KCC (CEOs Chung Mong-jin, Chung Jae-hoon), a major precision chemical company producing paints, silicones, and advanced materials, unveiled a plan to enhance corporate value on July 3. This marks the first time in 52 years since its KOSPI listing in 1973 that KCC has announced such a value-up plan.

The Core Issue: Financial Assets and Interest Costs

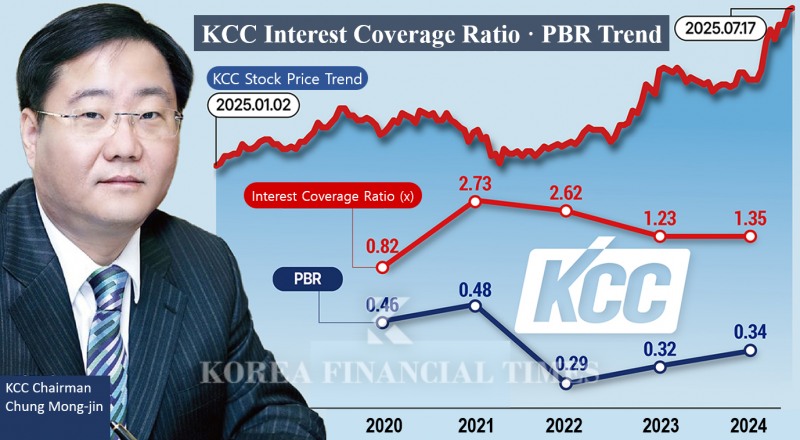

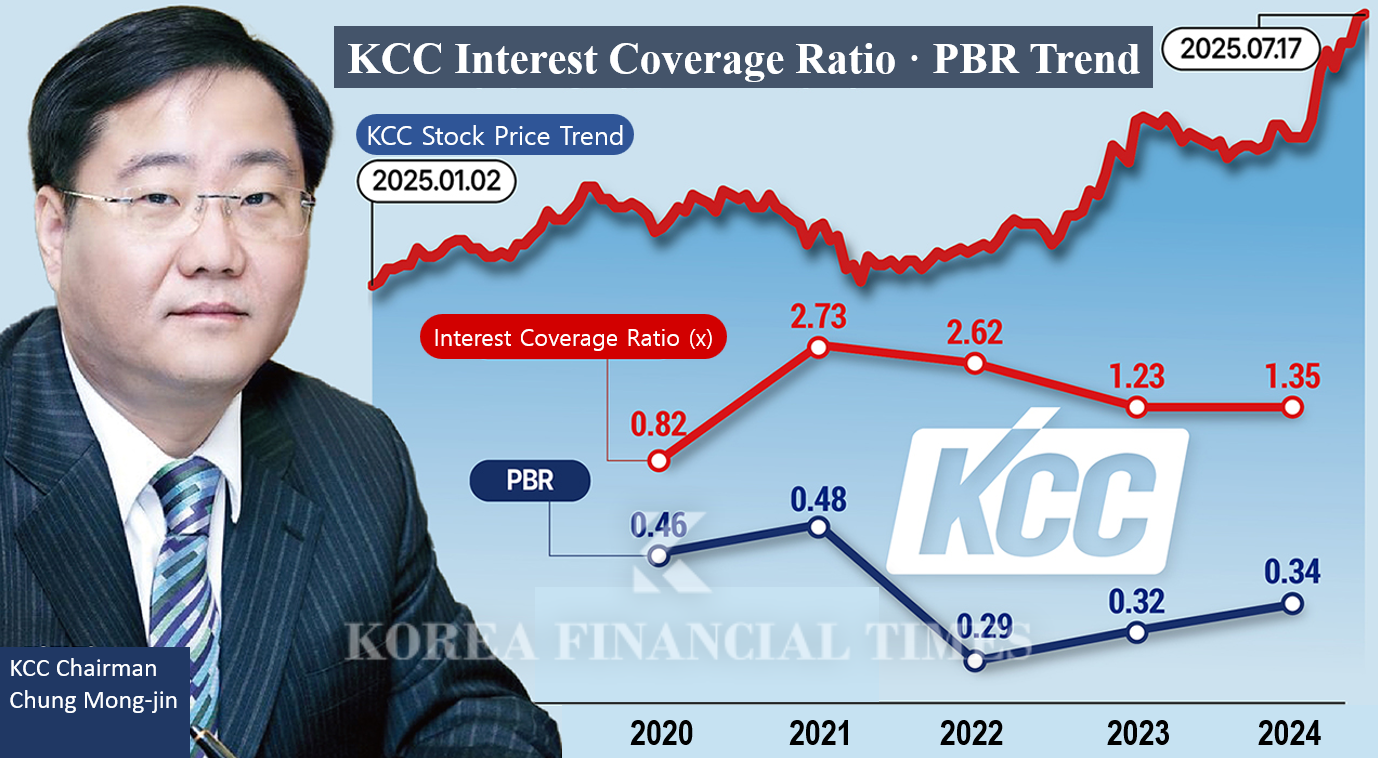

KCC aims to achieve a price-to-book ratio (PBR) above 1.0, interest coverage ratio above 2.0, sales of KRW 10 trillion, and an operating profit margin of 10% by 2030.At the end of last year, KCC’s PBR was only 0.34. After falling from 0.48 in 2021 to 0.29 in 2022, it edged up to 0.32 in 2023. PBR, calculated as share price divided by book value per share (BPS), indicates how much the market values a company relative to its net assets. A PBR above 1 suggests the stock commands a premium or is overvalued, while a figure below 1 signals undervaluation.

KCC’s unusually low PBR is due to its unique financial structure, which includes a large proportion of financial assets. Looking at the financial figures alone, KCC appears to be as much an asset manager as a manufacturer of building materials, paints, and silicones. Currently, KCC holds stakes in 36 companies, including a 10.01% share in Samsung C&T and a 3.91% stake in Korea Shipbuilding & Offshore Engineering.

At the end of 2023, KCC’s consolidated total assets stood at KRW 13.1086 trillion. Of this, financial assets accounted for KRW 5.1546 trillion (39.32% of total assets), while tangible assets—core to its main business—amounted to KRW 3.5255 trillion (26.89%).

A securities industry official noted, “When the share prices of companies in KCC’s investment portfolio rise, so do its financial income and net profit. Since late March, Samsung C&T’s share price has surged over 50%, and Korea Shipbuilding & Offshore Engineering’ has risen about 60%.”

However, KCC’s growing headache is its ballooning interest expenses. After acquiring U.S. silicone manufacturer Momentive Performance Materials (Momentive) in 2019 through special purpose company MOM Holding Company, KCC has been burdened by heavy interest costs linked to increased net debt.

Total borrowings, previously stable at around KRW 2 trillion, now exceed KRW 5 trillion. At the end of 2023, KCC’s consolidated borrowings stood at KRW 5.3 trillion, rising to KRW 5.6 trillion in the first quarter of this year.

Interest expenses reached KRW 347.8 billion at the end of last year, equivalent to 74% of operating profit. In the first quarter, interest costs amounted to KRW 78.9 billion, or 76% of operating profit.

The interest coverage ratio, which indicates debt-servicing capacity, is now at a somewhat precarious level. A ratio below 1.5x signals repayment risk. Last year, KCC’s interest coverage ratio was 1.35x—a sharp decline from 10x in 2015.

To address this, KCC is actively working to improve its financial structure. This year, it completed a revaluation of its major land and investment properties. Land revaluation gains totaled KRW 1.2 trillion, while gains on investment properties reached KRW 300 billion—boosting equity by over KRW 1 trillion. As a result, the debt ratio dropped from 160% at the end of last year to 141% in the first quarter of this year.

Lee Dong-wook, an analyst at IBK Investment & Securities, explained, “KCC repaid about USD 400 million in debt last year, completing 25% of its acquisition financing repayments and reducing annual interest expenses by KRW 40–50 billion.”

Recently, KCC issued KRW 882.8 billion in exchangeable bonds (EB) based on its Korea Shipbuilding & Offshore Engineering shares and added KRW 100 billion in loans, investing a total of about KRW 1 trillion in MOM Holding Company. These funds will be used to repay KRW 643.8 billion in debt borrowed from a KB Kookmin Bank consortium and other acquisition-related loans.

Park Se-ra, an analyst at Shinyoung Securities, said, “This EB issuance is expected to reduce annual interest costs by about KRW 60 billion and improve the interest coverage ratio to 1.56x.”

Treasury Stock Retirement? Or Sale of Stakes?

Market attention is now focused on how KCC will handle its treasury shares, which account for over 17% of total shares outstanding.With the likelihood of mandatory treasury stock cancellation increasing, KCC could consider maximizing shareholder value by utilizing its treasury shares. Market sources say, “If KCC cancels all its treasury shares, BPS would rise 14%, increasing shareholder value accordingly.”

However, it is unclear whether KCC will go this far. Chairman Chung Mong-jin is the largest shareholder with a 20% stake, and together with special related parties, he controls 35.61% of the company. Retaining treasury shares would further stabilize management control, so there appears to be little incentive to risk management stability by canceling them.

Indeed, KCC’s value-up plan makes no mention of treasury share cancellation. The recent EB was also based on HD Korea Shipbuilding & Offshore Engineering shares, not treasury shares.

Liquidation of financial assets is also being discussed as a way to address low PBR. According to LS Securities, selling the Samsung C&T stake to repay debt could reduce annual interest costs by about KRW 123.3 billion. Selling the HD Korea Shipbuilding & Offshore Engineering stake would generate approximately KRW 820 billion in cash, and using it to repay debt would save KRW 50.9 billion in annual interest. This would reduce interest expenses, improve net profit and ROE, and help KCC escape the low-PBR trap.

Shin Haeju (hjs0509@fntimes.com)

![[김의석의 단상] 이찬진 리스크보다 더 무서운 ‘견제 실종’](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260630162720015020fa40c3505512411124362.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)