This infographic, originally published by Korea Financial Times, has been reconstructed using generative AI (Gemini).

이미지 확대보기

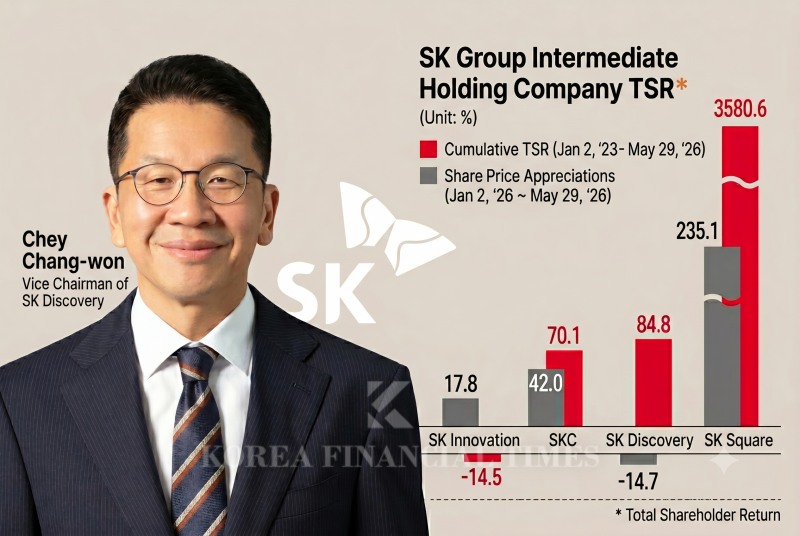

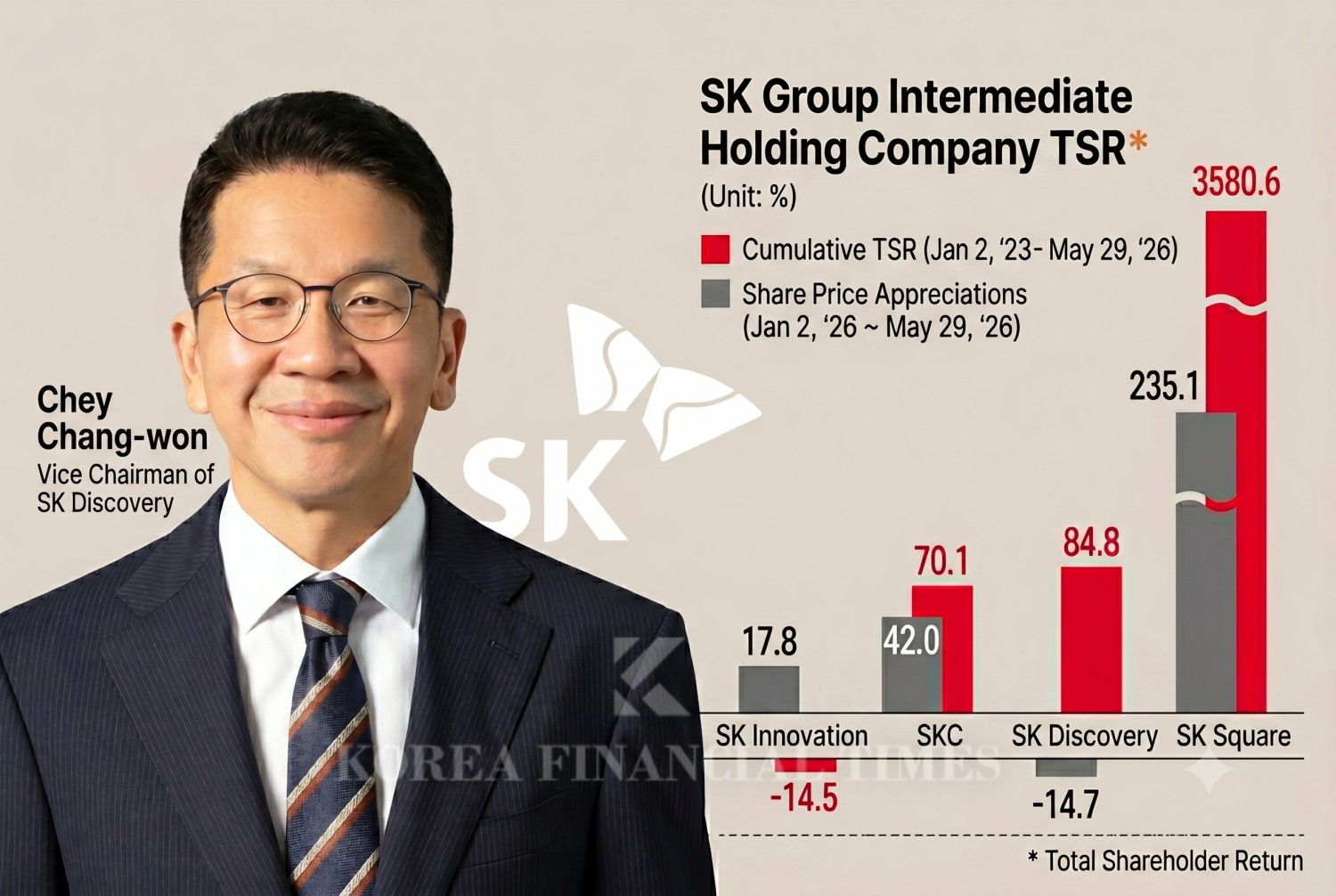

The shareholder-value scorecards of SK Group's four major intermediate holding companies are diverging sharply. Attention is focused in particular on whether SK Discovery—which has thus far weathered conditions with high dividends as its weapon—can recover future growth momentum and regain upward momentum in its share price.

SK Discovery, led by Vice Chairman Chey Chang-won, has maintained a solid total shareholder return (TSR) on the back of a high dividend yield grounded in its stable LPG (liquefied petroleum gas) business. Yet this stands in contrast to the recent rebound of other intermediate holding companies centered on batteries and semiconductors—such as SK Innovation and SKC—driven by group-level rebalancing and expectations for new businesses.

Securing cash through the sale of non-core assets and rebalancing its portfolio, while proving a clear growth engine capable of leading the market, is cited as its task going forward.

Korea Financial Times calculated the TSR of SK Group's intermediate holding companies using the corporate data platform "DeepSearch." TSR is the sum of the share-price change rate and the dividend yield over a given period. It is an indicator showing the actual total return a shareholder can earn by investing in a particular company.

The analysis period spans roughly three years and five months, from January 2, 2023, to May 29, 2026. The period was set from 2023 onward, when the KOSPI index entered a recovery phase right after plunging in the wake of the global interest-rate hikes of 2022.

During this period, SK Group transitioned to a four-major-intermediate-holding-company system through a "Deep Change (fundamental transformation)" that absorbed and merged key affiliates. SK Square was born from that restructuring. It took over non-telecom segments such as SK Telecom's semiconductor affiliate SK Hynix and TMAP Mobility.

As a result, returns ranked as follows: SK Square (3,580.6%), SK Discovery (84.8%), SKC (70.1%), and SK Innovation (-14.5%). The holding company SK Inc. posted 270.4%, a higher return than the other intermediate holding companies excluding SK Square.

SK Networks Completes Business Overhaul, Enters 'AI Monetization' PhaseSK hynix Eyes KRW 40 Trillion in Q1 Operating Profit — Is AI Ushering in a Long-Term Boom?SK Hynix Weighs Growth Over Governance in Treasury Share Strategy [Treasury Share Report]Beyond Hynix: SK's Three-Company AI Alliance Eyes Full-Stack Jackpot

The backdrop to SK Square's overwhelming return is the impact of SK Hynix's share price, which surged on the artificial intelligence (AI) semiconductor boom. The analysis is that, because institutional investors face restrictions when investing more than a certain proportion in a single stock, SK Square—which holds a 20% stake in SK Hynix—is becoming an alternative.

A Changed Mood This Year

SK Discovery has a distinctive governance structure. SK Innovation and SKC are controlled by SK Inc., whose largest shareholder is SK Group Chairman Chey Tae-won. SK Discovery, by contrast, is an independent intermediate holding company managed by the family of Vice Chairman Chey Chang-won, who holds a 51% stake.Vice Chairman Chey Chang-won is Chairman Chey Tae-won's younger cousin. Chairman Chey is the eldest son of Chey Jong-hyon, SK's second-generation chairman, while Vice Chairman Chey is the third son of founder Chey Jong-gun. Although SK Discovery is effectively run independently, it continues a "separate yet together" style of management, in practice cooperating with the SK Inc. affiliates and securing practical benefits.

SK Discovery's business portfolio includes energy, bio, and vaccines. On a consolidated revenue basis (including intra-group transactions) last year, the breakdown was: gas business (SK Gas) 92%, chemical materials (SK Chemicals' Green Chemicals division) 15%, and bio (SK Bioscience, SK Plasma) 13%.

Looking at the past four-plus years, SK Discovery's record is not bad. It posted better returns than the SK Innovation and SKC affiliates, which have partly similar portfolios.

This year, however, SK Discovery's share-price growth rate has slumped to minus 15%. This is the exact opposite of SK Innovation and SKC, which rebounded by rising 18% and 42%, respectively.

SK Innovation benefited from forecasts that the battery industry—into which tens of trillions of won in large-scale funding has been poured—has "hit bottom," as well as from group-level support such as its merger with the lucrative SK E&S.

In the case of SKC, which continues to post operating losses, expectations are growing as it recently succeeded in a well-received rights offering on the strength of its glass-substrate business, dubbed a "game changer" in the semiconductor field.

By contrast, the lack of a business that can demonstrate such future growth is cited as the backdrop to SK Discovery's recent share-price weakness. SK Chemicals is expanding investment in its recycled-plastics business, and SK Bioscience has also presented a vision of leaping into a global contract development and manufacturing organization (CDMO) over the medium to long term.

Still, the assessment is that, without showing clear earnings or leading momentum capable of shaking up the market, it falls short of drawing investors' attention.

SK Discovery's dependence on SK Gas, which still operates the LPG distribution business, remains absolute. In phases where the KOSPI index moves sideways, it benefited from SK Gas. Because it effectively monopolizes private LPG supply, a high-dividend policy enabled by stable cash generation is possible.

SK Discovery's annual TSR was 5.6% in 2023, 33.9% in 2024, and 52.4% in 2025. Of these, the dividend yield excluding the share-price growth rate was 4.3% in 2023, 4.4% in 2024, and 3.5% in 2025. The cumulative share-price growth rate is 63%, and the cumulative dividend yield reaches 21.8%. The cumulative dividend yield far outpaces those of SK Inc. (13.2%), SK Innovation (6.8%), and SKC (2.6%).

Will "Rebalancing Expert" Chey Chang-won Show His Skill?

Vice Chairman Chey Chang-won is regarded as having a cautious and conservative management style. His strengths emerge in the portfolio-rebalancing (business realignment) process—coordinating businesses among affiliates in crisis situations and boldly disposing of businesses he deems unnecessary.This is the backdrop to Vice Chairman Chey being installed as chairman of the SK SUPEX Council, the group's decision-making advisory body, in December 2023 when SK Innovation fell into a financial crisis.

So let us take a look at the SK Discovery rebalancing that Vice Chairman Chey is likely pursuing with the greatest interest.

First, he began winding down the real-estate business. Last October, he sold his entire stake in real-estate developer SK D&D to the private-equity firm Hahn & Company. SK Engineering & Construction (now SK ecoplant), a former major shareholder, had divested its stake in 2019 to avoid Fair Trade Act regulations.

In March this year, he sold his entire stake in SK Eternix—a specialist in renewable energy such as wind power, solar power, and fuel cells—to the private-equity firm KKR. The move appears to be a strategy to concentrate the eco-friendly energy business on SK Chemicals' waste-plastics business, where vertical integration is underway.

Securing cash for large-scale investment was also an urgent matter. According to "The Compass," the artificial intelligence (AI) data platform built in-house by Korea Financial Times, SK Discovery's free cash flow (FCF, including depreciation) recorded a deficit of nearly KRW 450 billion every year from 2022 to 2025. At least it is expected to find some breathing room, having turned to a surplus this year as international LPG contract prices surged in the wake of the Middle East war.

Gwak Horyung (horr@fntimes.com)

![‘삼전 불황’ 경험으로 삼성SDI 버티기 돌입한 오재균 [나는 CFO다]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260613000702036160dd55077bc212411124362.jpg&nmt=18)

![전기로 1위의 저주...‘친환경 부메랑’ 제대로 맞은 현대제철 [Z-스코어 기업가치 바로보기]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260612150606034240dd55077bc212411124362.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)