On the 30th, E-Mart announced that it would tender 2.12 million 661,000 common shares (27.33%) of Shinsegae E&C's registered shares. Currently, E-Mart holds 5.46 million shares (70.46%) of Shinsegae E&C. It plans to buy all shares except treasury shares (171,432 shares, 2.21%) and then delist Shinsegae E&C.

Shinsegae E&C a group 'risk'...E-Mart 'bargain-basement' eyes

The purpose of E-Mart's tender offer is to simplify its governance structure and establish an efficient decision-making system. In the process, it emphasized the practice of responsible management and protecting investors holding shares of Shinsegae E&C.However, shareholders of Shinsegae E&C are not happy. Shinsegae E&C's stock price has been declining since 2021. With full group support expected, it is inevitable that E-Mart is seen as buying at a low price. It is inevitable that E-Mart will be criticized for buying at a low price.

The group's support for Shinsegae E&C began in earnest this year. In January, Shinsegae E&C merged with Shinsegae Yeongrangho Resort and secured KRW 68.6 billion in capital. In May, it issued KRW 650 billion in new capital securities backed by credit enhancements, such as the fund replenishment agreement from parent company E-Mart. And in June, the company transferred its leisure business to Chosun Hotel & Resort and received KRW 181.8 billion in proceeds. In addition, Shinsegae I&C purchased bonds (KRW 60 billion) issued by Shinsegae E&C to ease the repayment burden.

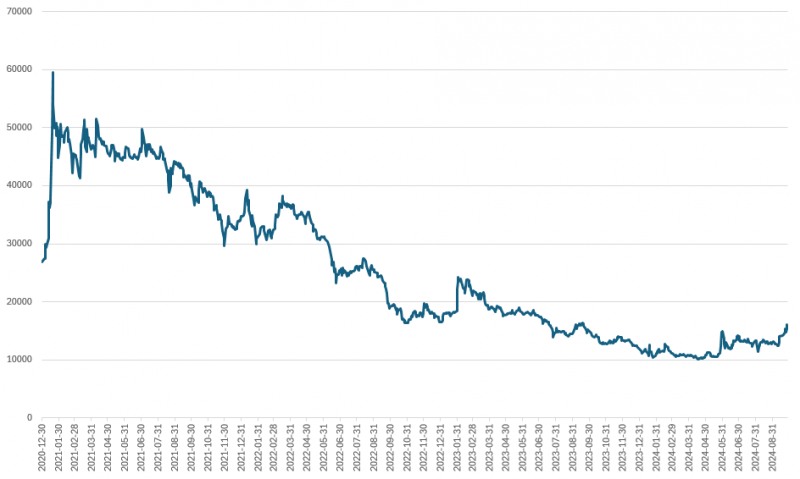

As a result of the diversionary support to E-Mart and its affiliates, Shinsegae E&C's debt-to-equity ratio fell from 976.2% at the end of last year to 145.7% at the end of the first half of this year. While improving profitability remains a challenge, the company's financial buffer has reduced the likelihood of a further downgrade following the downgrade earlier this year ('A0, negative' → 'A-, stable'). From E-Mart's point of view, Shinsegae E&C has less credit risk.

Debt-to-equity ratio(on a separate basis) trend by quarter for Shinsegae E&C./Source=Deep Search, Korea Financial Times

이미지 확대보기

Shinsegae E&C is criticized for its weak self-sustainability due to its growth through internal group transactions. Starfields, where Shinsegae E&C can secure stable revenue, are also the main business of Shinsegae Properties, in which E-Mart holds a 100% stake. Shinsegae Properties has each of the Starfield entities under its umbrella and has been making a strong push for projects such as Hwaseong International Theme Park, which recently came under fire for delayed compensation payments.

Starfield has received relatively positive reviews among the projects promoted by Chairman Chung Yong-jin. Shareholders of Shinsegae E&C had high hopes that the company would be able to withstand the share price decline and rise again in a difficult environment, but E-Mart's tender offer will dash those hopes.

Shinsegae Star REITs launches, more disappointment for Shinsegae E&C shareholders

Shinsegae Property Investment Management, a subsidiary of Shinsegae Properties, will apply for a business license for 'Shinsegae Star REITs' next month, with Starfield Hanam as the underlying asset. Shinsegae Star REITs will purchase the 51% stake in Starfield Hanam held by Shinsegae Properties, and Shinsegae Properties will receive the proceeds from the sale.Shinsegae Properties will use a portion of the proceeds to secure a stake in Shinsegae Star REITs (50%). After the REITs business license is approved, the company will go public next year.

Shinsegae Properties is focusing on the development of new Starfield complexes. As the business requires large-scale expenditures, it plans to liquidate assets and secure investor funds through the REITs.

In this process, Shinsegae E&C will benefit alongside Shinsegae Properties. If Shinsegae Properties can stabilize its financing and improve its profitability, it will be positive for E-Mart, which will acquire an additional stake in Shinsegae E&C.

Group growth centered on Shinsegae Properties is not guaranteed. However, it is good to see that the financial buffer has reduced the difficulty of financing due to the group's creditworthiness.

“E-Mart's purchase of a stake in Shinsegae E&C is unlikely to have a significant impact on immediate credit fluctuations,” said a researcher at the rating agency. ”While Shinsegae E&C's actual borrowing burden has increased, its lower debt-to-equity ratio more than offsets this and demonstrates its willingness to support the group centered on E-Mart.” “If the securitization through Shinsegae Star REITs is followed by a successful IPO, the financial structure could improve more than expected,” he added.

Lee Sungkyu (lsk0603@fntimes.com)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)