POSCO Future M, Chief Financial Officer (CFO) Jeong Dae-hyung / photo = POSCO Future M

However, Chief Financial Officer (CFO) Jeong Dae-hyung continues to face challenges. The company is grappling with persistent financial instability due to repeated profit declines and weak cash inflows relative to heavy investments. Jeong has recently begun adjusting the pace of battery-related investments, signaling a shift to a more defensive financial posture.

Known within the POSCO Group as a “focus and concentrate” strategist, Jeong is not a traditional POSCO executive. Born in 1968 and a graduate of Yonsei University’s Business Administration program, Jeong previously worked at leading consulting firms including PwC, Deloitte, and A.T. Kearney Korea, before joining Samsung’s restructuring office. He entered the POSCO Group in 2015 through the then-Value Management Office (now the Strategy & Planning Division).

Since joining POSCO, Jeong rose to Senior Vice President in 2019 and held various leadership roles in strategy and restructuring, including Head of the Corporate Strategy Office. After the launch of POSCO Holdings in 2022, he was promoted to Executive Vice President and took charge of strategic planning before becoming head of the Strategy Division the following year. He joined POSCO Future M in 2024, where he currently serves as CFO.

At the time of his appointment, POSCO Future M was already dealing with worsening performance and rising financial risks driven by the EV chasm. Given that the company serves as the core battery affiliate in the group’s future growth plan, Jeong’s capabilities in corporate strategy and financial management quickly became a focus of attention.

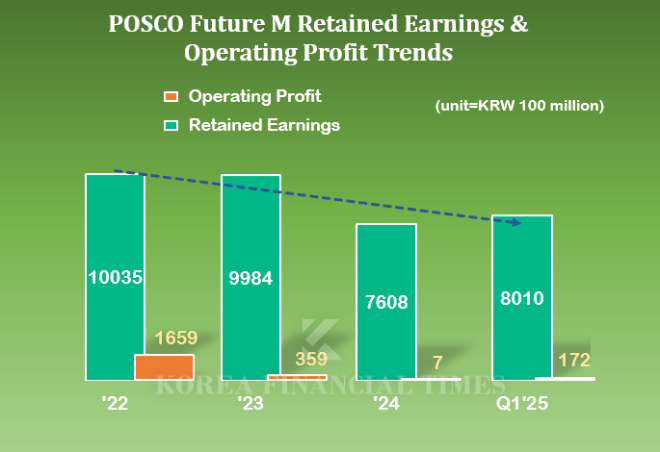

POSCO Future M’s annual operating profit peaked at KRW 165.9 billion in 2022, buoyed by growth in the EV market. However, the figure has declined for three consecutive years. Particularly in 2023, the effects of the EV chasm dragged operating profit down to just KRW 700 million.

In Q1 2024, the company posted a turnaround in operating profit with KRW 17.2 billion. However, this was largely driven by a one-off gain of KRW 52.1 billion from the sale of its cathode material plant in Gumi on February 24. According to financial data provider FnGuide, POSCO Future M’s estimated Q2 operating profit is expected to fall back to KRW 10.7 billion.

Despite deteriorating profitability, the company has continued to invest in its battery materials business to strengthen competitiveness. Major projects include the NCA cathode material plant in Gwangyang and a joint venture cathode plant in Canada with GM, aimed at bolstering its global battery supply chain.

As a result, the company’s cash reserves have rapidly declined. POSCO Future M’s cash flow from investing activities worsened from negative KRW 54.6 billion in 2022 to negative KRW 1.0314 trillion in 2023, and further to negative KRW 1.8103 trillion last year. A larger negative figure indicates greater cash outflows due to investment. While income is shrinking, rising expenditures have also eaten into retained earnings, which fell from KRW 1.0035 trillion in 2022 to KRW 998.4 billion in 2023 and KRW 760.8 billion in 2024.

Meanwhile, the company’s total borrowings, which had hovered around KRW 1 trillion, exceeded KRW 3 trillion for the first time in Q1 2024. Although retained earnings grew by about KRW 40 billion to KRW 801 billion in the same period, the amount remains insufficient to offset debt pressure.

In May, CFO Jeong responded with a capital raise of KRW 1.1 trillion to support investments and stabilize the company’s finances. According to POSCO Future M’s public filings, the company will issue 11.48 million new shares at KRW 95,800 each. Parent company POSCO Holdings will inject KRW 525.6 billion to fully acquire its 59.7% allotted share of the new stock.

While this capital raise offers some breathing room, financial pressure is likely to persist amid continued market uncertainty. Analysts note that it may take time before the investments translate into tangible returns.

Joo Min-woo, an analyst at NH Investment & Securities, stated, “Due to the likely expiration of U.S. EV tax credits, we are lowering POSCO Future M’s earnings forecast based on expectations of weaker U.S. EV sales in 2026. It will also take time to stabilize the production yield of precursor materials, which limits the company’s earnings momentum in the second half.”

CFO Jeong is also taking a more conservative stance on capital expenditures. According to POSCO Future M, the company has postponed the capital contribution dates for its joint ventures in Zhejiang, China—Zhejiang Huapoxin Energy Material Co., Ltd. and Zhejiang Pohua Xin Energy Material Co., Ltd.—from June to December.

These joint ventures were established to respond to growing local demand for precursor and cathode materials. POSCO Future M had originally planned to invest KRW 176.9 billion (50.43% stake) in Pohwa for cathode production and KRW 104.1 billion (32.49% stake) in Huapo for precursor production. However, due to the prolonged EV chasm, the capital schedule was reportedly adjusted.

The company also revised its plant construction schedule in Pohang. POSCO Future M had planned to invest KRW 461.2 billion in a new anode production facility capable of manufacturing 13,000 tons of synthetic graphite annually. While the plant was initially set for completion by June 30, the schedule has now been delayed based on internal and market conditions. A new timeline has not yet been confirmed.

Kim JaeHun (rlqm93@fntimes.com)

![“희망퇴직 아닌 구조조정”…라이나생명 노조, IT 인력 재편에 반발 집회 [막 오른 금융권 하투(夏鬪)]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260731143300046780ed56b8e1f8203251185109.jpg&nmt=18)

![[그래픽 뉴스] 미국 증시 새로운 키워드 'MANGOS'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202607291740382069de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)