Shin Hak-cheol, CEO and Vice Chairman of LG Chem

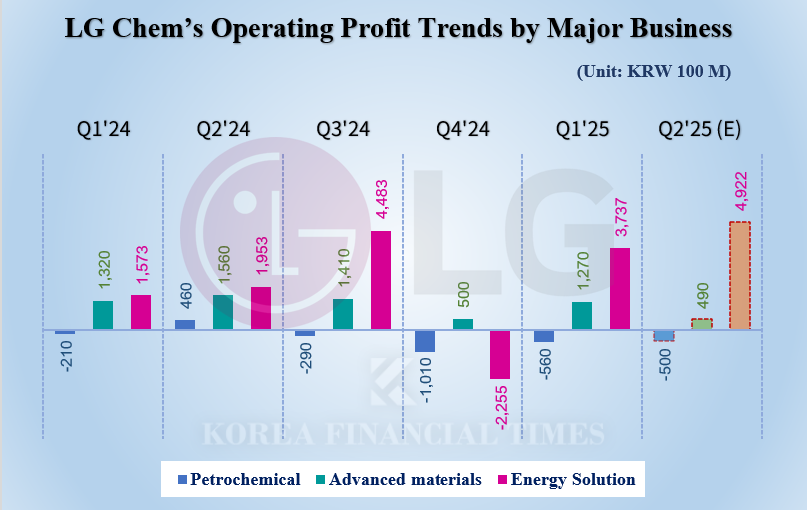

According to FnGuide on the 22nd, LG Chem is expected to post second-quarter consolidated sales of KRW 11.1849 trillion and operating profit of KRW 436.8 billion. This would mark an 8% drop in sales from the previous quarter, but a return to the black in operating profit. The company has posted losses for two consecutive quarters since the fourth quarter of last year.

Notably, the operating profit consensus jumped 21.1% in just one month to KRW 435.8 billion from KRW 359.9 billion, reflecting the earnings surprise from battery subsidiary LG Energy Solution, which reported earnings above expectations earlier this month with an operating profit of KRW 492.2 billion.

However, the outlook for LG Chem’s other businesses outside of Energy Solution remains weak.

The petrochemical division is expected to post an operating loss of about KRW 50 billion, marking four straight quarters in the red, as global demand remains sluggish and low-price competition from China continues.

The advanced materials business, which relies heavily on battery cathode materials, is expected to post operating profit of KRW 49 billion—a roughly 60% decline from the previous quarter. LG Energy Solution’s strong results were helped by U.S. subsidies, but this has had little positive spillover on materials businesses.

With core operations struggling and profitability weakening, the burden of ongoing large-scale investment in battery and other transformational businesses is increasing. LG Chem’s total borrowings have surged from about KRW 16 trillion at the end of 2022 to KRW 29.4 trillion as of the end of March 2025.

Vice Chairman Shin Hak-cheol of LG Chem to Extend Term by Two More Years... Expectations for a CEO Approaching His 70sWhy Is LG Left Behind While Holding Companies Soar?LG Display President Jeong Cheoldong Faces Test of ‘OLED Transformation’ in 2nd HalfLG Group, 'Electronics' Defensive Power Draws Attention Amid 'Chemical' Crisis

The company’s 81.8% stake in LG Energy Solution is constantly cited as a potential solution for raising funds. LG Chem previously considered selling a portion of its Energy Solution shares, but the plan was not executed. At the regular shareholders’ meeting in March, Vice Chairman Shin Hak-cheol responded to a related question by describing it as “one of several options,” neither confirming nor ruling it out.

However, Shin appears to prioritize shoring up liquidity without undermining core strategy. LG Energy Solution is a strategic asset that can benefit from future investments in next-generation technologies like solid-state batteries and U.S. Inflation Reduction Act subsidies. A hasty sell-off for short-term funding could compromise mid- to long-term growth, necessitating a cautious approach.

Instead, LG Chem is stabilizing its finances by selling non-core businesses. Last month, the company sold its water treatment filter business within the advanced materials division to a private equity fund for KRW 1.4 trillion. This business generated EBITDA (earnings before interest, taxes, depreciation, and amortization) of KRW 65 billion last year, but was classified as non-core outside the three main focuses of batteries, eco-friendly materials, and new drugs, and was thus divested. Previously, the company also offloaded its life sciences medical device business (KRW 150 billion) and display polarizer business (KRW 1 trillion) at the end of 2023.

Even if LG Chem does not sell LG Energy Solution shares directly, it is exploring alternative ways to utilize the stake for fund-raising. In May, LG Chem announced plans to raise KRW 1.4 trillion by issuing exchangeable bonds (EBs) backed by a 1.76% stake in LG Energy Solution. This appears to be a compromise—securing investment funds without a direct sell-off.

Gwak Horyung (horr@fntimes.com)

![[단독] 무신사 스탠다드 ‘산역사’ 이건오 퇴사…‘브랜드 정체성’ 전환점 맞나](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709134450047000b5b890e35c21123419294.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)