HD Hyundai plans to issue a total of KRW 150 billion in corporate bonds on the 16th. The bonds will consist of KRW 70 billion with a three-year maturity, KRW 70 billion with a five-year maturity, and KRW 10 billion with a seven-year maturity. All proceeds will be used for debt repayment. If the demand forecast on the day is successful, the issuance can be increased up to KRW 180 billion.

This is the second corporate bond issuance this year. Previously, in February, HD Hyundai issued bonds worth KRW 300 billion. Although the company initially aimed to raise KRW 150 billion, the demand forecast attracted funds amounting to ten times the target, resulting in a doubling of the initial public offering amount.

At that time, the company issued bonds with a spread of about 27 basis points (bp) over government bonds, allowing it to raise funds at a relatively low interest rate.

Currently, HD Hyundai’s corporate bond credit rating is ‘A+ (Stable)’. It received A+ ratings from the three major domestic credit rating agencies: Korea Ratings, Korea Investors Service, and NICE Investors Service. All maintained the regular evaluation rating received in February this year.

HD Hyundai is the pure holding company of the group, generating revenue through dividend income from affiliates, rental income from the Global Research and Development Center (GRC), and trademark income. As of the first quarter, on an individual basis, cash and cash equivalents amounted to KRW 38.3 billion, and short-term borrowings stood at KRW 1.1649 trillion.

Park Hyun-jun, chief researcher at NICE Investors Service, stated, “It is expected that the company can smoothly respond to ordinary funding needs by utilizing rental and trademark income,” and assessed that “the company’s short-term liquidity risk is very low.”

Recently, HD Hyundai announced plans to merge HD Hyundai Construction Equipment and HD Hyundai InfraCore to launch ‘HD Construction Equipment,’ which is likely to have a positive impact on HD Hyundai’s profitability improvement.

'From Shipbuilding to Solar'... HD Hyundai’s Chung Ki-sun vs. Hanwha’s Kim Dong-kwan in a Winner-Takes-All ShowdownHD Hyundai, LIG, and KAI Team Up for 'Futuristic Unmanned Vessel Project' — Hanwha Left Out?HD Hyundai’s Two Construction Equipment Affiliates: "Even with Poor Performance, It’s for the Shareholders"

In the past, HD Hyundai acquired Doosan InfraCore (now HD Hyundai InfraCore) from Doosan Heavy Industries & Construction (now Doosan Enerbility), maintaining a structure with two listed companies operating construction equipment businesses within the group.

Through an integrated corporation worth KRW 8 trillion, the company can resolve business overlaps and simplify the governance structure, leading to strengthened competitiveness in the construction equipment sector and cost reduction effects.

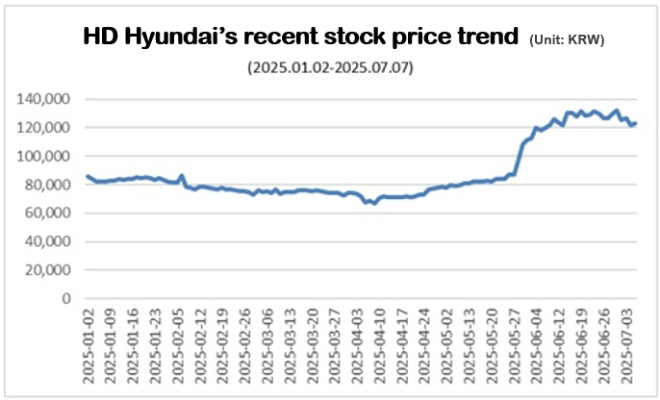

Recently, NICE Investors Service forecasted that the impact of this merger on the credit ratings of both companies would be limited and that business stability would improve. Following the announcement of the merger plan on the 1st, HD Hyundai’s stock price reached a new high for the year at KRW 132,400, and closed at KRW 134,300 on the 8th.

Shin Haeju (hjs0509@fntimes.com)

![[단독] 무신사 스탠다드 ‘산역사’ 이건오 퇴사…‘브랜드 정체성’ 전환점 맞나](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260709134450047000b5b890e35c21123419294.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)