This infographic, originally published by Korea Financial Times, has been reconstructed using generative AI / Data Source = The Compass etc.

이미지 확대보기

If one were to choose a four-character Chinese idiom that best describes Kakao (CEO Chung Shina) hese days, it would be hwabuldan-haeng (禍不單行) — "misfortunes never come alone." The company finds itself in a compound crisis, battered by a convergence of internal and external headwinds.

At a pivotal moment defined by a global paradigm shift toward artificial intelligence, Kakao's response has fallen short of market expectations. Internally, a labor dispute culminating in the company's first-ever strike in its history is intensifying. One might hardly recognize this as the same Kakao that once led the market with an aggressive expansion strategy.

Revenue Efficiency Stagnant Relative to Asset Base

For years, Kakao's growth formula rested on aggressive mergers and acquisitions, combined with the separate listings of key subsidiaries to expand its scale. The atmosphere has changed completely. The company has embarked on intensive restructuring — both human and physical — including the sale of Kakao Games and a broader rationalization of its bloated subsidiary portfolio.Industry observers note that Kakao's fundamentals had reached their limits as a result of scale expansion unaccompanied by genuine core business innovation or meaningful profitability improvements, forcing a belated effort to shed excess weight.

As of the first quarter of this year, Kakao's total assets stand at KRW 28.8 trillion, yet revenue amounts to only approximately KRW 1.9 trillion. The revenue-to-total-assets ratio — a measure of how efficiently the company generates sales from its asset base — sits at just 0.28.

This is virtually unchanged from 2021 (0.26), indicating that revenue growth has stagnated relative to asset expansion, and that the company faces a structural limitation in the utilization of its asset base. Also noteworthy is the fact that retained earnings — reflecting cumulative profitability — account for only 10% of total assets, suggesting the company has been unable to retain sufficient profits internally. When one also factors in interest expenses on total liabilities, which account for approximately 30% of total assets, it becomes clear that the pace of profitability recovery will remain constrained unless revenue efficiency improves.

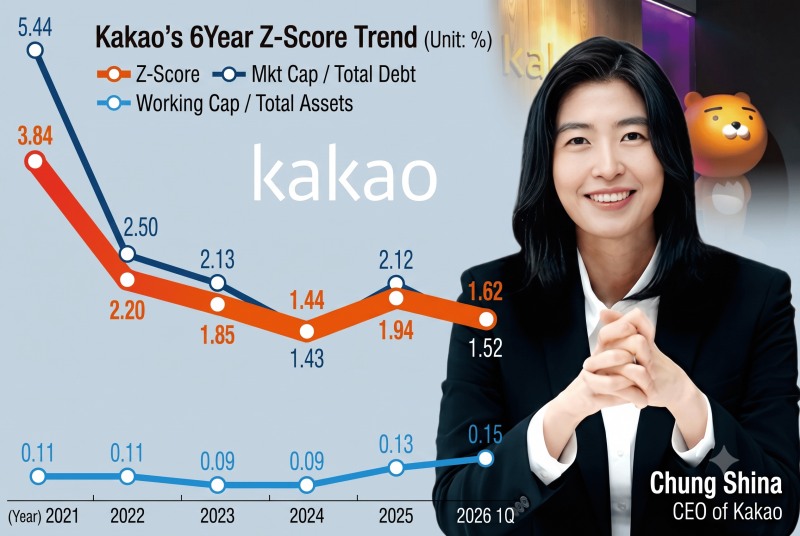

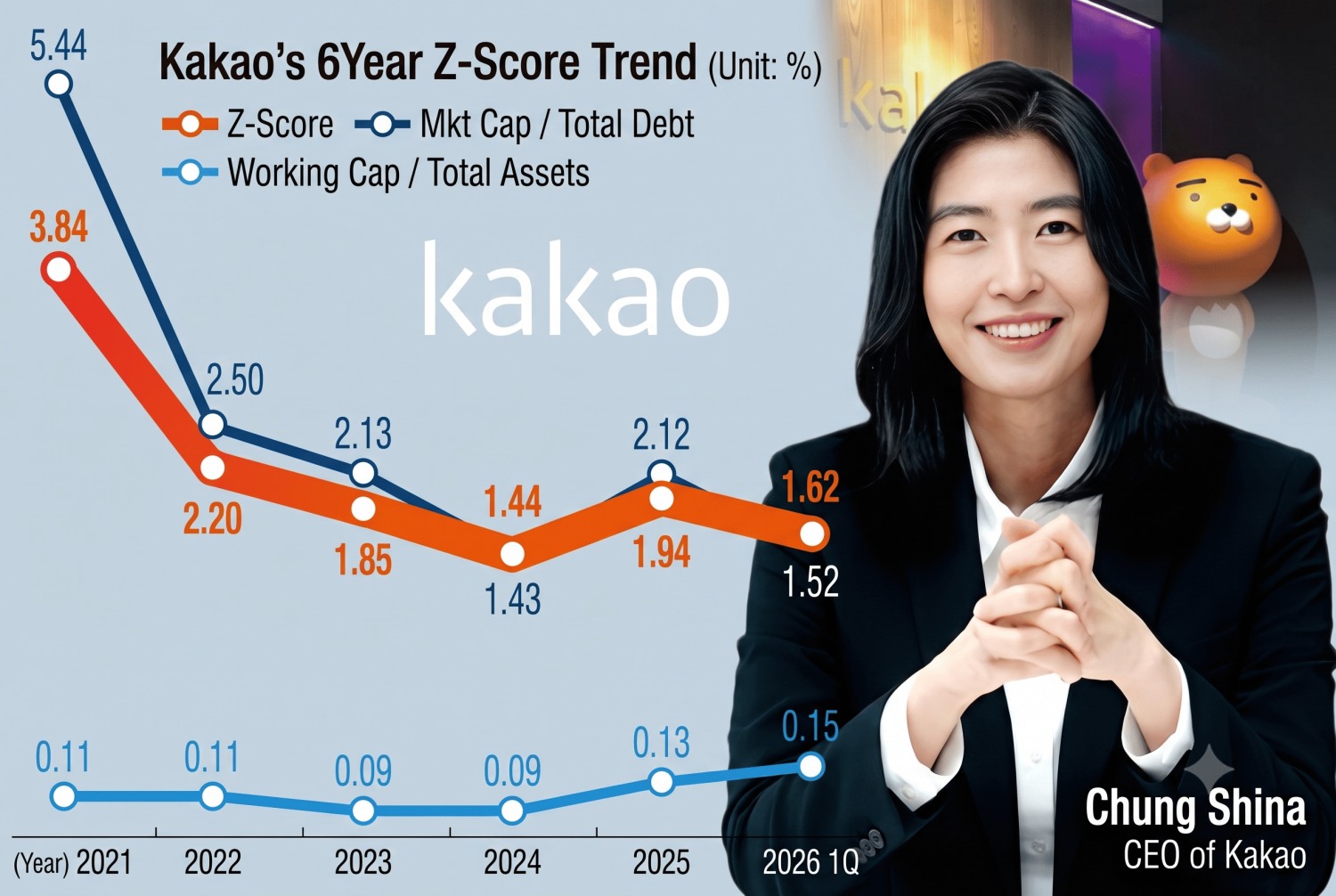

An analysis of Kakao's Z-Score conducted through the Korea Financial Times' proprietary AI data platform THE COMPASS confirmed the company's deteriorating financial health over recent years. Kakao's Z-Score stood at 3.84 in 2021 — within the "safe zone" — before falling to 2.20 in 2022, 1.85 in 2023, and 1.44 in 2024. After a modest recovery to 1.94 in 2025, the score dropped again to 1.62 as of Q1 2026, re-entering the "distress zone."

Internal and External Pressures Mount

The primary driver behind the Z-Score's decline is the excessive debt burden (total liabilities) relative to the company's market-assessed value (market capitalization).

The ratio of market capitalization to total liabilities — which measures debt levels against market valuation — plummeted from 5.44 in 2021 to 1.52 in Q1 2026. As of Q1 2026, Kakao's market capitalization stands at KRW 20.2787 trillion, less than half its level five years ago (KRW 50.1508 trillion).

Meanwhile, total liabilities have risen to KRW 13.3823 trillion, a 45% increase from KRW 9.2162 trillion in 2021. The simultaneous growth in total liabilities and contraction in market capitalization has driven a deterioration in financial soundness metrics.

The most urgent task in addressing the fractures in Kakao's financial structure is a recovery in market capitalization through a stock price rebound — yet the environment surrounding the company has rarely been more uncertain.

The most significant factor is what can only be described as a vacuum in AI momentum. Kakao currently offers the on-device AI service "Cana in KakaoTalk" and the conversational AI "ChatGPT for Kakao."

Early traffic indicators are positive. ChatGPT for Kakao has surpassed 11 million cumulative subscribers, with monthly active users (MAU) nearly doubling compared to the prior quarter. Cana in KakaoTalk has also recorded approximately 80% positive ratings for response quality in user surveys.

However, a key limitation remains: these user metrics have not yet translated into a clear business model (BM) capable of driving the company's stock price and corporate value. As the global IT industry faces mounting pressure to demonstrate the real return on investment (ROI) of AI, Kakao's AI business appears stuck at the early stage of user acquisition, with value creation lagging.

Further aggravating the situation are perceptions — even if they are partly misreading — that Kakao is being sidelined within the global AI value chain. During NVIDIA CEO Jensen Huang's recent visit to Korea, he met successively with the heads of major Korean conglomerates, including Samsung Electronics, SK, LG, Hyundai Motor, and Doosan, as well as with the chief of Kakao's rival Naver, reaffirming his commitment to strengthening alliances. Yet Kakao was conspicuously absent from that circle. Compounding this, the postponement of OpenAI CEO Sam Altman's planned visit to Korea — during which Kakao had been cited as a potential key partnership target — has dimmed expectations for any near-term momentum.

On the domestic front, the outbreak of the company's first-ever labor strike adds another risk factor. For a platform and software company whose core production asset is human capital, a prolonged labor dispute will inevitably complicate the organizational and personnel restructuring needed to respond to rapidly changing market conditions.

A transition to an AI-centric operational model requires flexibility in human capital allocation, but as union cohesion strengthens, management's strategic latitude narrows. Indeed, concerns have been raised that ongoing labor unrest could undermine the internal execution of Kakao's management reform initiatives announced this year — including a reorganization into product-centric dual divisions and the establishment of a "User First Task Force."

Dunamu Investment — a 630x Return — Offers a Ray of Hope

In the midst of an environment where Kakao's market valuation is being compressed by internal and external headwinds, the fact that short-term liquidity indicators remain robust is a positive sign. Balance sheet liquidity metrics suggest that Kakao retains the financial firepower to defend its current position.The working capital-to-total-assets ratio — a measure of near-term liquidity — rose from 0.11 in 2021 and 0.09 in 2023 to 0.13 in 2025, and further to 0.15 in Q1 2026. In Q1 2026, Kakao held current assets of KRW 14.9508 trillion against current liabilities of KRW 10.5059 trillion, securing working capital of approximately KRW 4.4–4.5 trillion.

The rising working capital ratio signals that the company is free from near-term debt pressures due within the next twelve months. It also means that, despite heightened external uncertainty, Kakao retains sufficient financial room to pursue investment in core future businesses without being weighed down by fixed-cost outlays or short-term risks.

Over the same period, the retained earnings-to-total-assets ratio — reflecting cumulative profitability — improved slightly to 0.10, based on retained earnings of KRW 2.9232 trillion, up from 0.08 in the same period last year. This suggests the company is steadily building an organic financial foundation — retaining net income earned from its core operations rather than relying excessively on external borrowings or equity stake sales, and reinvesting those earnings into future growth drivers.

Adding to this, Kakao Investment recently divested a 6.55% stake in Dunamu to Hana Financial Group for KRW 1.00325 trillion, and a 3.9% stake to Hanwha Investment & Securities for KRW 597.8 billion. Further sales of a 4.0% stake (KRW 612.8 billion) to Samsung Securities, Samsung SDS, and Samsung Card followed in quick succession.

Through these transactions, Kakao raised a total of KRW 2.21 trillion in cash. Compared to its initial investments of KRW 200 million in 2013 and KRW 3.3 billion in 2015, this represents a return of approximately 630 times the original principal — a remarkable outcome.

This amount significantly exceeds Kakao's projected consolidated free cash flow (FCF) for the current year. According to THE COMPASS, Kakao's consolidated FCF is forecast to surge from KRW 184.7 billion in 2025 to KRW 796.6 billion this year.

Notably, the stake sale proceeds are of particular significance because they fall outside the existing shareholder return guidelines (20–35% of consolidated FCF) set by CEO Chung Shina upon taking office — making them a trillion-won-scale resource unconstrained by those parameters. This effectively enables a structure in which cash generated from core operations is channeled in its entirety toward shareholder returns, while the stake sale proceeds are deployed independently for AI infrastructure investment and targeted M&A.

Kakao's corporate value warning lights may be flashing amid internal and external challenges, but through proactive asset monetization, the company has secured the financial latitude to defend against the crisis and improve its underlying business profile. Whether it can prudently resolve the strike risk and similar headwinds, and deploy its liquidity reserves at the right moment — into AI service stabilization and restructuring — to demonstrate improved asset efficiency, will be the decisive factor in restoring capital market confidence.

Jeong Chaeyun (chaeyun@fntimes.com)

![[DCM] 미래에셋증권, 첫 공모CP 1.26조…회사채 대신 택한 배경은](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260630151601033060141825007d12411124362.jpg&nmt=18)

![NHN KCP, AI·스테이블코인으로 미래 결제 인프라 선점 [PG사 신사업 전략]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202606291553470418709efc5ce4ae1182351386.jpg&nmt=18)

![STO 시장 개막 초읽기…“조각투자 장외거래소 안정적 생태계 구축 관건” [KDX vs NXT컨소 본인가 레이스 (하)]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202606291513040709700f4390e77d211234194120.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)