According to financial reports on the 16th, SK innovation and SK E&S will hold a board meeting on the 17th to discuss the merger.

The key is the merger ratio.

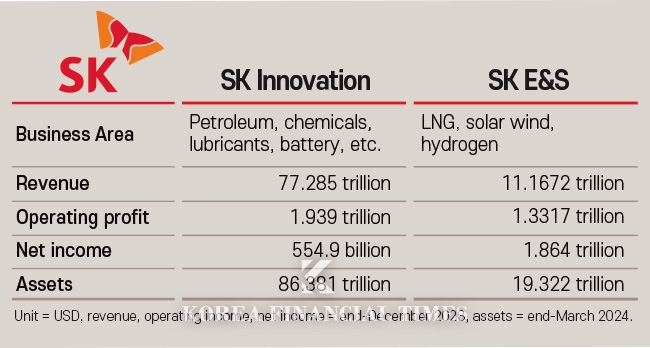

SK E&S is overvalued, while SK innovation is undervalued. Compared to SK E&S, SK Innovation has seven times the sales and assets, but its recent profits are similar. Moreover, SK Innovation's price-to-earnings ratio (PBR) is 0.5x, which is half of the average for KOSPI companies, due to a decline in its stock price due to the sluggish industry.

In conclusion, SK E&S shareholders are favored if the merger ratio is calculated based on stock price, while SK Innovation shareholders are favored if it is evaluated based on asset value under the exception rule.

The industry is expected to discuss the merger ratio based on stock prices. In this case, it is estimated that the merger ratio between SK innovation and SK E&S will be 1:2.

The largest shareholder of both companies is SK Corporation. It owns 36% of SK innovation and 90% of SK E&S. The higher the valuation of SK E&S, the lower the diluted share value after the merger. Convincing private equity firm KKR, which holds redeemable convertible preference shares (RCPS) in SK E&S, is also inevitable. KKR holds 3.1 trillion won worth of SK E&S RCPS. If the merger proceeds by increasing the valuation of SK innovation and KKR opposes the merger, it will have to repay the funds.

However, it is expected to face a backlash from SK innovation's minority shareholders, whose stake value will be diluted. The company is expected to present its future vision through the merger or boost its stock price through a shareholder return policy.

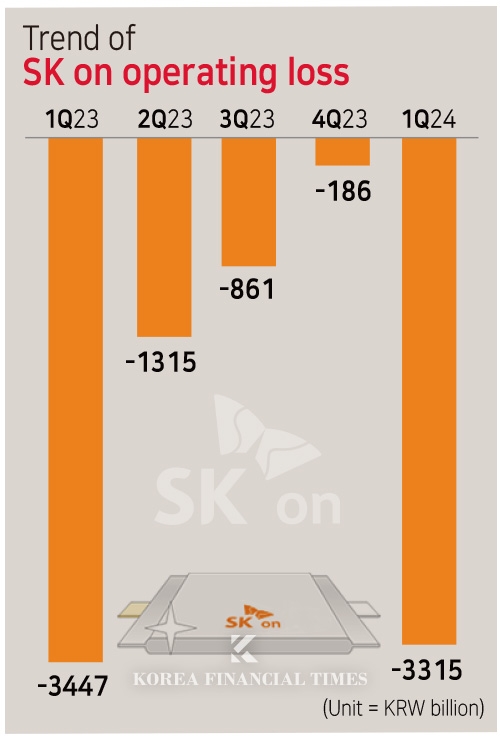

If SK E&S, a cash-generative company, were to merge with its parent company, SK Innovation, it could provide more support for SK Energy.

Of course, this is not a fundamental solution to SK E&S's funding crisis, so it needs to secure its own profitability. SK innovation had previously proposed a merger of its lubricant subsidiary SK Enmove and SK On, but it was reportedly canceled due to stakeholder opposition. More recently, SK Innovation has also been considering a merger with SK Trading International and SK Enterm.

SK innovation said, "We are reviewing various strategic measures to strengthen the competitiveness of the SK ON business, but no specific decisions have been made."

Gwak Horyung (horr@fntimes.com)

![기관 '디앤디파마텍'·외인 '파두'·개인 '주성엔지니어링' 1위 [주간 코스닥 순매수- 2026년 5월26일~5월29일]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260529201200089420179ad439071182351514.jpg&nmt=18)

![12개월 최고 연 8.00%…케이뱅크 '마이키즈 적금' [이주의 은행 적금금리-6월 1주]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202605291008240277701b5a2213792211381469.jpg&nmt=18)

![기관 '삼성전자'·외인 '삼성전자우'·개인 'SK하이닉스' 1위 [주간 코스피 순매수- 2026년 5월26일~5월29일]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=20260529195932045130179ad439071182351514.jpg&nmt=18)

![24개월 최고 연 8.00%…케이뱅크 '마이키즈 적금' [이주의 은행 적금금리-6월 1주]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=69&h=45&m=5&simg=202605291010410727501b5a2213792211381469.jpg&nmt=18)

![[그래픽 뉴스] 퇴근 후 주차했는데 수익 발생? V2G의 정체](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202605131656357745de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] “전쟁 신호를 읽는 가장 이상한 방법, 피자 주문량”](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604151704028482de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 트럼프의 ‘타코 한 입’에 흔들린 시장의 비밀](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202604031646576130de68fcbb3512411124362_0.jpg&nmt=18)

![[그래픽 뉴스] 청년정책 5년 계획, 무엇이 달라지나?](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603301556498218de68fcbb3512411124362_0.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=298&h=298&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[신간]은퇴연옥…김경록의 은퇴 후 삶의 나침반](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260414140833047280f8caa4a5ce12411124362.jpg&nmt=18)

![[신간] 물처럼 흐르고 원칙으로 서다…김용환의 통찰을 담다](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260409114249027860f8caa4a5ce12411124362.jpg&nmt=18)

![[안현정 서평] 플랫폼의 영지에서 ‘미학적 주권’을 선포하라...'K가 죽어야 K가 산다' 장준환 著](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=20260527121426063220c1c16452b012411124362.jpg&nmt=18)

![[서평] 추세 매매의 대가들...추세추종 투자전략의 대가 14인 인터뷰](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=81&h=123&m=5&simg=2023102410444004986c1c16452b0175114235199.jpg&nmt=18)

![[AD] 기아 ‘디 올 뉴 셀토스’, 인도 타임스 드라이브 어워즈서 ‘올해의 SUV’ 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202605071156400590007492587736124111243152.jpg&nmt=18)

![[AD]‘그랜저 잡자’ 기아, 상품성 더한 ‘The 2027 K8’ 출시](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=2026042110193702730074925877361211627527.jpg&nmt=18)

![[카드뉴스] KT&G, ‘CDP’ 기후변화·수자원 관리 부문 우수기업 선정](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=202603241415423015de68fcbb3512411124362_0.png&nmt=18)

![[AD] 현대차, 글로벌 안전평가 최고등급 달성 기념 EV 특별 프로모션](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260106160647050337492587736121125197123.jpg&nmt=18)

![[AD] 현대차 ‘모베드’, CES 2026 로보틱스 부문 최고혁신상 수상](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=89&h=45&m=1&simg=20260105103413003717492587736121125197123.jpg&nmt=18)