According to Alteogen on May 20, the company is currently in discussions for a strategic collaboration with a global top 10 auto-injector manufacturer. After signing a Material Transfer Agreement (MTA) and conducting joint research, both companies confirmed that combining high-dose SC therapeutic formulations with an auto-injector is technically feasible.

Based on these results, Alteogen plans to proceed with a strategic partnership to secure differentiated technology. This discussion is expected to be further detailed at ‘BIO USA 2025,’ a global bio event to be held in Boston, USA, from June 16 to 19.

An auto-injector is a device that allows medication to be administered automatically by simply placing the device on the skin and pressing a button, without complicated procedures. This enables patients, rather than healthcare professionals, to easily self-administer medication. Key features include the ability to pre-set the dosage, injection speed, and depth.

Due to its user-friendly nature, the application of auto-injector technology to pharmaceuticals has been increasing in the global bio industry. In 2019, Celltrion Pharm introduced auto-injector production facilities for Remsima SC. Aprogen also attracted attention in 2022 by developing an auto-injector device for its Humira biosimilar. According to the Ministry of Food and Drug Safety, the global auto-injector market is expected to grow at an average annual rate of 11.8%, from USD 3.6 billion (approximately KRW 5 trillion) in 2021 to USD 7.9 billion (approximately KRW 11 trillion) by 2028.

Alteogen is also focusing on the convenience and market potential of auto-injectors. A company representative stated, “Currently, therapeutic drugs are generally shifting to high-dose formulations, and auto-injectors can greatly increase convenience for both healthcare professionals and patients. As partners have a wider range of formulation options for their business strategies, we believe this will enhance the practicality and scalability of the Hybrozyme platform.”

Through this collaboration, Alteogen is expected to further strengthen its licensing negotiation power. Alteogen has set a management goal of achieving more than two new technology transfer deals annually and has continued to sign large-scale technology export contracts based on its Hybrozyme platform ‘ALT-B4’. Over the past six years, the total value of technology transfer contracts for ALT-B4 has exceeded KRW 10 trillion. As SC formulation therapies, which offer greater convenience than traditional intravenous (IV) injections, become the mainstream, Alteogen’s ALT-B4 is receiving increasing attention.

An Alteogen official stated, “We aim to enhance the competitiveness of the Hybrozyme platform together with the partner company’s medical device. We expect this collaboration to contribute to effective business strategy development for both current and prospective partners and to provide new methods of drug administration.”

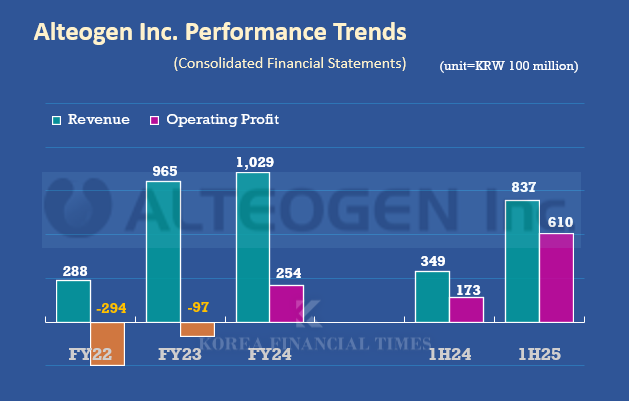

Graph=Korea Financial Times / Data Source=Financial Supervisory Service e-disclosure

Meanwhile, Alteogen continues to achieve rapid growth through technology transfer contracts. The company’s consolidated sales for the first quarter of this year reached KRW 83.7 billion, a 139.8% increase compared to the same period last year. This marks the highest quarterly performance in the company’s history. During the same period, operating profit and net profit were KRW 61.0 billion and KRW 83.0 billion, up 253.5% and 297.5% year-on-year, respectively.

Kim Nayoung, Korea Finacial Times (steaming@fntimes.com)

![[DQN] 커지는 하이닉스 의존도…SK스퀘어의 딜레마](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709203239068320141825007d12411124362.jpg&nmt=18)

![[자사주 리포트] 태광산업 vs 트러스톤](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607100742140295807de3572ddd12517950139.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)