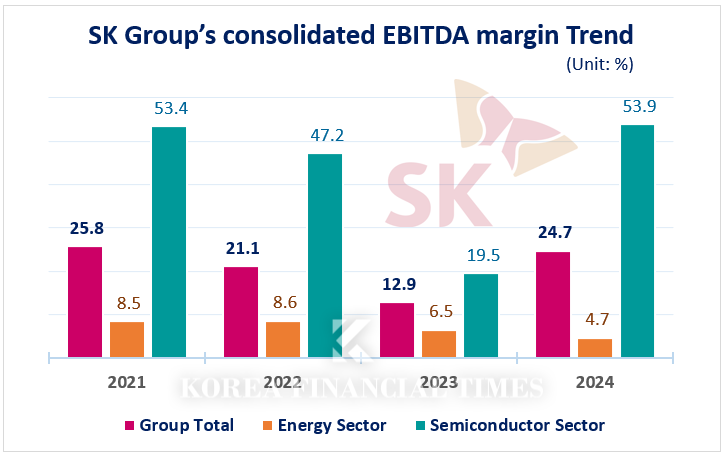

According to the Korea Ratings data package, SK Group’s consolidated EBITDA margin reached 23.8% in 2024, nearly doubling from 12.3% in 2023 in just one year.

The EBITDA margin is the ratio of EBITDA to sales revenue. While similar to the operating profit margin, it reflects profitability excluding depreciation, interest expenses, and taxes, thus indicating the actual cash-generating capability.

* Energy Sector = SK Innovation, SKC, SK Gas, SK Chemicals, SK Advanced ; * Semiconductor Sector = SK hynix, SK Siltron / Data Source: Korea Investors Service, Inc.(KIS) Data Package

이미지 확대보기

SK Group’s main concern is the pronounced reliance on semiconductors. The EBITDA margin of semiconductor affiliates such as SK hynix and SK siltron surged from 19.5% in 2023 to 53.9% in 2024. In contrast, the EBITDA margin of the energy affiliates, which account for the largest portion of sales, declined from 6.5% to 4.7% over the same period.

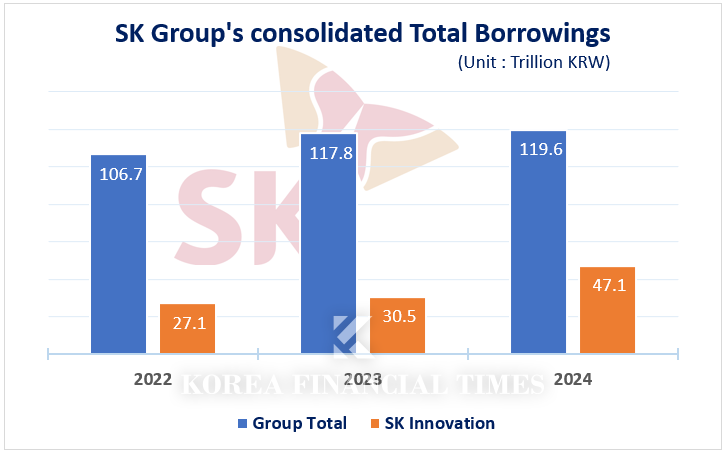

SK innovation, which accounts for 81% of sales among SK’s energy affiliates, is experiencing poor performance across all major business segments, including refining, chemicals, and batteries. As a result, even though its cash generation capacity is weakening, it faces a structural burden to continue large-scale investments such as battery facility expansions.

Consequently, dependence on external financing has increased, leading to a vicious cycle of expanding borrowings.

In fact, SK innovation’s consolidated total borrowings surged by approximately 54%, from KRW 30.535 trillion in 2023 to KRW 47.129 trillion in 2024.

SK hynix Posts Over KRW 7 Trillion in Q1 Operating Profit… “Strong Demand for HBM to Persist”SK Innovation's Credit Rating Downgrade Spiral... Battery Division Faces KRW 1 Trillion Loss Concerns This YearChairman Chey Tae-won of SK Group gives 'high praise at CES'... Who is he praising?"Why SK On Pins Its Hopes on Hyundai and Kia's Performance in the U.S."SKT Appoints Group's Strategic Expert, Marking Pinnacle in 'AI Company' Transformation

Gwak Horyung (horr@fntimes.com)

![함영주號 하나금융, '하나더넥스트‘ 연계 확대…신탁수수료 2배 증가 효과 [금융 시니어 비즈니스 돋보기]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260713215904006980b4a7c6999c121131189150.jpg&nmt=18)

![[그래픽 뉴스] ISA 대개편! 나에게 유리한 계좌는?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202608041713155615de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 미국 증시 새로운 키워드 'MANGOS'](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202607291740382069de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 은퇴후 30년 부모님 세대의 생존전략](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202606301704439153de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 제네시스, 럭셔리 경험 더한 ‘2027 GV70’‧‘GV70 그래파이트’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702143546085600749258773622211122717.jpg&nmt=18)

![[AD] 개소세 혜택 종료…현대차, ‘썸머 페스타’로 고객 부담 완화](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260702142355004830749258773622211122717.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)