CJ CheilJedang (CEO Kang Shin-ho), which has taken the global dining table by storm with its Bibigo brand, has suddenly fallen into a period of low growth. The company’s core bio business, especially in China, has suffered amid challenging market conditions. In response, CJ CheilJedang is refocusing on its main business of “K-food,” while building large-scale production bases in Western markets such as the United States and Europe. At the same time, the company has ramped up dividends to elevate what it sees as an undervalued stock price and to strengthen shareholder returns.

Samyang Foods became a “blue-chip” trading above KRW 1 million per share and broke through the KRW 10 trillion market cap barrier, while Orion reached a record-high operating profit margin and market capitalization of KRW 4 trillion. During this period, CJ CheilJedang’s shares declined, reducing its market cap to the KRW 3 trillion range.

Domestically, prolonged consumption stagnation has weighed on earnings. CJ CheilJedang’s domestic food sales dropped from KRW 5.9231 trillion in 2022, to KRW 5.8783 trillion in 2023, and KRW 5.7716 trillion in 2024.

In contrast, overseas food sales have steadily risen: KRW 5.1811 trillion in 2022, KRW 5.3861 trillion in 2023, and KRW 5.5814 trillion in 2024. With the domestic business still accounting for more than 50% of sales, the consumption slump has dampened overall performance.

Beyond weak domestic demand, a sluggish bio business has also been a significant drag. The company’s green bio operations, notably affected by the Chinese economy, specialize in feed amino acids such as lysine and threonine. Both of its production facilities are located in China, where local companies have ramped up lysine output, leading to oversupply. As a result, bio business sales fell from KRW 4.854 trillion in 2022 to KRW 4.2095 trillion in 2024, down 13.3% over two years.

A CJ CheilJedang official stated, “There are currently no plans to sell the bio business,” emphasizing, “Strategic alternatives are being considered for CJ Feed & Care’s business restructuring, but nothing has been finalized.”

Despite these challenges, CJ CheilJedang has continued a policy of high dividends, consistently increasing payouts. Since 2022, the company has implemented quarterly dividends.

The payout ratio has mostly stayed around 50–55% of the annual dividend amount, but from this year, the company plans to raise this to around 75%. Further, over the next three years, CJ CheilJedang has pledged to return at least 25% of separate net income (excluding non-recurring items) to shareholders. The annual dividend will be determined by taking into account investments, financial structure, and management conditions, with an emphasis on stability.

Over the past decade, CJ CheilJedang’s total dividends have grown by an average of 12% per year. The dividend per share has tripled from KRW 2,000 in 2014 to KRW 6,000 in 2024.

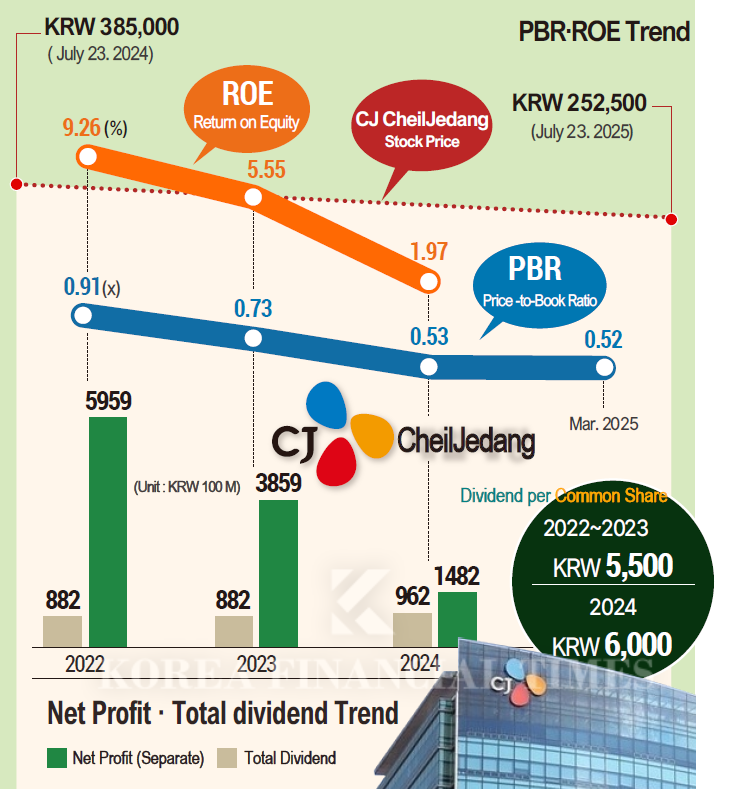

Indeed, the payout ratio (consolidated basis) surged from 14.8% in 2022 to 22.9% in 2023, and 64.9% in 2024. As earnings slowed, net income (attributable to owners of the parent) plunged from KRW 595.9 billion in 2022 to KRW 148.2 billion in 2024. Yet, dividend payments rose from KRW 88.2 billion to KRW 96.2 billion.

Including CJ Logistics, total sales over the past three years were relatively flat: KRW 30.0795 trillion in 2022, KRW 29.0235 trillion in 2023, and KRW 29.0359 trillion in 2024.

CJ CheilJedang’s return on equity (ROE) declined steadily from 9.26% in 2022, to 5.55% in 2023, and 1.97% in 2024. Conversely, its price-to-earnings ratio (PER) rose from 10.46 times in 2022, to 13.75 in 2023, and 28.25 in 2024.

ROE measures how effectively a company generates profits from its own capital; a higher figure indicates greater profitability. PER indicates whether a stock is undervalued or overvalued relative to its earnings: a lower PER suggests undervaluation, while a higher figure implies overvaluation.

Based on this, it appears that CJ CheilJedang’s decade-long high dividend policy has propped up the PER, regardless of the company’s performance.

CJ CheilJedang’s retained earnings remain robust, at KRW 5.4515 trillion in 2022, KRW 5.7315 trillion in 2023, and KRW 5.7471 trillion in 2024.

Nonetheless, the share price has continued to struggle amid this low-growth phase, falling from KRW 378,500 (closing price, July 25, 2024) to KRW 249,000 on July 25, 2025—a 34.2% decline over the year.

Though long considered a prime beneficiary of value-up trends in the food sector, CJ CheilJedang failed to make the “Korea Value-Up Index” due to an excessively low ROE. Despite this, the company remains committed to its high-dividend policy.

CEO Kang Shin-ho said, “We will enhance corporate value by achieving financial results and upgrading our long-term business portfolio, while actively communicating with shareholders and expanding return policies. To strengthen market confidence, we have established a new dividend policy for the three-year period from 2024 to 2026, increasing both the payout ratio and the weight of quarterly dividends.”

Son Wontae (tellme@fntimes.com)

![기관 '삼성전기'·외인 '삼성물산'·개인 'SK하이닉스' 1위 [주간 코스피 순매수- 2026년 8월3일~8월7일]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260808120121012140179ad4390711823565238.jpg&nmt=18)

![[김의석의 단상] 왜 지금 ‘윤종규 리더십’인가](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260807170724038790c1c16452b012411124362.jpg&nmt=18)

![기관 '심텍'·외인 'HLB'·개인 '대한광통신' 1위 [주간 코스닥 순매수- 2026년 8월3일~8월7일]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260808121054026860179ad4390711823565238.jpg&nmt=18)

![12개월 최고 연 6.50%…애큐온저축은행 '처음만난적금'[이주의 저축은행 적금금리-8월 2주]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202608090009240069907c96e797801121481643.jpg&nmt=18)

![3년 만에 글로벌 1위, 로봇판 화웨이의 탄생 :애지봇(AgiBot·智元机器人)의 시대 [전병서의 中 첨단기업 리포트⑬]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260807173916059060c1c16452b012411124362.jpg&nmt=18)

![[그래픽 뉴스] ISA 대개편! 나에게 유리한 계좌는?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202608041713155615de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 미국 증시 새로운 키워드 'MANGOS'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202607291740382069de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)