Immediately following his return, Samsung's semiconductor division saw a rebound in the second quarter of last year, recording an operating profit of 6.5 trillion Korean Won. However, Vice Chairman Jun insightfully remarked, "This was not a recovery of fundamental competitiveness but merely an improvement in market conditions. Relying solely on market fluctuations will only lead to a recurrence of the same situation."

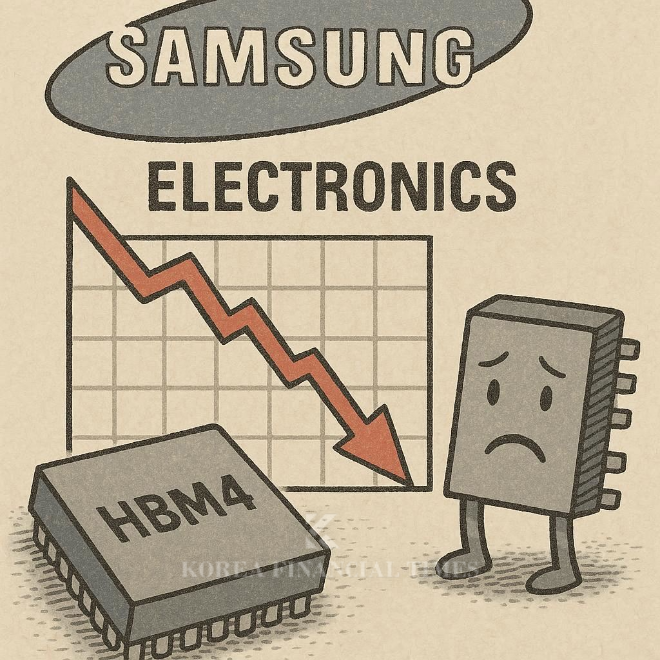

His apprehension proved prescient. Samsung Electronics' semiconductor operating profit subsequently declined for four consecutive quarters. In the second quarter of this year, operating profit plummeted by a stark 94% year-on-year to 400 billion Korean Won . This significant underperformance is primarily attributed to falling behind in the High Bandwidth Memory (HBM) market, a critical component in the burgeoning AI era.

This starkly contrasts with rival SK Hynix, which posted an operating profit of 9.2 trillion Korean Won in the second quarter, a figure 23 times greater than Samsung's semiconductor division . Consequently, Samsung, which has consistently held the top position in DRAM since 1992, now finds itself on the brink of losing that leadership. According to DRAMeXchange, Samsung's DRAM market share in the first half of this year dropped by 8.8 percentage points from the end of last year, reaching 32.7%.

Nevertheless, Samsung Electronics has not been idle. Vice Chairman Jun is reported to have made consecutive visits to Silicon Valley in the U.S. in May and June, engaging in discussions with Nvidia concerning HBM supply. Furthermore, from late July, Samsung Electronics Chairman Lee Jae-yong directly embarked on a two-week business trip to the U.S., where he reportedly met with Nvidia CEO Jensen Huang. Upon his return, when questioned by the press about the details of his trip, Chairman Lee succinctly stated, "I came back having prepared for next year's business."

Jun Young-hyun, Vice Chairman of Samsung Electronics

The semiconductor industry anticipates that the competition for next-generation HBM will intensify from next year. This is primarily driven by Nvidia's planned launch of 'Rubin,' the successor to its Blackwell AI semiconductor Graphics Processing Unit (GPU), in the latter half of 2026.

Rubin will feature the next-generation HBM4. In the HBM3e market, integrated into Blackwell, SK Hynix currently dominates with a 75% market share. Kiwoom Securities analyst Park Yu-ak projects that "HBM4 market share will be intensely competitive among suppliers, likely settling at around 50% for SK Hynix, 30% for Samsung Electronics, and 20% for Micron." Should Samsung secure a significant share in HBM4, it would undoubtedly accelerate its performance recovery.

관련기사

Conversely, SK Hynix will outsource the design and mass production of the base die for HBM4 to Taiwan's TSMC. At its second-quarter earnings call on July 31st, Samsung Electronics announced that it had "completed the development of 10nm-class 6th-generation (1c) nano process HBM4 and has already shipped samples to key customers (Nvidia)."

However, variables remain. The critical factor lies in Nvidia's quality certification results. Although there are reports of positive signals from initial tests, premature optimism is unwarranted given past delays in HBM3e certification.

The outcome of HBM4 quality certification is expected to become clearer around the first quarter of next year. An industry insider commented, "Nvidia appears to be conducting tests for as long as possible to gain leverage in price negotiations," adding, "Rather than allocating volume to a specific vendor, they will consider quality and price comprehensively."

Gwak Horyung (horr@fntimes.com)

![지방이전에 뿔난 농협 노조 4000명 광화문 집결…"이전 강요 시 금융노조 총파업 불사" [막 오른 금융권 하투(夏鬪)]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202607291713380470707c96e79780124111243152.jpg&nmt=18)

![송파구 '극동' 18평, 7.5억 오른 19.5억원에 거래 [일일 신고가]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260624115142011110dd55077bc212411124362.jpg&nmt=18)

![[그래픽 뉴스] 미국 증시 새로운 키워드 'MANGOS'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202607291740382069de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)