PMIC)—for smartphones, TVs, monitors, and laptops. Its business overlaps with SK keyfoundry.

Last year, SK hynix System IC sold part of its Chinese subsidiary and began domestic workforce restructuring. Meanwhile, SK keyfoundry expanded by acquiring SK Powertech from SK Inc.

◇ Post-Acquisition Losses and Halved Revenue

Unlike its parent SK hynix, which is thriving, SK keyfoundry has struggled with poor performance. With little business overlap with SK hynix, it must secure orders from external clients. The 8-inch foundry sector was hit hard by the post-pandemic slump in IT device demand.In 2022, the year of the acquisition, prospects were positive.

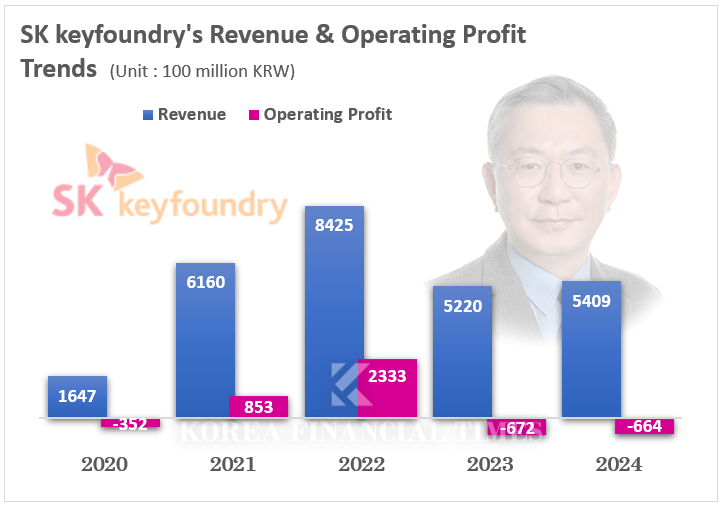

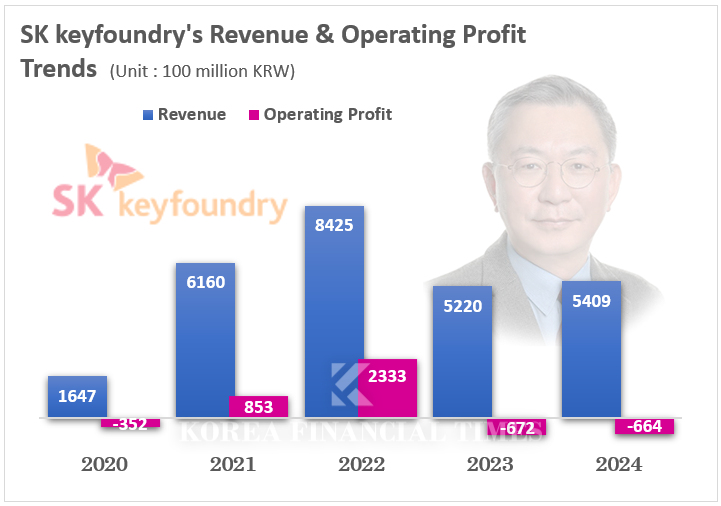

That year, SK keyfoundry posted sales of 842.5 billion KRW and operating profit of 233.3 billion KRW—a record, with sales up 37% and operating profit up 174% year-on-year.

But performance plummeted from the following year. In 2023, sales fell 38% to 522 billion KRW, and the company swung to an operating loss of 67.2 billion KRW. Last year’s results were similarly weak.

An industry insider said, “Since 2023, Chinese 8-inch foundry companies like SMIC have aggressively ramped up capacity, likely impacting Korean firms with high exposure to the Chinese market.”

◇ Betting on Power Semiconductors

SK keyfoundry’s acquisition of SK Powertech came at a time when expanding into high-value-added businesses was urgent. The deal was a win-win, aligning with SK Inc.’s need for liquidity.In March this year, SK keyfoundry signed a contract to acquire SK Inc.’s entire 98.59% stake in SK Powertech for 25 billion KRW.

SK Powertech specializes in silicon carbide (SiC) power semiconductors, and was acquired by SK Inc. in 2022. Power semiconductors are essential for controlling current and power conversion in electric vehicles, electronics, and 5G networks. SiC is a new material that offers less power conversion loss at high voltage, current, and temperature compared to conventional silicon.

SK keyfoundry plans to source SiC wafers from SK Siltron, manufacture products, and supply them to the group’s battery affiliates, investing accordingly.

However, during a portfolio rebalancing, SK Siltron was put up for sale, prompting the sale of SK Powertech as well. Ultimately, instead of an external sale, SK hynix—flush with liquidity—indirectly absorbed the business.

◇ Foundry Specialist at the Helm

SK keyfoundry’s board was filled with SK hynix personnel immediately after the August 2022 acquisition, including foundry expert CEO Lee Dong-jae, Kim Dal-joo (Growth Support), Jin Bo-geon (Corporate Culture), and Choi So-jung (Corporate Development).CEO Lee Dong-jae, born in 1962, graduated from Sungkyunkwan University with a degree in electronic engineering. He started his career as a semiconductor engineer at Samsung Electronics, working there for 15 years, then spent 11 years at Singapore foundry Chartered Semiconductor (now GlobalFoundries), before returning to Korea in 2009 as head of development planning at SK Engineering & Construction (now SK ecoplant). Since 2014, he has led SK hynix’s foundry and new business divisions, served as CEO of SK hynix System IC, and now heads SK keyfoundry.

Recently, CEO Lee stated, “We will broaden our power semiconductor lineup and establish ourselves as a specialized power semiconductor foundry.”

Gwak Horyung (horr@fntimes.com)

![지방이전에 뿔난 농협 노조 4000명 광화문 집결…"이전 강요 시 금융노조 총파업 불사" [막 오른 금융권 하투(夏鬪)]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607291713380470707c96e79780124111243152.jpg&nmt=18)

![송파구 '극동' 18평, 7.5억 오른 19.5억원에 거래 [일일 신고가]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260624115142011110dd55077bc212411124362.jpg&nmt=18)

![[그래픽 뉴스] 미국 증시 새로운 키워드 'MANGOS'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202607291740382069de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)