Boston Dynamics, the robotics affiliate of Hyundai Motor Group, has come under the scope of financial authorities' dual-listing regulations. Pictured are Hyundai Motor Group Chairman Chung Eui-sun (left) and Boston Dynamics' humanoid robot "Atlas." / Photo: Generative AI

이미지 확대보기

This has also drawn attention to the potential listing of Boston Dynamics, the robotics affiliate of Hyundai Motor Group. While Boston Dynamics avoids the regulations targeting subsidiaries spun off through physical division (muljeok bunhal), it is seen as facing a difficult test of procedural validity, caught between the authorities' cross-cutting dual-listing regulations and the protection of parent-company shareholders' rights.

Financial Authorities Take Aim at Subsidiary Spin-off Listings and Dual Listings

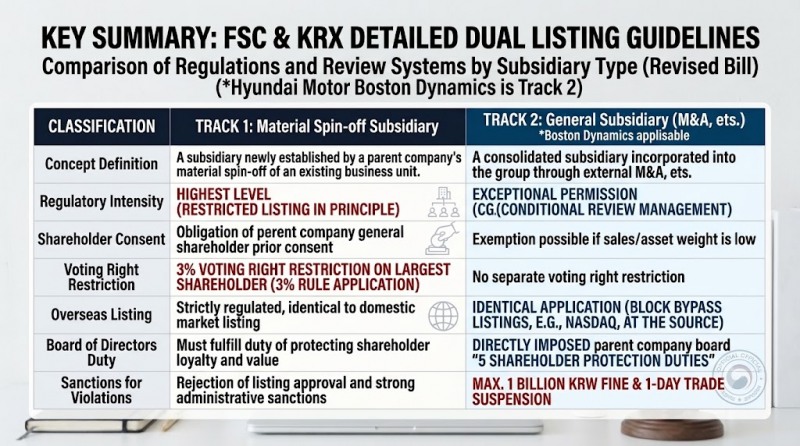

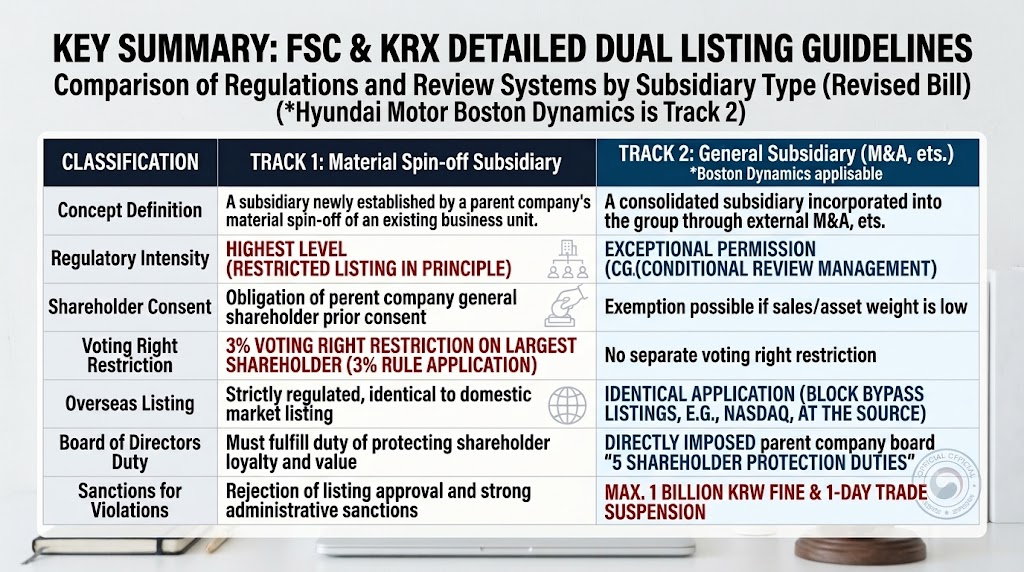

On July 6, the FSC and the KRX released detailed guidelines for the "principle ban, exception allowance" rule on dual listings. The revised rules will undergo a public notice period through July 14, after which they are expected to take final effect as early as the end of this month, pending resolutions by the Securities and Futures Commission and the FSC.The core of the revision is a requirement that parent companies obtain shareholder consent for the IPOs of subsidiaries created through physical division. Going forward, when a company seeks to list a subsidiary established this way, it must obtain the consent of the parent company's ordinary shareholders. This is because the so-called "3% rule" will apply, capping the largest shareholder's voting rights at 3% of total issued shares. Given that large conglomerates typically have difficulty securing friendly shares, this could make it virtually impossible to pass a shareholder vote.

In addition, parent company boards will be subject to five shareholder-fiduciary obligations when listing a subsidiary, including conducting a shareholder impact assessment. The five obligations are: ▲conducting a shareholder impact assessment; ▲preparing sufficient shareholder protection measures; ▲confirming that shareholder communication has taken place; ▲holding a board resolution for or against the listing and notifying the subsidiary; and ▲disclosing compliance with these obligations at each stage. The same requirements apply when a subsidiary is listed on an overseas exchange.

However, under an exception clause, low-weight subsidiaries — those whose revenue, operating profit, and assets are each less than 10% of the parent company's — are exempted from the shareholder consent requirement, provided a board resolution has been passed.

The revision is interpreted as part of the government's broader push to protect shareholders and curb split listings, long cited as a flaw in Korea's stock market. Large Korean conglomerates have long spun off core business units through physical division into separate corporate entities, then relisted them to raise capital through public offerings. In the process, parent company shareholders have repeatedly been criticized as bearing the cost of a "parent company discount," in which the value of their stake in a profitable business is diluted.

In particular, the revision divides dual listings into two categories — subsidiaries created through physical division and "general subsidiaries" brought in through mergers and acquisitions — creating a tightly structured regulatory framework. By directly linking the board's "duty to protect shareholders," as specified under the revised Commercial Act, to the listing review process, the rule is regarded as one of the strongest regulations in the history of Korea's capital markets, in that it institutionally checks unilateral listing decisions made solely for the benefit of controlling shareholders.

Stock Down 40% in a Month—Is Hyundai Mobis' 'Robot Fantasy' Falling Apart?Why Did Hyundai's Sales 'Sharply Decline'?... A Misjudgment by CEO Muñoz?Hyundai Motor Group Chairman Mulls Deepening Boston Dynamics IPO DilemmaHyundai Wia Bets on Robots and EVs—With an Eye on SuccessionNVIDIA's Huang Visits Hyundai HQ, Hails "Hyundai's Time" in the Age of Physical AI

One corporate-sector source said, "Under the current government's stance, the stock market's focus is squarely on the erosion of shareholder value." The source added, "This revision amounts to a declaration that when a listed company seeks to additionally list a subsidiary it controls, listing approval itself will not be granted unless it passes the now-stricter governance review and shareholder protection procedures."

Hyundai Motor's Acquired Subsidiary Boston Dynamics Falls Within Regulatory Scope

The government's revised rules have also drawn attention to whether Hyundai Motor Group will proceed with listing Boston Dynamics. According to industry sources, Hyundai Motor Group is known to have begun preliminary preparations for a Boston Dynamics listing this year, including forming a task force led by Vice Chairman Chang Jae-hoon.Boston Dynamics was not created by splitting off an existing Hyundai Motor business unit. It is an "externally acquired M&A entity," having been acquired in 2021 from SoftBank at an 80% stake for approximately KRW 1 trillion, and under the revised rules it is classified as subject to review as a "general subsidiary" for dual-listing purposes.

As a result, it is relatively free from the shareholder consent requirement that applies to dual listings of subsidiaries created through physical division, and it can be listed at home or abroad simply by passing securities registration statement review. Some also argue that, under the exception clause, since Boston Dynamics still accounts for only a marginal share of Hyundai Motor Group's revenue and operating profit, the path toward an overseas listing has actually gained momentum.

The issue is whether the securities registration statement will pass review. Given that the government is focused on protecting shareholders' rights, there is a strong likelihood that authorities could slow the listing by declining to accept the registration statement.

In January of this year, Hyundai Motor unveiled Boston Dynamics' humanoid robot "Atlas" at CES 2026 and declared its transformation into a robotics company. Since then, shares of Hyundai Motor as well as Kia, Hyundai Mobis, and Hyundai Glovis — all of which hold stakes in Boston Dynamics — along with other robotics-related Hyundai Motor Group affiliates, have surged.

Ordinary retail shareholders did not buy Hyundai Motor Group stock solely to receive high dividends from strong car sales. Rather, the growth potential of Boston Dynamics' physical AI and humanoid robot (Atlas) had already been priced into Hyundai Motor's stock as a "future premium."

For shareholders who invested in Hyundai Motor based on this future growth driver, a separate listing of this valuable asset could subject the parent company's stock to a discount, or value dilution.

A similar case in fact occurred at LS Group. LS Group had planned to list Essex Solutions, a U.S. company it had acquired and grown, on the domestic stock market. However, it withdrew the listing after facing intense dual-listing controversy and backlash from minority shareholders.

Hyundai Motor thus finds itself caught in a complex calculation between accelerating its future transition into robotics and protecting shareholders' rights.

Beyond a simple subsidiary listing, the Boston Dynamics IPO is also viewed as central to Chairman Chung Eui-sun's succession within the group and to resolving its circular shareholding governance structure. This is because the prevailing view is that Chung, who holds an approximately 22% stake in Boston Dynamics, would monetize his stake through a secondary offering of existing shares during the listing process, and use the proceeds to purchase stakes in affiliates such as Hyundai Mobis, which sit at the top of the group's governance structure.

A corporate-sector source commented, "Ironically, the 'dual-listing guidelines' established by the government have put Hyundai Motor in a position where it must prove it has advanced, board-centered governance and shareholder-friendly policies." The source added, "Ultimately, the key will be how genuine the measures Hyundai Motor puts forward to protect shareholders' rights are when it lists Boston Dynamics."

A Hyundai Motor representative said regarding the future listing of Boston Dynamics, "Nothing has been specifically decided yet."

Kim JaeHun (rlqm93@fntimes.com)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)